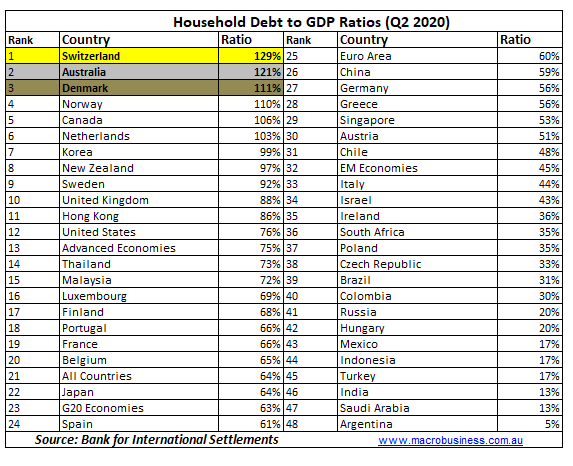

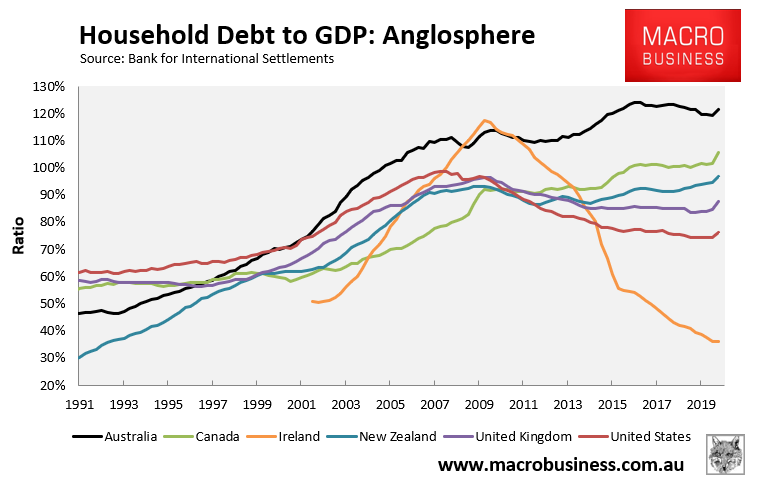

The Bank for International Settlements (BIS) has released its global household debt statistics for the June quarter, which reveals that Australian households remain the second most indebted in the world and easily the most indebted among English-speaking nations:

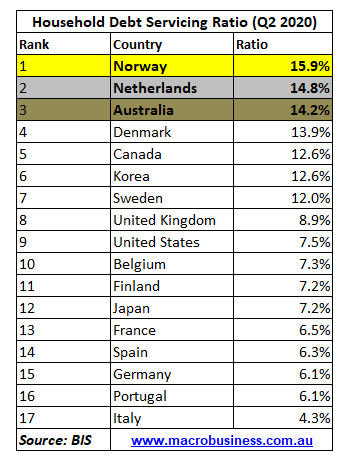

Australia also has the third highest debt repayment burden out of sampled nations and by far the highest debt burden in the English-speaking world:

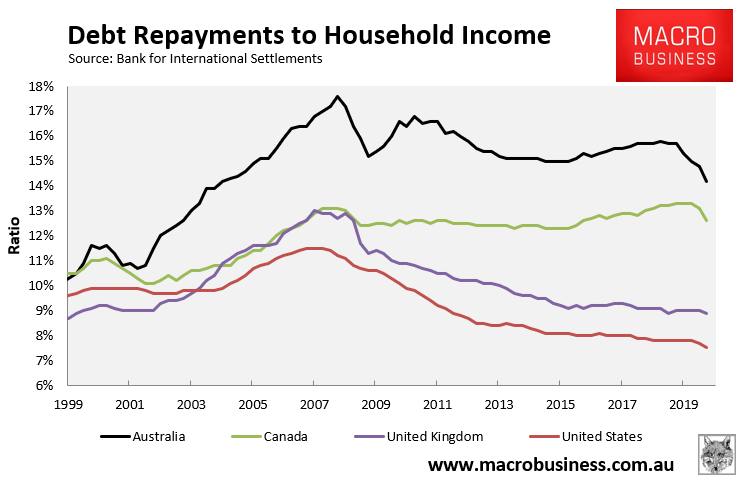

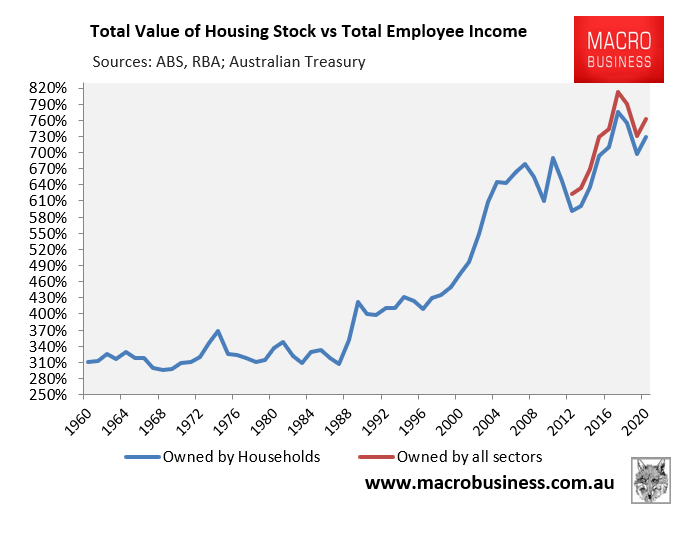

That said, Australia’s debt repayment burden has fallen to its lowest level since September 2004, despite dwelling values running near an all-time high relative to incomes:

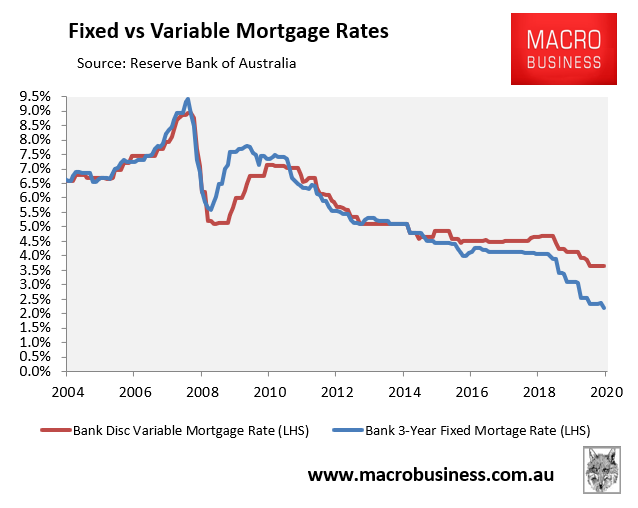

The reason is obvious: average mortgage rates have cratered to all-time lows, namely 3.65% variable and 2.20% 3-year fixed:

Expect the repayment burden to fall further as borrowers pivot to fixed mortgages. Those rates are too low to ignore.