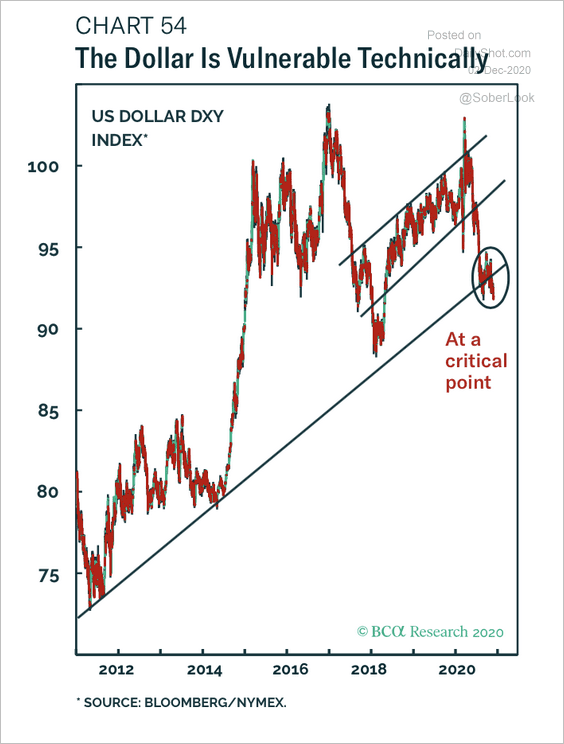

DXY is in free fall as EUR roars:

The Australian dollar is back at breakout highs:

Oil and gold both rose:

Metals fell:

Miners to the moon:

EM stocks lagging:

Junk too:

As curve steepening returns:

Stocks were stable:

Westpac has the data wrap:

Event Wrap

US media suggested that Mnuchin and Trump might agree to Republican Senator McConnell’s Covid relief package, as talks continued in Washington.

US ADP private sector employment rose 307k in November, undershooting the median estimate of 430k, as rising pandemic cases and restrictions in US curbed hiring.

Brexit: EU negotiator Barnier said to EU Leaders that there were still notable disagreements on three main issues and that talks could fail. He was told to continue discussions but that he should not led the deadline force a bad deal.

UK approved the Pfizer/BioNTech Covid vaccine, with an initial tiered rollout of vaccination planned for 15 December, ahead of the US and EU.

Eurozone Oct. unemployment was in line with expectations at 8.4%, although the prior level was revised from 8.3% to 8.5%. Oct. PPI remained very weak at -2.0%y/y, but the +0.4%m/m outturn was above the estimate of +0.2%m/m. Germany Oct. retail sales rose 2.6%m/m (est. +1.2%m/m) to +8.2%y/y (est. +5.8%y/y), notably on IT and clothing purchases.

RBNZ Governor Orr’s speech overnight reiterated that economic risks remain skewed to the downside, and that it remains willing to implement a negative OCR if future conditions required it.

Event Outlook

Australia: Westpac expects that October housing finance approvals will grow by 2%, with owner occupier loans (WBC f/c: 2.8%) likely to continue outperforming investor loans (WBC f/c: 1.2%). The trade balance should remain broadly stable at $5.8bn in October; underlying this, Westpac expects that both imports and exports will advance by around 3.5%. The November AiG PCI will continue to be supported by housing construction – the survey recently printed above 50 for the first time since August 2018.

New Zealand: Westpac expects that building consents will fall by 5% in October. That follows a large number of apartment consents in September, which tend to be issued in lumps. That would still leave annual issuance at very high levels, signalling a strong construction pipeline as we head into the new year. November ANZ commodity prices will be published, with dairy prices stable over the month.

China: The November Caixin services PMI is set for another strong print as the sector benefits from the resurgence of household spending (market f/c: 56.4).

Euro Area: October retail sales will come under pressure as lockdowns inhibit consumer movement (market f/c: 0.7%).

US: Consecutive increases in initial jobless claims raise concerns around softness in the labour market (market f/c: 775k). The November ISM non-manufacturing index remains above pre-COVID levels, but is expected to retrace as the virus’ spread and capacity constraints hinder the recovery (market f/c: 55.8).

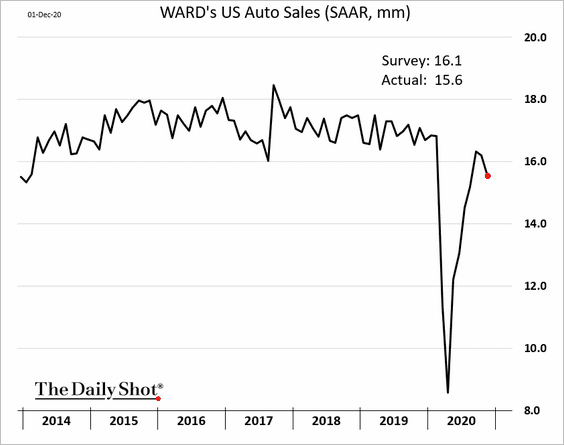

It still appears that the Us hs flattened the virus curve though squashing it going to take time:

Short term, the economic damage is mounting:

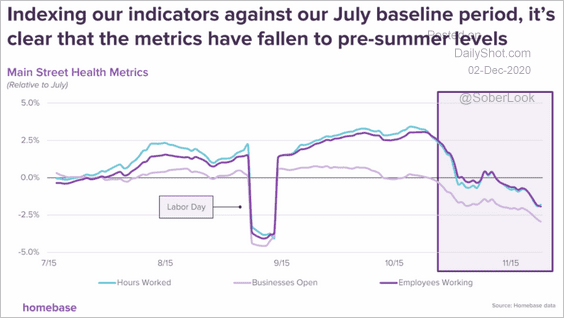

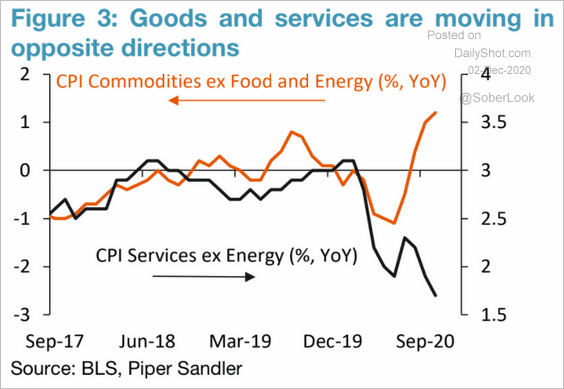

But it remains entirely services based as the global inventory cycle lifts all manufacturing boats:

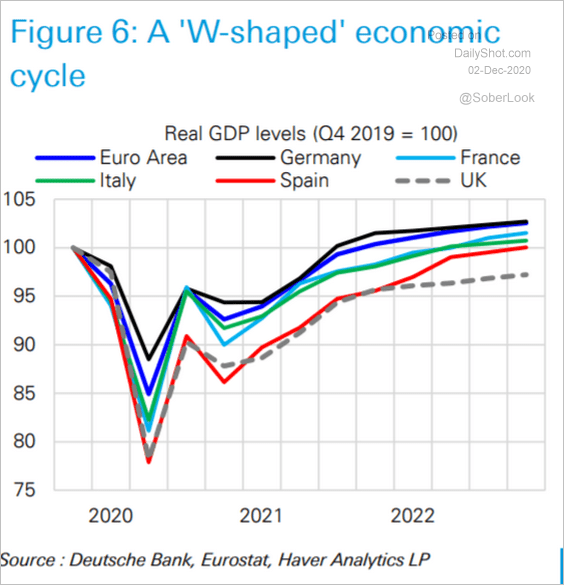

Europe is no shape to survive a rocketing EUR:

But that’s too bad. Global reflation always means a strong EUR as DXY falls with more ahead:

The AUD will track the EUR.