DXY is down, down:

The Australian dollar has broken out:

Gold and oil and running:

Metals fell:

Miners shimmy, shimmy, whoosh!

EM stocks broke out:

Junk on fire:

US yields fell:

Stocks added small gains:

Westpac has the wrap:

Event Wrap

US weekly initial jobless claims fell more than expected to 712k (vs est 776k, prior 787k), breaking a string of two consecutive increases. Continuing claims also fell more than expected, to 5520k (vs est 5800k, prior 6089k). ISM services activity slipped as expected, from 56.6 to 55.9. Components were mixed, with employment firmer but new orders weaker.

Senate Majority Leader McConnell said that it was “heartening” that Democrats have embraced a smaller stimulus package but gave no indication he was willing to increase in order to reach an agreement. “Compromise is within reach. We know where we agree. We can do this,” he said to Senate.

The European Union’s chief Brexit negotiator Barnier, is poised to leave trade talks in London on Friday morning to return to Brussels, diplomats saying the outline of a deal could emerge within the next 48 hours.

Event Outlook

Australia: The preliminary estimate of October retail sales revealed a 1.6% increase – the 5% surge in Victoria was a little surprising given that restrictions were not being fully relaxed until November. Westpac expects that the final print will remain unchanged (WBC f/c: 1.6%).

New Zealand: Westpac is forecasting a 33% rise in Q3 building work, with bounce backs in both residential and non-residential work following the easing in Covid-related restrictions. Risks are to the upside, due to possible catch-up activity.

US: The November employment report is due, and Westpac expects non-farm payrolls will increase by 450k (consensus 475k). That would see the unemployment rate hold at 6.9% (consensus 6.8%). Risks are to the downside, with ADP employment coming in under expectations and initial claims posting consecutive increases. With considerable slack in the labour market, average hourly earnings are likely to remain weak for an extended period (WBC f/c: 0.1%). The October trade balance is expected to show that the deficit continued to widen (market f/c: 64.8bn). Factory orders should expand 0.8%, but investment remains in limbo against the uncertain backdrop. Finally, the FOMC’s Bowman (02:00 AEDT) and Kashkari (03:00 AEDT) will speak.

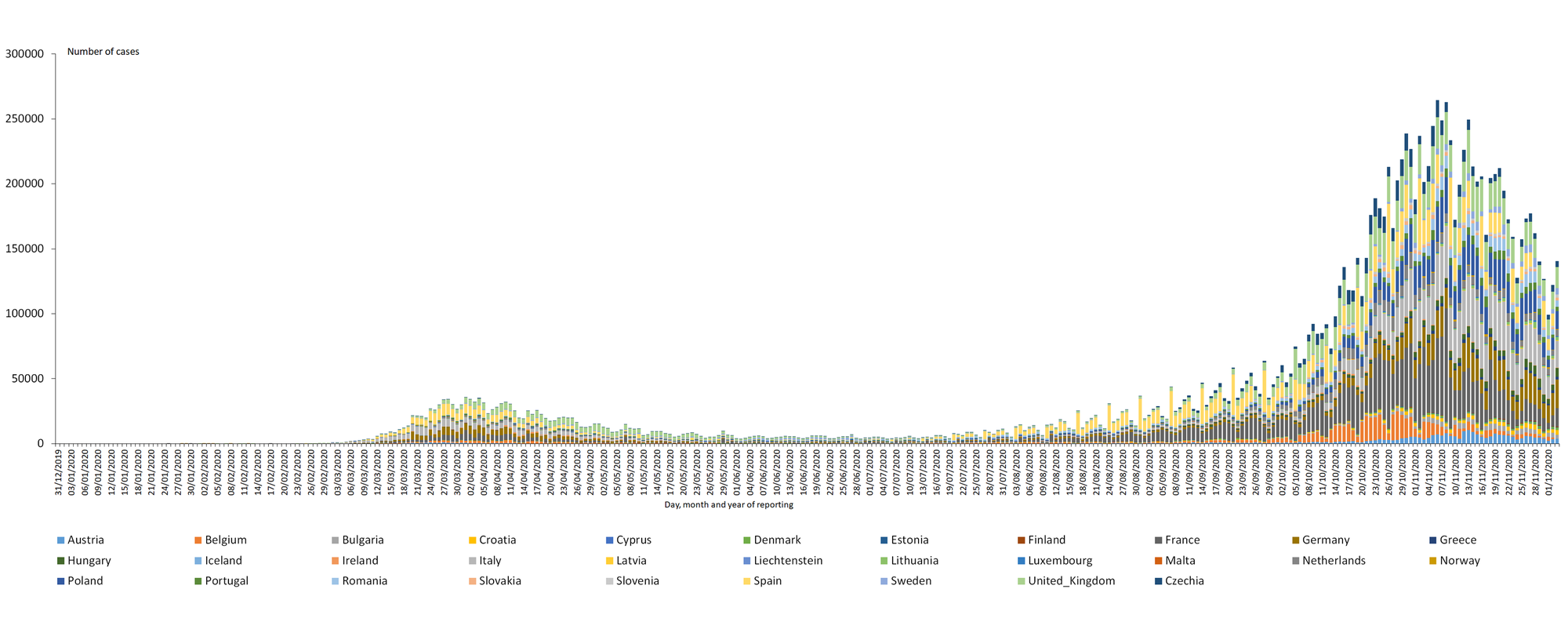

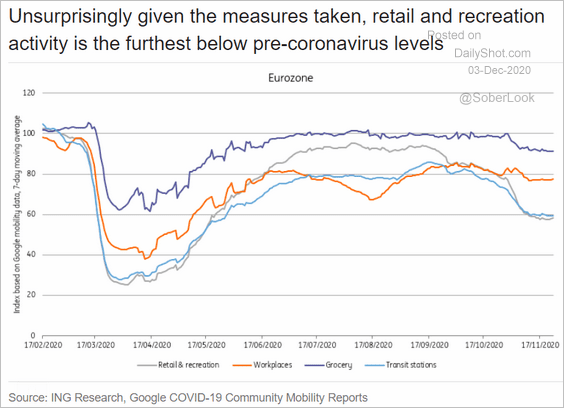

The virus continues to retreat in Europe:

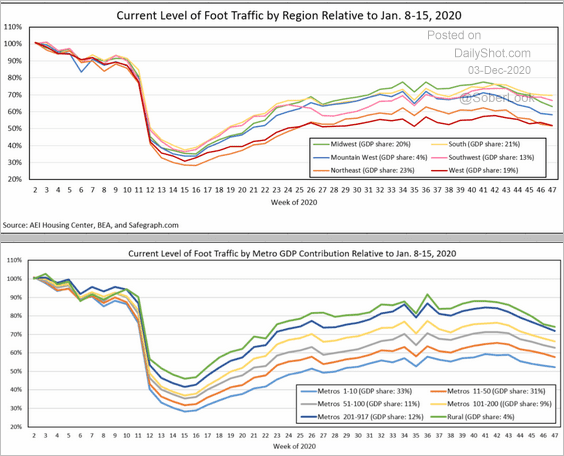

Along with the services economy:

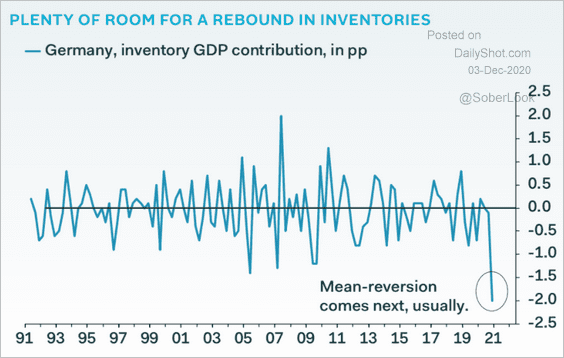

However, industry is on a winner with the inventory cycle which will run through much of next year:

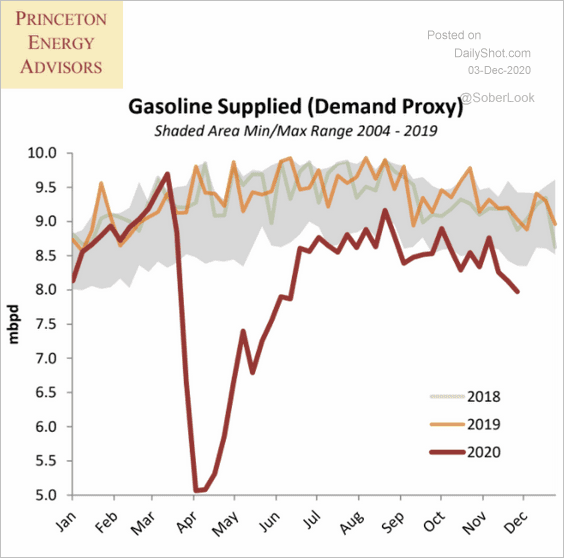

The US virus still appears toppy post-Thanksgiving though not so convincingly:

As it slowly but surely closes enough:

And so the market keeps looking through to the sunny uplands of vaccine-led recovery.

I had hoped that the last wave of virus would discount assets for some good entry points but no such luck. There is a rude profits boom coming over the next year or two as a combination of forces combine:

- rebounding aggregate demand landing on huge cost cuts and efficiencies;

- full bore stimulus, central bank inflation elasticity and suspended capitalism;

- no inflation and no wage pressure, plus

- a global inventory rebuild.

Doesn’t get much better than that. DXY will keep falling and AUD keep rising while it lasts.