DXY is into its widely expected post-COVID swoon. EUR took off:

Thr Australia dollar firmed but held back:

Other EMs did better:

Oil fell, gold lifted:

Base metals are manic:

Big miners too:

EM stocks were firm:

Junk too:

Treasuries copped it on stimulus scuttlebutt:

Stocks piled it on:

Westpac has the data wrap:

Event Wrap

Optimism in the US about a reopening of negotiations towards a bipartisan Covid support package gained force as Mnuchin and Pelosi scheduled a call. Further, Senator Manchin (Dem) announced, “…a bipartisan, bicameral framework for a Covid-19 relief package. This proposal would direct more than $900bn to help small business, healthcare providers, and unemployed Americans who need help now. It’s time to put politics aside & do what’s best for our country”.

There was also optimism over reported comments that negotiations for a “UK-EU trade deal have entered the ‘tunnel’”. Although UK officials did not respond, EU officials suggested that it was an appropriate assessment.

ECB’s Schnabel affirmed the likelihood of easing in the form of extended and enlarged PEPP and longer duration TLTRO’s with favourable terms. Although not markedly different from previous ECB comments, they did clarify a longer period of PEPP due to the extended Covid impacts.

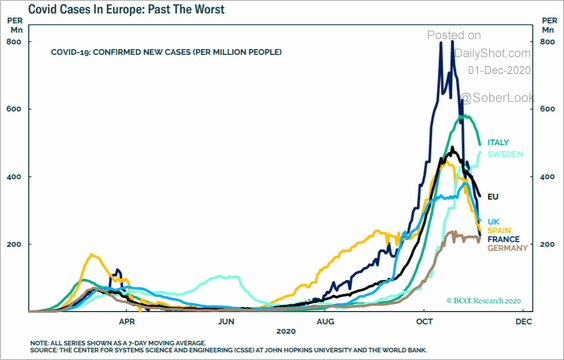

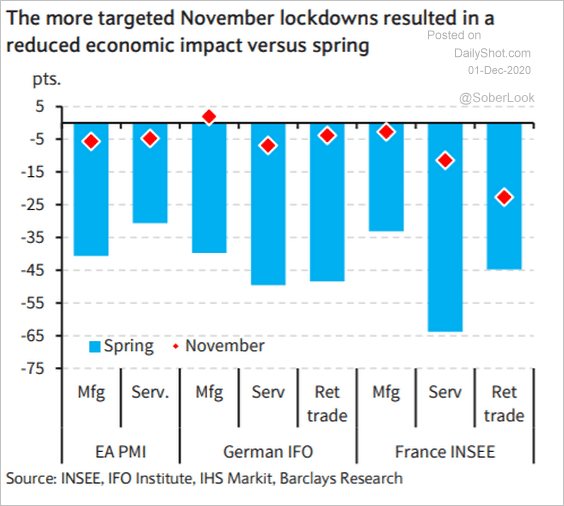

Eurozone final Nov. manufacturing PMI rose to 53.9 from the flash 53.6. Markit reported a solid pace of growth and an avoidance of the lockdown hit of 2Q. However, they did note that services are being hit hard, while also looking positively towards an easing of lockdowns and less reliance on German activity.

UK final Nov. manufacturing PMI also rose to 55.6 from the flash 55.2, although some activity was attributed to stockpiling in advance of the Brexit transition period ending. Unlike the Eurozone, UK manufacturing continued to shed jobs.

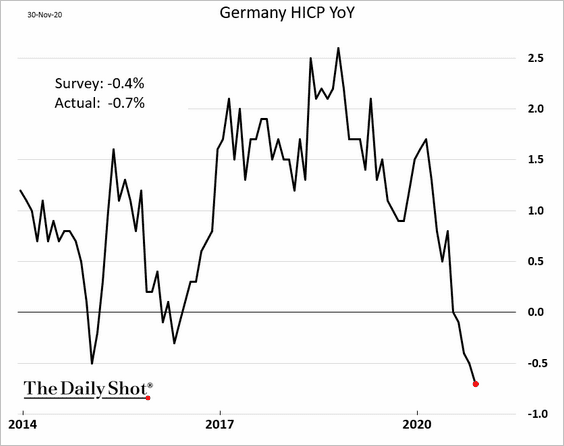

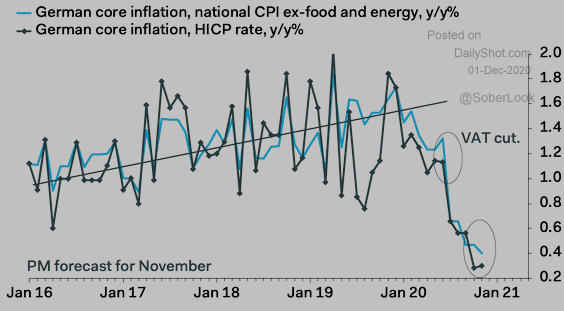

Eurozone Nov. CPI fell 0.3%m/m (est. -0.3%m/m) and -0.3%y/y (est. -0.2%y/y), with core CPI unchanged and in line with estimates at +0.2%y/y. German unemployment in Oct. was yet again below estimates. Unemployment fell -39k (estimated to rise 8k), while the unemployment rate fell to 6.1% (est. 6.3%, prior 6.2%).

US ISM activity survey weakened as expected to 57.5 (est. 58.0) from 59.3. The key employment component fell to 48.4 from 53.2, but new export orders rose to 57.8 (from 55.7), and the fall in production still left it at a solid 60.8 (prior 63.0). US manufacturing PMI was unchanged from its flash reading at 56.7.

Fed Chair Powell testified on the CARES Act before the Senate Banking Committee. As expected, he reiterated that the Fed is committed to using all of its tools to support the recovery; the CARES Act has provided the lion’s share of aid to the economy and the emergency programs remain available; although the economy has performed better than expected, it still has a long way to go with 10m people out of work; and it may be that more is needed on the fiscal policy front.

Event Outlook

Australia: The COVID pandemic triggered a severe recession over the first half of 2020 – with output a -0.3% for Q1 and a -7.0% for Q2. The second half of the year sees the virus under control locally (but only after a 2nd lock-down in Victoria) and restrictions being reversed. We expect Q3 GDP to expand by 3.0% (-3.9%yr). At 10:00 am AEDT, RBA Governor Lowe will appear before the House of Representatives Standing Committee on Economics.

New Zealand: The Q3 terms of trade are expected to fall 4.0% on temporary export price weakness. RBNZ Governor Orr will speak via Zoom to an invitation by the Australian National University in Canberra, the speech to be published on the RBNZ website at 7:30pm NZT.

Euro Area: The October unemployment rate is expected to rise a notch as the labour market continues its softening trend (market f/c: 8.4%).

US: Westpac is looking for a print of 430k in the November update of ADP employment – initial claims point to downside risks. The Federal Reserve’s Beige Book will provide a snapshot of conditions across the Fed districts; the employment gains highlighted in the September publication may begin to unwind. Finally, Fed Chair Powell (02:00 AEDT) and the FOMC’s Williams (05:00 AEDT) will speak.

The swooning DXY is a typical feature of any global recovery. As growth expectations rise, capital flows out of US money centres and into higher-yielding countries, typically EMS, which also consume the lion’s share of commodities, so they get a double lift from a monetary tailwind and demand. It’s a simple and reliable global reflation mechansim.

How far does it get? Post-GFC, the DXY sank a very long way. But that was in part a function of two things. First, the Federal Reserve was one of only a very small group of central banks doing QE. Second, and in particular, Europe was not doing it, so the EUR was strong (in between bouts of crisis around the debt crisis). Once the ECB began the print and the US to recover, the situation of respective currencies reversed:

I expect we’ll something similar this time around. But I do not think that DXY will sink as far as did in 2008-11. mid to low 80s is enough this time as 2021 lifts global growth and Europe recovers with it from its current funk:

Europe has been bashed up much more than the US economy in the virus third wave so its recovery will be faster. That can support the EUR rising/DXY falling trade for six to twelve months. But after that, things will revert pretty quickly. Europe will have more long term economic damage with more zombies and greater exposure to next year’s China slow down. Its lowflation is embedded much deeper than even the US’s. It’s fiscal support will be less as well.

So, soon enough, the ECB will be printing more than the Fed and EUR will fall again, lifting DXY:

This is one major reason why I do NOT see the Australian dollar running away in a multi-year bull market akin to the post-GFC environment. In fact, I expect it reverse downwards pretty quickly with EUR, perhaps as early as H2, 2021, especially as China slows and decouples us as well.