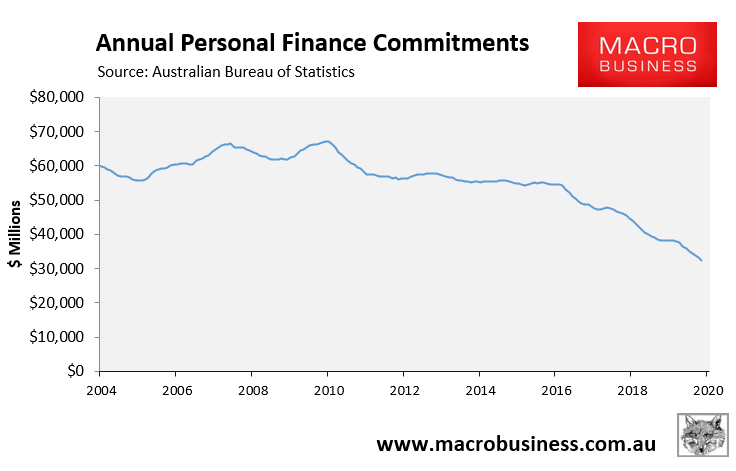

Thursday’s Lending Indicators data for October from the Australian Bureau of Statistics (ABS) revealed that Australian households continue to shun consumer borrowings, with personal finance commitments collapsing to another record low:

As shown above, annual new personal finance commitments fell by 15.3% year-on-year and were 42% below the long-term average.

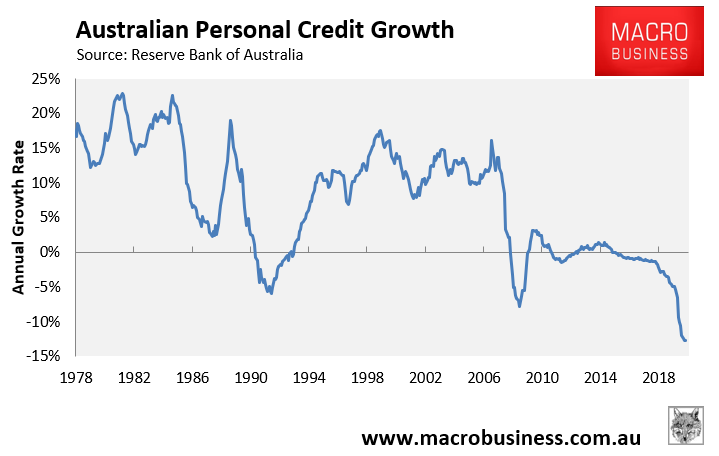

This followed last week’s private credit data from the RBA, which also showed that personal credit has plummeted to its lowest level on record:

The outstanding stock of personal loans fell by a record 12.7% in the year to October, easily eclipsing the falls experienced during the early-1990s recession (-6.0%) and the GFC (-7.8%).

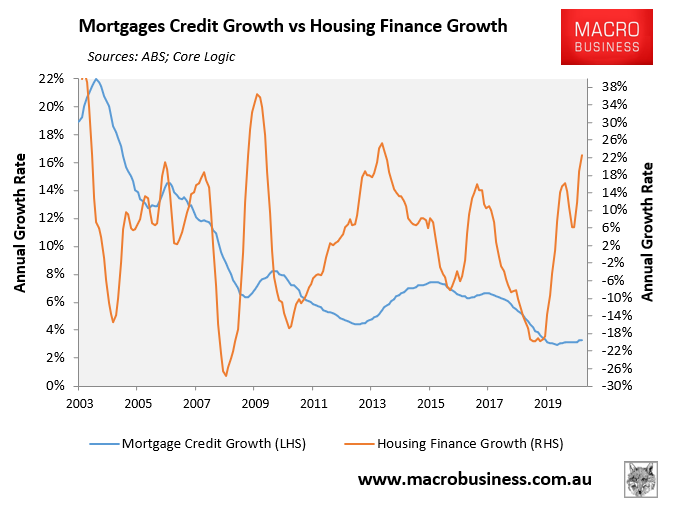

The only area where Australian households are gearing up is for property purchases:

The growth in new mortgage commitments (excluding refinancings) has lifted to levels not seen since 2013.

That said, growth in the stock of mortgage credit outstanding (mortgage growth) has barely lifted, suggesting those already “in” the market are repaying their mortgages at a furious pace, largely offsetting the new mortgage demand.

The bottom line is that Australian households are shunning debt for everything other than to purchase a new home.