The Australian Bureau of Statistics (ABS) has released data showing the total value of Australia’s dwelling stock as at the September quarter of 2020.

Australia’s dwelling stock owned by households was valued by the ABS at a whopping $6.95 trillion as at 30 September 2020, whereas the total housing stock was valued at $7.28 trillion.

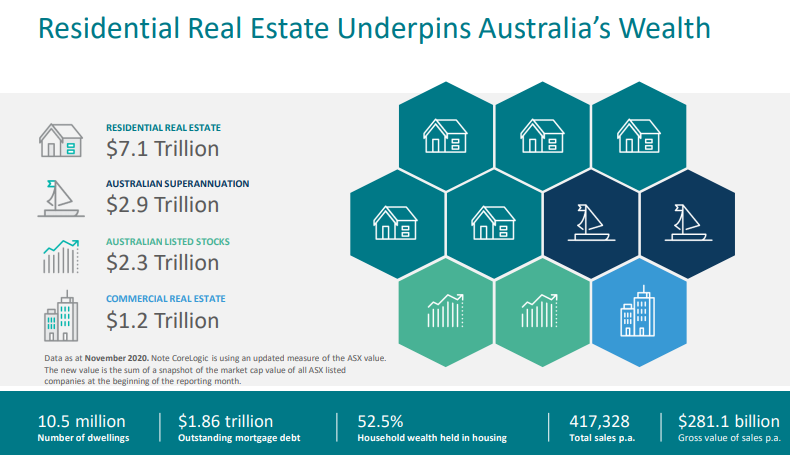

This is slightly above CoreLogic’s $7.1 trillion total housing valuation as at October 2020:

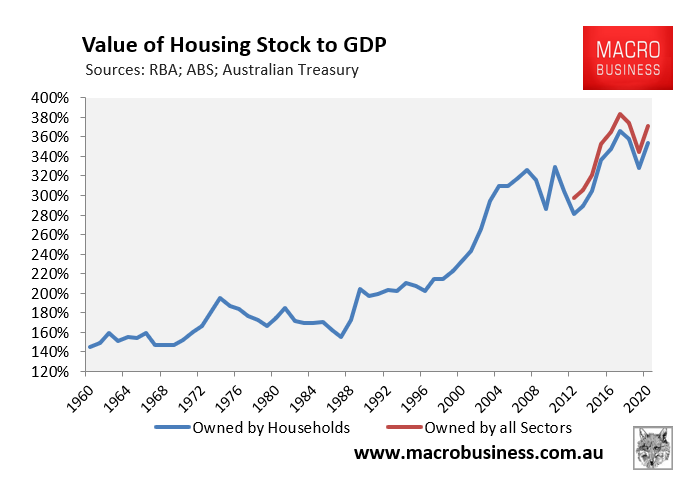

As shown in the next chart, the total value of Australia’s dwelling stock owned by households was 3.54 times as at September 2020, up from last year’s trough of 3.28 times, but still below the peak of 3.66 times GDP in the June quarter of 2017. The total housing stock was valued at 3.71 times GDP in the September quarter, down from a peak of 3.84 times GDP as at June 2017:

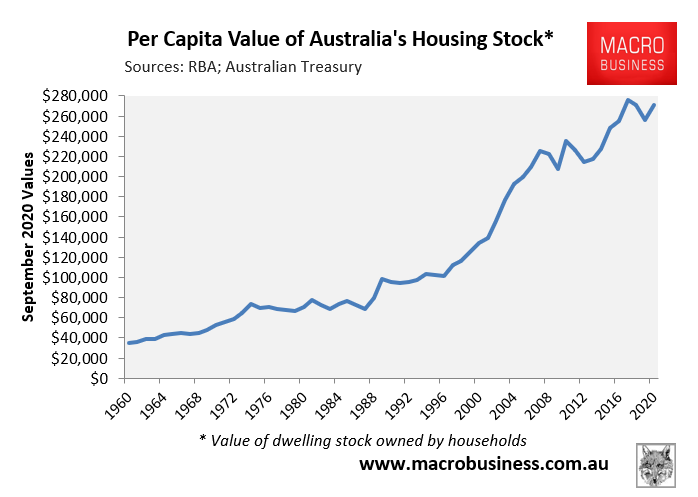

When divided by Australia’s estimated resident population, Australia’s dwelling stock owned by households was worth $271,470 per head of population in the September quarter, up from last year’s trough of $255,934, but down from a peak of $275,897 in the June quarter of 2017 in real inflation-adjusted terms:

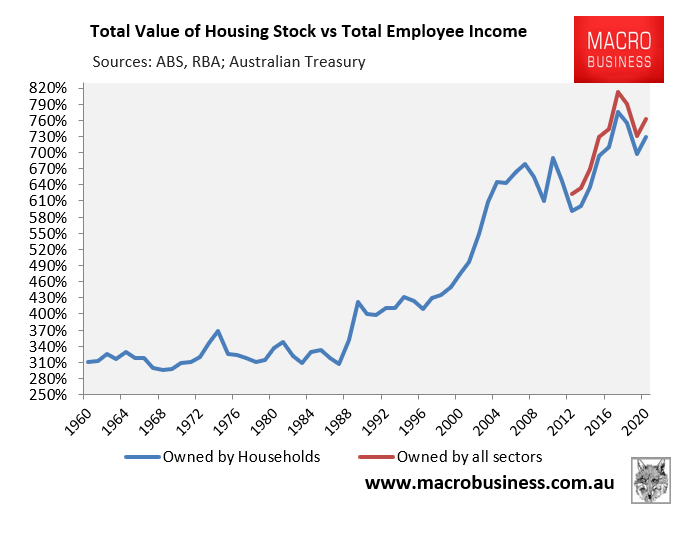

Finally, the total value of Australia’s dwelling stock owned by households only rose to 7.28 times employee incomes as at 30 September 2020, up from June 2019’s trough of 6.98, but still below the 7.76 times incomes at the peak in June 2017. The total housing stock was valued at 7.63 times employee incomes in September, below the 8.13 times incomes in June 2017:

A breakdown of valuations by state, albeit only to the June quarter of 2021, is available here.