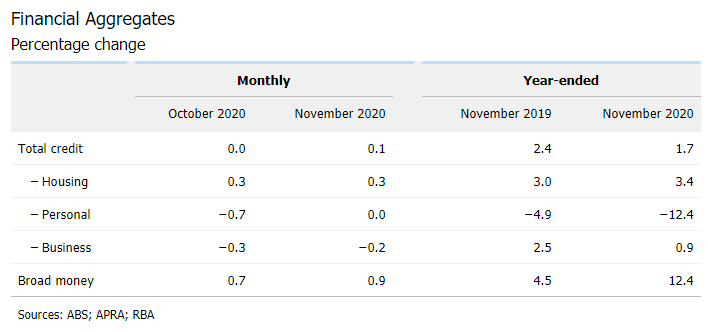

The RBA has released its private sector credit aggregates data for the month of November, which continued the strong rebound in mortgage growth.

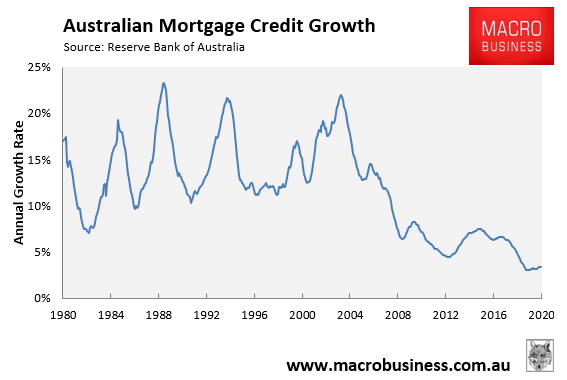

A chart plotting the long-run time series is shown below:

Advertisement

Annual mortgage growth continues to trend higher, but remains low overall at just 3.4%.

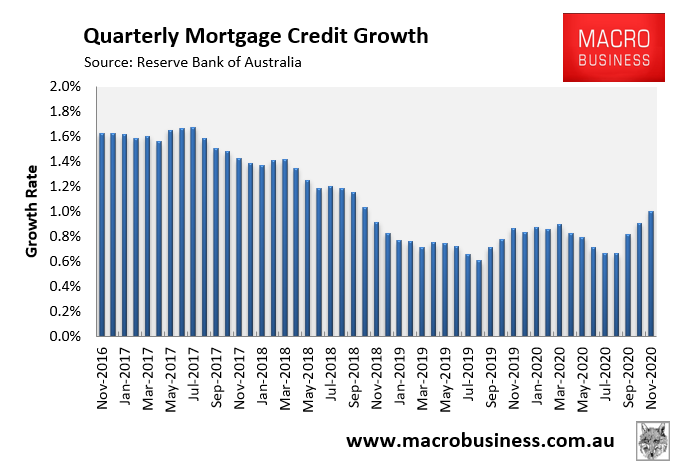

However, quarterly mortgage growth has rebounded hard, climbing for three consecutive months:

Advertisement

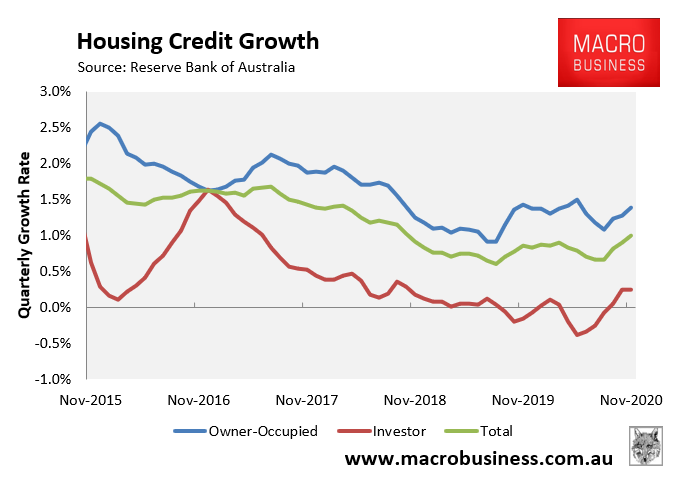

As shown below, quarterly mortgage growth is being driven by owner-occupiers; although investors have also rebounded:

Another positive indicator for the Australian property market.

Advertisement