By Gareth Aird, head of Australian economics at CBA:

Key Points:

The 2020/21 Mid-Year Economic and Fiscal Outlook (MYEFO) is scheduled fornext week(date to be confirmed).

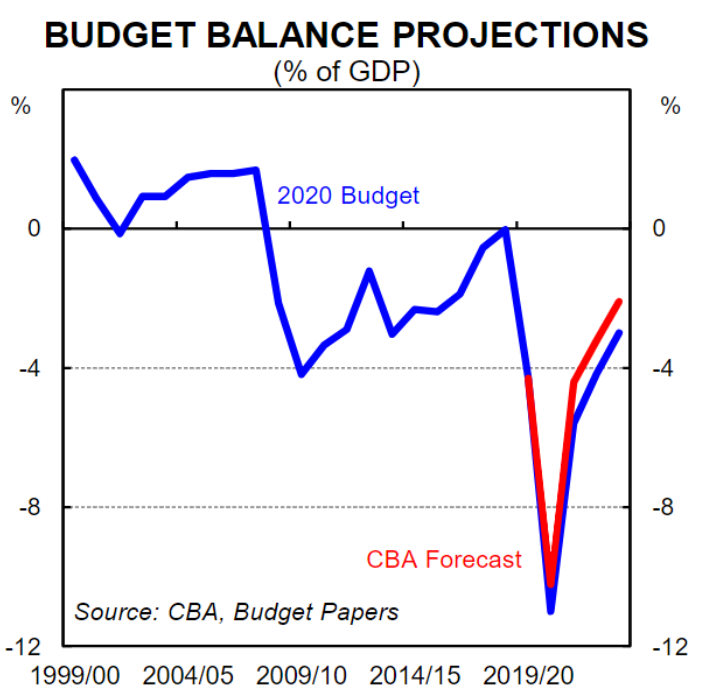

The MYEFOshould show an improved Budget bottom line.

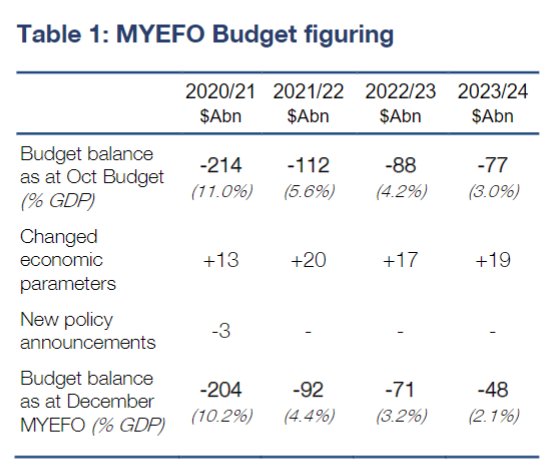

Our point estimate for the revised underlying cash deficit in 2020/21 is $A204bn (10.2% of GDP)

Overview

The landmark 2020/21 Budget was delivered on 6 October, so the gap between the MYEFO and the Budget is a lot shorter than usual this year. A shorter period of time between the Budget and MYEFO should mean a smaller prospect of material revisions to the Budget bottom line. But this is no ordinary year and the economic recovery is occurring a lot faster than the Government expected. This means that we expect a decent upgrade to economic forecasts and by extension the fiscal projections in the MYEFO.

Our working assumption is that the MYEFO is not a “policy document” and we do not expect it to contain anything major in the way of policy announcements. Rather it should simply contain updated economic forecasts and fiscal projections including the operating statement, balance sheet and cash flow statement. Detailed commentary will accompany the updated figures as is always the case.

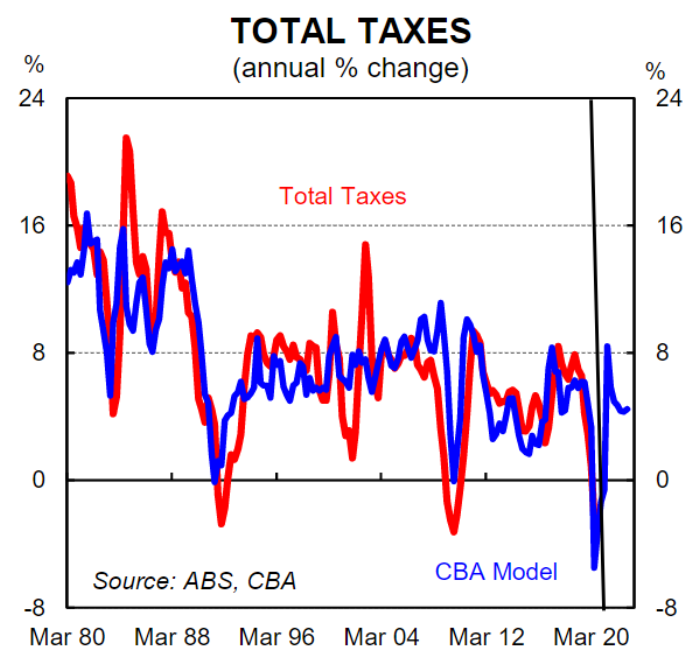

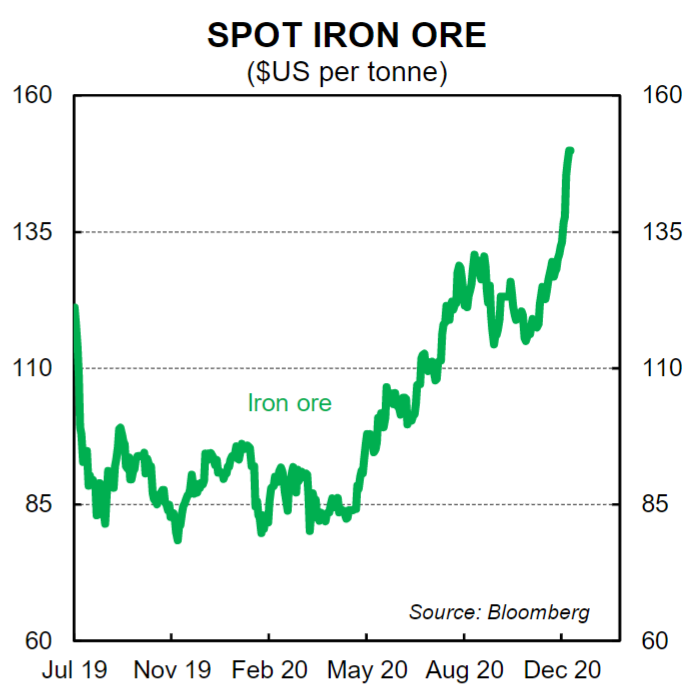

Revenue up and expenditure down On our estimates, changes to the economic parameters that drive budget forecasts will deliver an improvement of $A13bn in 2020/21. Parameter changes primarily relate to changes in economic forecasts, particularly nominal GDP which drives the revenue side of the equation,as well as the level of unemployment which underpins welfare payment forecasts. The news around both nominal GDP and the labour market is significantly better than expected since the October Budget. On revenue specifically, the price of iron ore has risen sharply over the past few months and at the current level around $US150 per tonne has significantly exceeded Treasury estimates which assumed the price of iron ore would fall to $US55/t by the end of Q2 2021.The swing is large and should see tax receipts boosted by around $A2bn in 2020/21 (there is further upside the longer the price of iron ore remains elevated).

Second, despite the lockdown in Victoria,household consumption rose sharply in Q3 20 and has continued to push higher in Q4 20. The lift in spending will have exceeded Treasury’s implied quarterly growth profile. This will mean higher nominal GDP. Third, growth in employment and hours worked will have been stronger over the first four months of 2020/21 than Treasury’s estimates, indicating a likely increase in personal tax revenue. Overall our fiscal model is pointing to a revenue upgrade in 2020/21 of ~$A8.6bn. The expenditure side should also look in better shape. The unemployment rate has so far undershot Treasury estimates. And importantly it was revealed on 30 November that there were around 700k fewer employees/eligible business participants on JobKeeper in October (1.5 million) than compared with the Budget assumption (2.2 million). We estimate this will ‘save’ the Budget $A5bn in Q4 20.

New policy announcements since the Budget around the extension to HomeBuilder, the ‘coronavirus supplement’ and the expanded eligibility for the legislated temporary full expensing measure will add to expenditure. But the sums will be small relative to the additional revenue and lower expenditure that is the direct result of the better than expected improvement in the economy.

In summary, the size of the projected budget deficits will remain extraordinary. But overall we can look forward to some good news in the MYEFO relative to what was presented in the October Budget.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.