According to The Australian’sJudith Sloan, Australia’s current retirement income system is a costly one that contains a range of inequities. One alternative would be to combine a universal pension with voluntary savings, which is essentially the New Zealand model. Sloan argues that such a model would likely cost taxpayers less than the present system, while creating a competitive savings market that would result in lower fees than under compulsory superannuation:

The combination of a means-tested Age Pension and compulsory superannuation with generous tax concessions results in a costly system generating a number of inequities…

It’s a great deal for the superannuation funds and the sub-industries that hang off them — but that shouldn’t be an objective of policy.

The alternative of universal pensions topped up with voluntary savings would, in all likelihood, generate better outcomes for most retirees as well as cost the taxpayer less. And having a competitive savings market would mean much lower fees than compulsory superannuation throws up. (More than $30bn is lost in superannuation fees each year, with some management fees more than 100 basis points of the value of assets under management.)…

Consider the universal pension idea. Everyone gets a certain amount on reaching a specified retirement age. Ideally, the qualifying age is adjusted to reflect increases in longevity.

All that bureaucratic faffing about, deciding whether someone is eligible for the Age Pension and at what rate, disappears. These cost savings alone would be substantial. And all that game-playing and manipulation on the part of older citizens to get the best deal out of the Age Pension would be for nought…

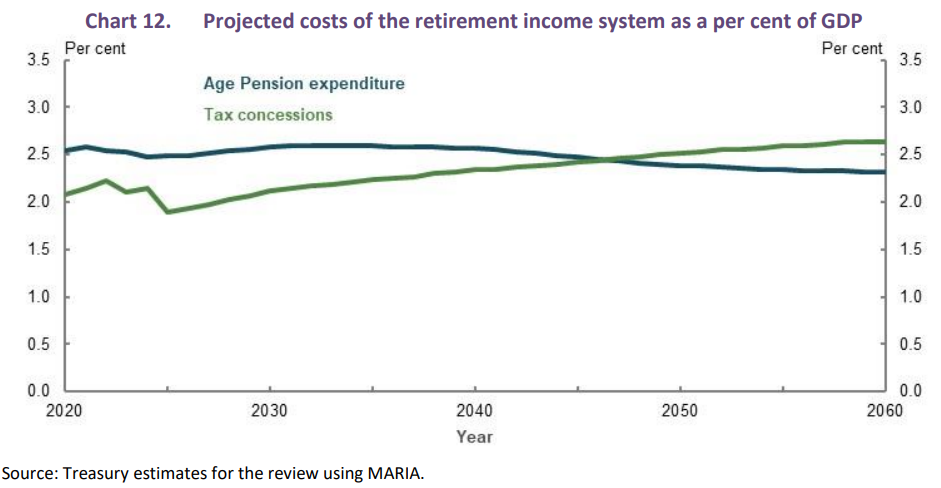

All things being constant, it is estimated the cost of the Age Pension will be eclipsed by the cost of the superannuation tax concessions. As the Retirement Income Review concludes, “government expenditure on the AP as a proportion of GDP is projected to fall slightly over the next 40 years. [But] the cost of superannuation tax concessions is projected to grow as a proportion of GDP and exceed that of AP expenditure by around 2050.”

In other words, compulsory superannuation saves taxpayers nothing in net terms; in fact, it costs them.

Well said. Compulsory superannuation acts like a tax and forces people to forgo current consumption – a particularly pernicious outcome for lower-income earners. It has also created a massive trough, worth some $30 billion a year, that has attracted snouts like Australia’s four major banks.

Superannuation concessions currently cost the Budget $43 billion a year and are very poorly targeted to high income earners, who receive the lion’s share of taxpayer assistance:

Advertisement

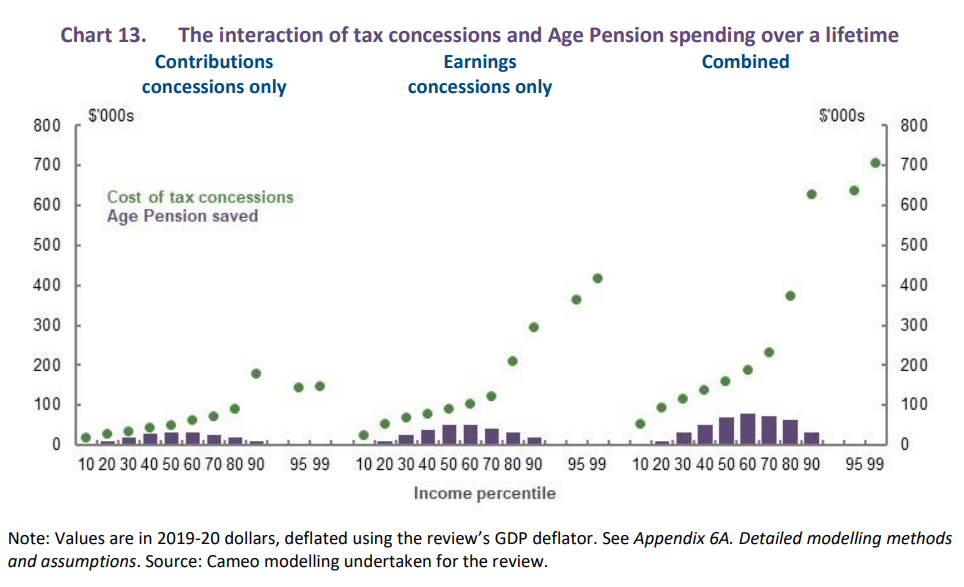

Moreover, the Retirement Income Review estimates that the cost of superannuation concessions will dwarf the Aged Pension, and costs taxpayers more in net terms:

As the superannuation system matures, the cost of superannuation tax concessions is projected to grow as a proportion of GDP such that by around 2050 it exceeds the cost of Age Pension expenditure as a per cent of GDP (Chart 12). This is the result of growth in the cost of earnings tax concessions…

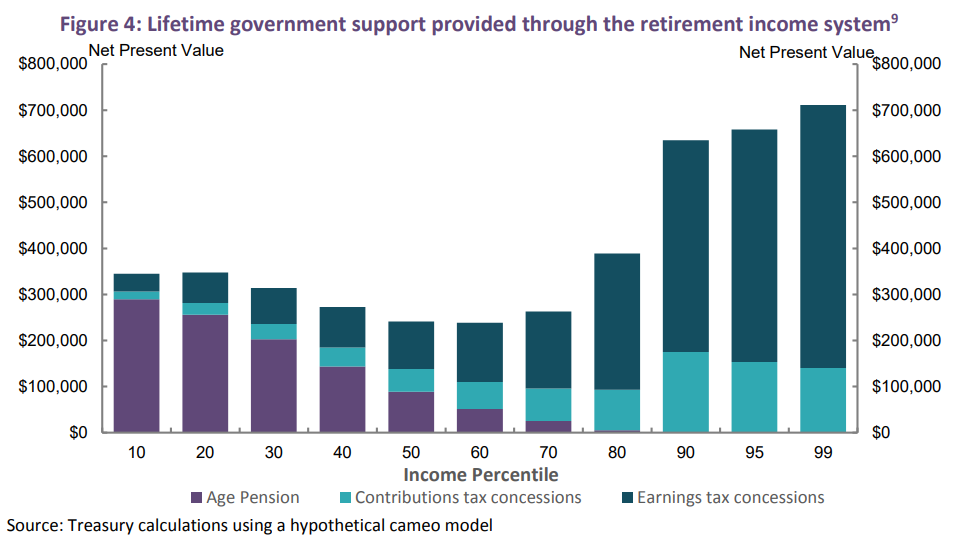

To the extent that superannuation tax concessions are contributing to higher superannuation balances of lower- to middle- income earners, they help to reduce Age Pension expenditure. But the main influence behind the growth in superannuation balances is the SG. Tax concessions are largely concentrated among higher-income earners who are close to and above preservation age. Across the income distribution, the lifetime cost of superannuation tax concessions is projected to outweigh the associated Age Pension saving (Chart 13)…

Advertisement

By extension, the current superannuation arrangements mean there are less funds available in the federal budget to lift the Aged Pension.

As noted above by Judith Sloan, New Zealand has a voluntary superannuation system that works very well. In fact, several years ago I met Bill English when he was Finance Minister and we discussed superannuation in some detail. English was reluctant to implement an Australian-style compulsory system precisely because he believed it would lead to inefficiency and ticket-clipping by the industry, while draining the Budget of revenue. Moreover, with a universal Aged Pension and no compulsory super, New Zealand has a savings rate similar to Australia’s. This speaks volumes.

There are few better rent-seeking industries to be in than superannuation. Abolishing the compulsory system in favour of a universal aged pension has merit and should be given detailed consideration.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.