Sep residential approvals rebound much stronger than expected 15.4% to 190k

Residential building approvals were far stronger than expected in September, up 15.4% m/m (UBS: 0.0%, mkt: 1.5%, pre: -2.3%), to 190k annualised (after 165k), the highest level since February, and one of the highest since the 2018 boom. The y/y picked up to 8.8% (after 0.7%). The m/m was led by volatile ‘other’/multi’s (23.4% after -12.1%; -12.1% y/y); but houses also lifted again (9.7% after 4.4%; 20.7% y/y). Overall, we are cautious to extrapolate one month of data. However, given the extent of the ‘beat’, we now expect dwelling commencements of 170k in 2020 (was 160k), and 180k in 2021, albeit both with upside risk. Meanwhile, alterations and additions (i.e. renovations) approvals increased further (1.1% m/m after 4.7%, 11.2% y/y), to be on a positive trend. Elsewhere however, non-residential building approvals retraced very sharply after rebounding (-36.7% m/m after 40.0%, -25.7% y/y), to the lowest level in almost 4 years; showing the negative impact of COVID on the outlook for business investment.

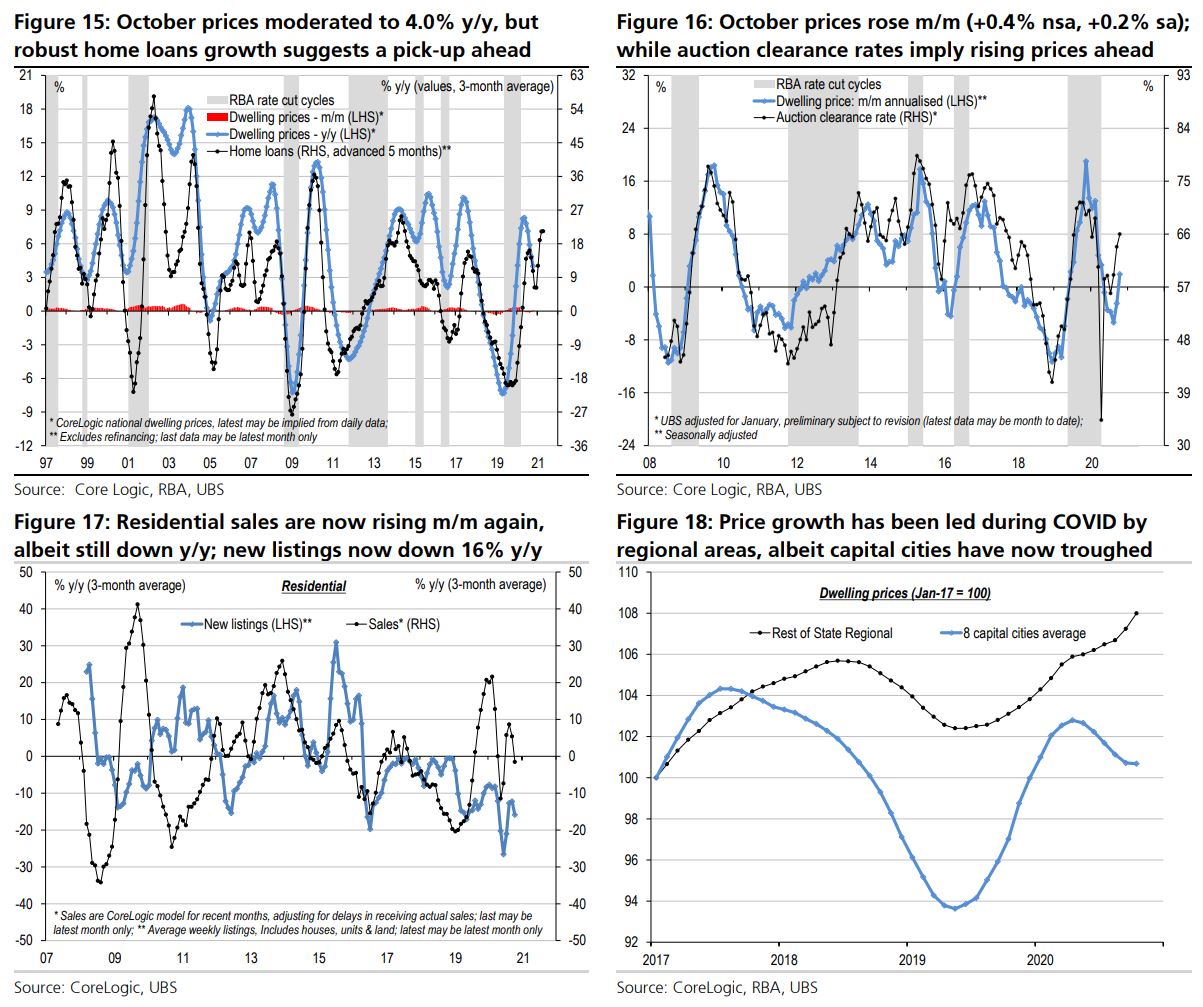

Oct home prices +0.2% m/m; UBS upside case realised… rises ahead

CoreLogic dwelling prices (seasonally adjusted) rose 0.2% m/m in October (UBS: +0.2%), the first increase since April. Across the prior five months, the peak-to-trough decline in this COVID cycle was small at -1.3% (or -2.1% non-seasonally adjusted). While this is better than our initial expectations when COVID struck of a 5% to 10% decline, for several months we have already cited upside risk to our forecast for (CoreLogic) prices (we highlight our analysis of Valuer General data indicates the peakto-trough price decline for Sydney houses was ~8% – in line with our view). Overall, we now expect positive price growth ahead. The key drivers are: 1) the RBA rate cuts are having a stronger than expected impact; 2) COVID cases fell towards zero, boosting sentiment, and seeing Melbourne finally exit lockdown. However, the primary drivers of the downside risk remains: 1) another wave of COVID sees renewed lockdowns; 2) the expiry of mortgage deferrals next year sees distressed supply that causes a ‘double-dip’ of prices; and 3) ~no migration cause a drop in ‘underlying demand’, especially as current incentives for new housing and/or first home buyers expire next year. However, we expect that if prices were to weaken again, then already unprecedented policy support would be ramped up even further. Meanwhile, in October, the y/y moderated further to 4.0% (after 4.9%). Reflecting the prior lockdown, Melbourne is clearly the weakest (-0.6% m/m, and -4.8% since April); but other cities are flat or rising, and regional areas are strong (0.7% m/m, 4.7% y/y). Meanwhile, the (modelled) number of home sales is recovering again recently, with October up ~7% m/m (after +1%), although still falling to -5% y/y (albeit the 12-month sum is still up by 5% y/y).

Sep home loans boom 5.9% m/m, & 38% since May; upside to credit growth

Home loans are a key lead indicator of house prices & credit growth. Loans (excluding refinancing) boomed another 5.9% m/m in September (UBS: -3%), after a record 12.6%; rebounding an incredible 38% since May, to the 2nd highest monthly level in history (after the record high in Mar-17 before the credit tightening occurred). The y/y also lifted to 25.5%, the fastest since 2013 (after +19.3%). The m/m rise in September was broad-based. Owner-occupiers are strongest (6.0%, 33.8% y/y), with renovations bouncing (5.5% m/m, 6.2% y/y). Investors also recovered (5.2%, 4.2% y/y). Total First Home Buyer loans skyrocketed again (12.4% m/m and 51.2% y/y), to a cycle high share of total loans at 25.2%, amid the very significant policy stimulus. If sustained, this suggests housing credit growth will continue to tick-up (despite faster pay-downs). Overall, despite the strength of housing, the RBA will still likely cut rates tomorrow, given their material shift towards focussing on the labour market as a policy driver.

All HomeBuilder driven. Given it ends at the end of the year that will be a problem.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.