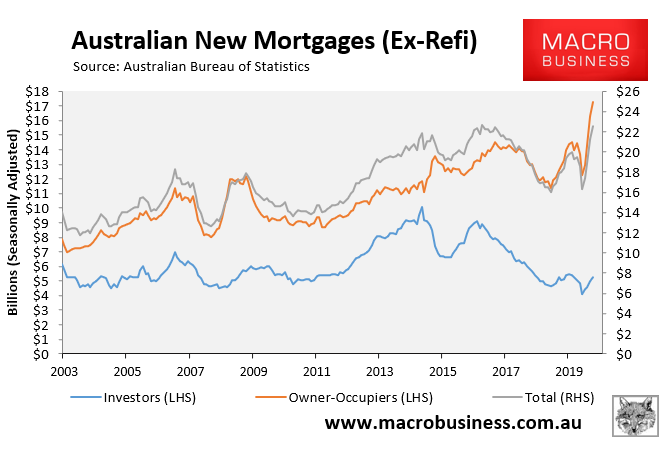

Strong mortgage growth bullish for property prices

Yesterday’s mortgage finance data from the Australian Bureau of Statistics (ABS) was unambiguously strong, driven by owner-occupiers:

Total new mortgage commitments (excluding refinancings) rose by 25.5% year-on-year in September, driven by a whopping 33.8% growth in owner-occupier mortgage commitments versus 4.2% growth in investor commitments.

As regular readers know, mortgage growth is one of the best indicators for property price growth having displayed a very strong historical correlation.

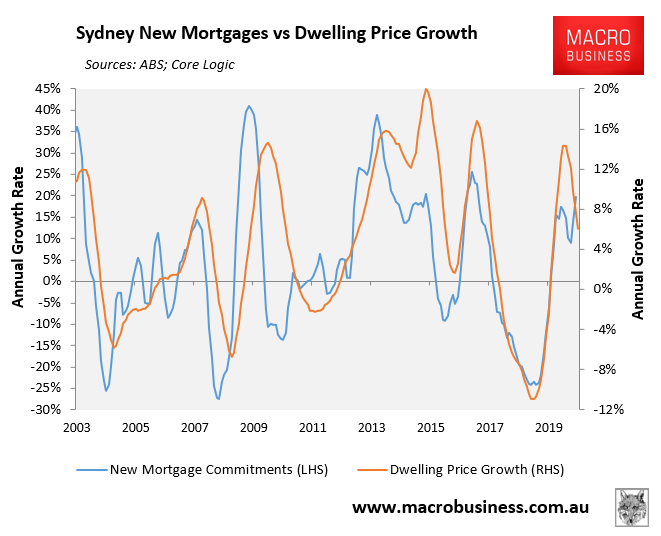

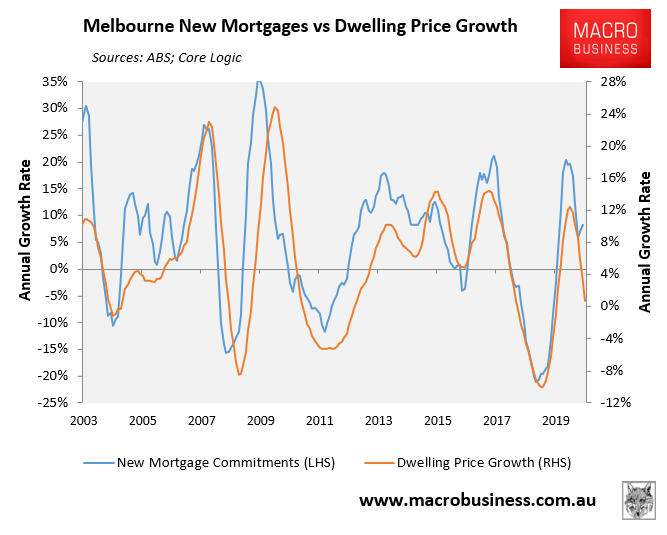

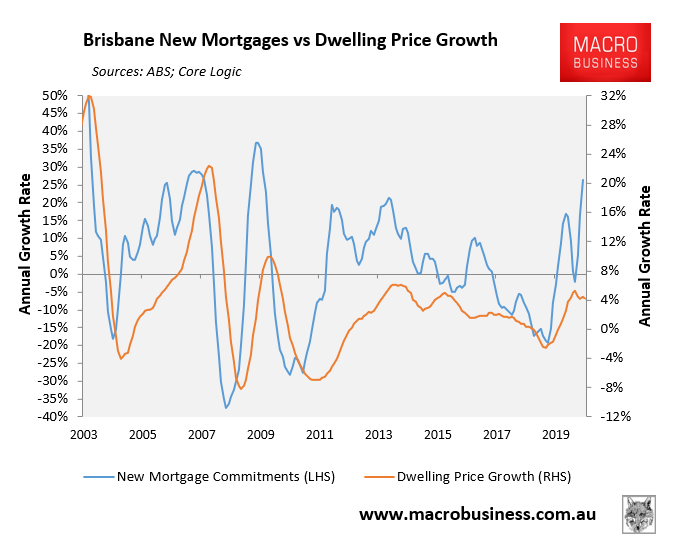

Below are charts plotting the annual value of mortgage growth (excluding refinancings) against annual dwelling value growth.

First Sydney:

Next Melbourne:

Next Brisbane:

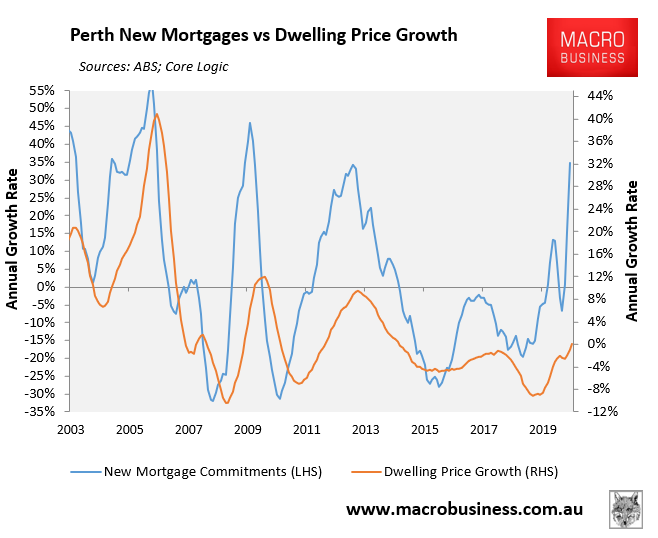

Next Perth:

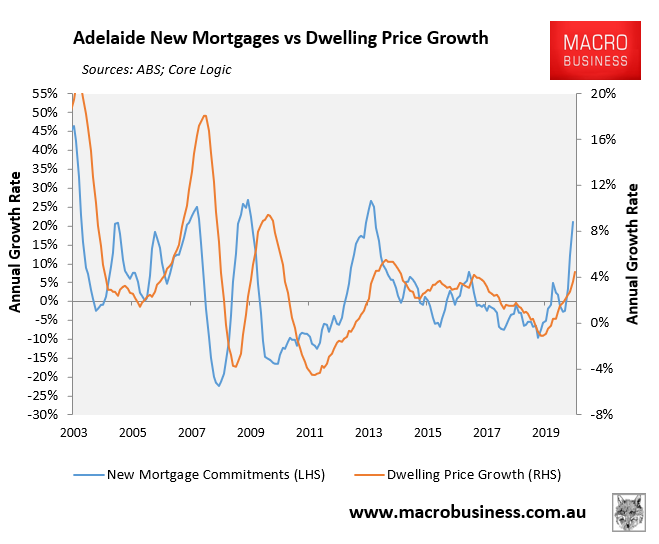

Next Adelaide:

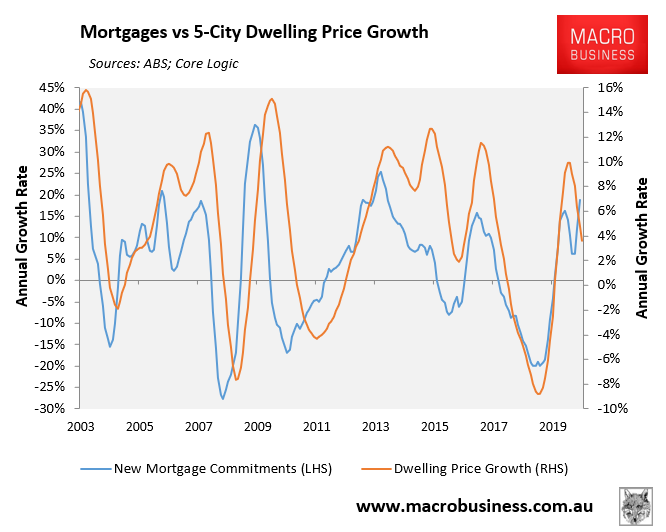

Finally, below is the 5-City aggregate:

As shown above, the mortgage rebounds have been strongest across the smaller three capitals, which is also reflected in their recent price rebound:

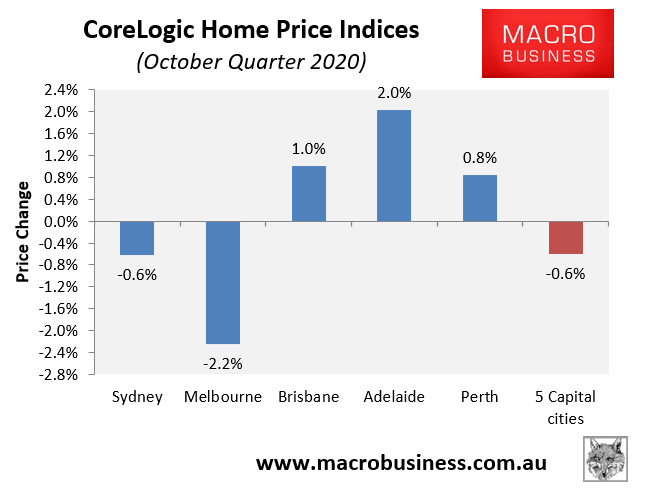

Brisbane and Perth are looking especially enticing.

By contrast, Sydney’s mortgage market has only experienced a moderate rebound, pointing to moderate growth, whereas Melbourne’s remains soft.