Data from RateCity shows that banks have slashed deposit rates since the RBA’s latest interest rate cut, with the average ongoing savings rate across the banking system now just 0.46%:

According to RateCity, 30 banks have taken a knife to interest rates since the RBA cut, with the average ongoing savings rate across the banking sector now sitting at 0.46 per cent.

Westpac is advertising the highest conditional savings rate out of the big four at 0.75 per cent, while Commonwealth Bank is offering the lowest at 0.45 per cent.

Both Westpac and NAB are advertising the highest introductory rates on standard deposit accounts at 0.75 per cent.

Ms Tindall said it was only a matter of time before NAB and Westpac were forced to drop rates.

“It’s not easy operating in a low-rate environment where profit margins are feeling the squeeze, but there aren’t many winners on the back of this month’s rate cut,” Ms Tindall said. “Savings rates are under fire”…

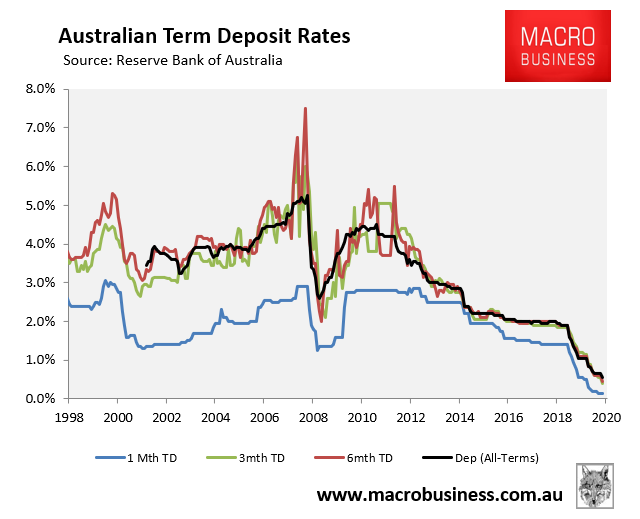

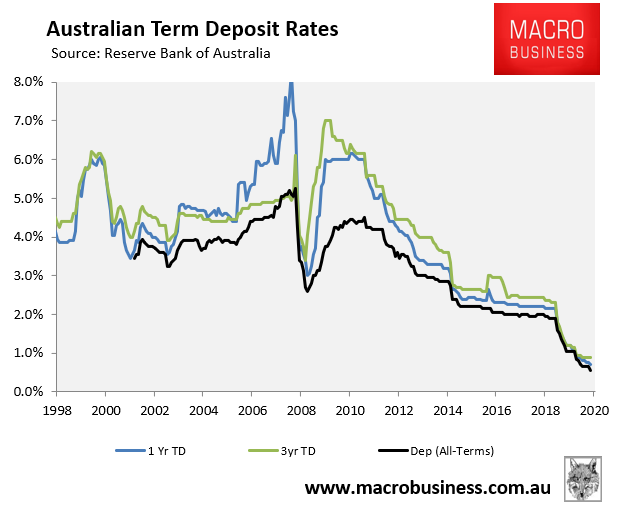

The below charts, which use aggregate deposit data from the RBA, illustrates the compression of deposit rates across various terms:

It sure does suck to be a saver right now.