From Gareth Aird, head of Australian economics at CBA:

Key Points:

The RBA has upgraded their assessment of the Australian economic outlook.

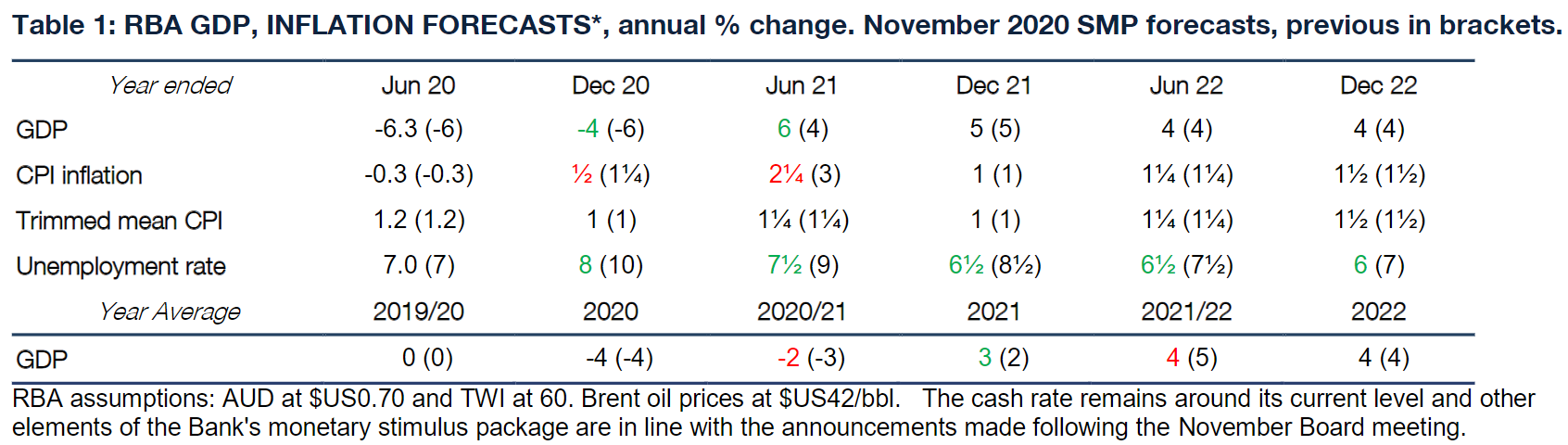

The RBA’s central scenario sees GDP contract by 4% in 2020 and to rise by 2% in 2021 and 4% in 2022.

The RBA has materially lowered their profile for the unemployment rate –it looks a lot closer to our profile now.

Underlying inflation forecasts are unchanged and the trimmed mean is forecast to be below 1½%/yr until H2 22.

The RBA Board is not contemplating a further reduction in interest rates and a negative policy rate is still considered “extraordinary unlikely”.

Any further easing in monetary policy from here will involve more bond buying than what has currently been announced.

The RBA Board meeting on Tuesday was the big domestic event this week. Expectations were high that the RBA would announce a suite of measures to ease financial conditions and the central bank duly delivered. The package comprised lowering the cash rate target, the target on the 3-year Australian Government bond yield and the term funding facility rate all to 10 basis points (from 25 basis points). And the RBA also announced a quantity based asset purchase program that involves buying $A100bn of Australian Commonwealth Government Bonds (ACGBs) and Semi-government bonds of maturities of around 5-10 years over the next six months. We covered the RBA decision in detail on Tuesday.

The November Statement on Monetary Policy(SMP) is not a document that needs to be read through the lens of looking for clues around the near term direction for monetary policy given the RBA’s suite of easing measures announced at the November Board meeting. Rather the SMP gives us an insight into the RBA’s views on the economic outlook and how their assessment has evolved over recent months.

There is still considerable uncertainty around the economic outlook as COVID-19 has not gone away. Until there is a vaccine the potential for the reimposition of restrictions and lockdowns remains the key source of risk to the economic outlook. Indeed many parts of Europe are now going through a new round of lockdowns which has profound negative economic consequences. Fortunately the situation in Australia around COVID-19 is positive and this has facilitated a further easing of restrictions which will support economic activity and job creation. Notwithstanding, risks remain.

Despite easing policy at the November Board meeting the RBA has upgraded their near term assessment of the economic outlook, as expected.

The RBA’s updated central scenario for GDP to contract by 4%/yr to Q4 20 is now similar to our near term profile (note that the RBA rounds GDP growth to the nearest whole number). The RBA’s forecast implies a rebound in GDP of ~3½% over H2 20 which is what we expect (note that we upwardly revised our numbers in mid-September). The RBA’s economic growth profile from there looks broadly unchanged in percentage terms. But the upward adjustment to GDP over H2 20 raises the level of GDP over the entire forecast period which means the profile for the unemployment rate must be lowered over the forecast horizon.

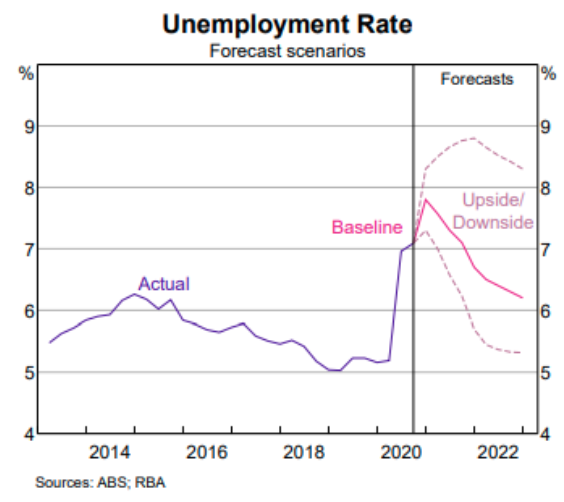

On that score, the RBA has made large downward revisions to their unemployment rate profile. It now looks a lot like our profile in the outer years, although even with these revisions we are still more constructive on the labour market. The RBA expects the unemployment rate to peak at a little below 8% (vs 10% previously) and to be at 6½% by end-2021. We have the unemployment rate at 6¼% at end-2021. And we think the risks are titled towards an unemployment rate below 6% by end-2021 given the huge fiscal stimulus and massive amount of savings buffers accrued by the household sector over the last six months that can be deployed to support consumption and by extension employment (we estimate savings have been accrued worth 5% of GDP over the past six months and that excludes the early withdrawal of superannuation).

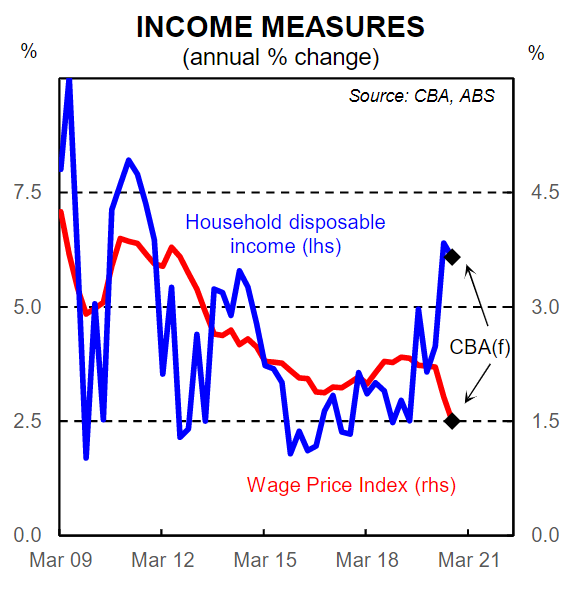

The trajectory for underlying inflation has been left unchanged and the message from the RBA remains the same. The economy will have a large output gap over the forecast horizon as evidenced by an elevated unemployment rate. This means that wages growth and underlying inflation will stay very low. We very much agree in terms of our central scenario. Indeed modelled underlying inflation, which we base our central scenario on, points to inflation remaining below 1¼%/yr until mid-2022 (currently the end of our forecast horizon). However there is upside risk to modelled inflation because there is a large disparity at present between wages growth and household income growth. The longer this disparity persists the greater the risk that inflation outcomes are higher than modelled inflation would imply (see pages 2-3 for more details on our modelled inflation).

It is worth nothing that the RBA’s forecast profile for inflation is now less important for the outlook for monetary policy than previously. That is because Governor Lowe recently stated that, “will now be putting a greater weight on actual, not forecast, inflation in our decision-making”. This is a significant shift. The RBA once again provided upside and downside scenarios in addition to their central scenario. See page 2 for a discussion on these additional scenarios. From a monetary policy perspective the RBA Board is not contemplating a further reduction in interest rates and a negative policy rate is still considered “extraordinary unlikely”. Any further easing in monetary policy from here will involve more bond buying than what has currently been announced. That said, further easing is not on the near term horizon given what the RBA announced at the November Board meeting. Policy is on hold at the December Board meeting and the RBA Board does not then meet until February 2021.

Scenarios

Since the COVID-19 pandemic hit the RBA has presented an upside and downside scenario when discussing their forecasts for the economy in the quarterly SMPs.

The main change between the scenarios is around the assumption on the path of COVID-19. The downside scenario assumes that there are further virus outbreaks in Australia and a loss of control of the virus in other countries. Under this scenario restrictions are reimposed domestically and internationally slowing the recovery in consumption and business investment. Under this scenario the unemployment rate would peak at around 9% in late 2021 and fall just a little in 2022.

The upside scenario assumes the faster control of the virus domestically and globally and a faster wind-back of restrictions. Under this scenario consumption, business exports and services exports rebound faster than under the base line scenario. The unemployment would be projected to peak at 7½%before falling to 5½% by the end of 2021.

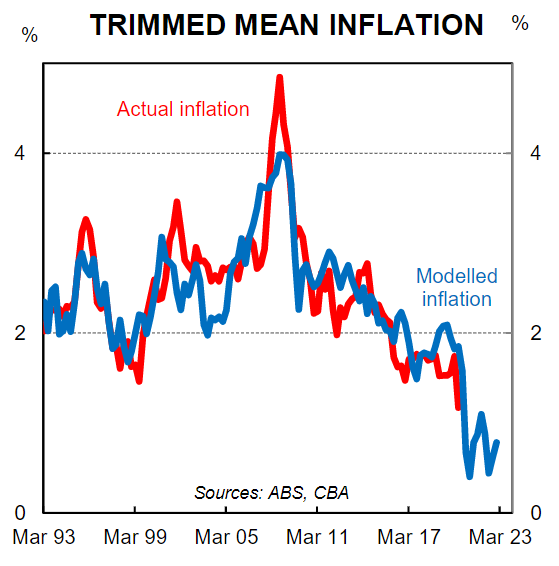

A model for inflation

Our model for trimmed mean inflation, the RBA’s preferred underlying inflation measure, shows a further drop in the annual rate of inflation over the next few quarters. The model shows the trimmed mean remaining at a low level thereafter and well short of the RBA’s 2-3% inflation target.

Our model includes inflation expectations, the labour market underutilisation rate and import prices. We expect underutilisation to gradually recede as the economy recovers but still remain elevated over our forecast horizon. Less slack in the labour market will add to inflationary pressures as wages growth should lift a little. However working the other way we are forecasting an appreciation of the Australian dollar over the next year which will reduce import prices. Lower import prices tend to reduce inflation. Inflation expectations are expected to remain soft.

While our model suggests that inflation will remain very low the risk lies towards stronger outcomes. The huge amount of government stimulus in play is boosting household income. If government stimulus continues for long enough we could see inflation pressures build because of strong income growth even as labour market slack remains elevated and wages growth soft. This is not our central scenario but it is a dynamic worth watching out for and one that we continue to reiterate to our readers.

The RBA’s baseline forecasts show trimmed mean inflation hovering around 1-1¼% over most of the forecasting horizon, a little higher than our model predicts.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.