Eliza Owen, head of research at CoreLogic, has released a report explaining how owner-occupiers and first home buyers are driving Australia’s housing rebound:

The volume of finance secured for the purchase of property experienced a strong rebound in the September quarter, following the initial shock to demand for housing in the first two months of the June quarter.

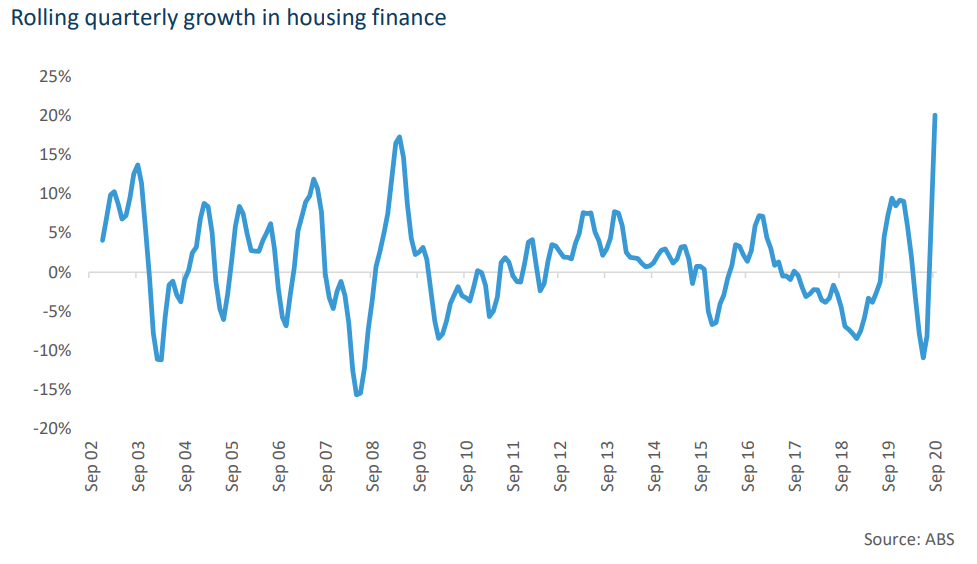

The latest ABS housing finance data shows the volume of finance lent for the purchase of property increased 5.9% in the month of September, taking the quarterly increase to 20.0%, the highest quarterly growth rate on record. It follows a 10.9% contraction in housing finance through the June quarter, when strict social distancing restrictions, such as a ban on open home inspections and on-site auctions, resulted in a sharp drop in transactions.

Housing finance for the purchase of property totalled $62.7 billion in the September quarter. This is the highest level since the March 2018 quarter, and is just 6.6% below the peak of the lending series in the three months to May 2017.

The uptick is a result of eased social distancing restrictions across the country, which have coincided with historically accommodative monetary policy, which sees mortgage rates at a record low.

As with the strong bounce-back in many economic indicators over the September quarter, eased social distancing led to a rise in consumer sentiment and an increase in sales and listings volumes. CoreLogic estimates that sales volumes increased around 27.7% in the quarter, despite renewed restrictions across Victoria.

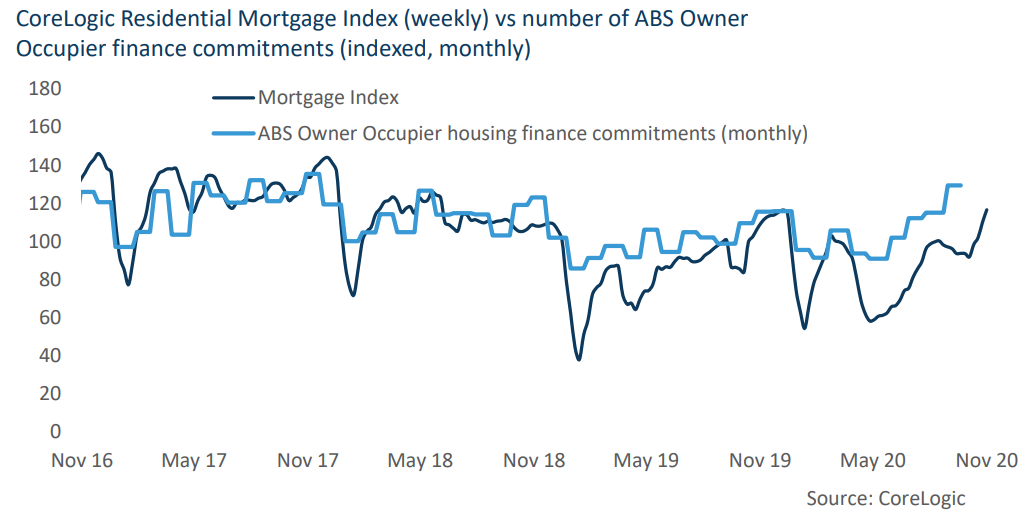

The CoreLogic Residential Mortgage index (RMI) indicates further increases in housing finance over October and November. The RMI tracks changes in valuation activity across CoreLogic platforms for the purpose of dwelling purchases. In the 28 days ending 8th of November, the CoreLogic RMI rose 26.9%. As can be seen in the chart below, the RMI is a leading indicator of monthly ABS housing finance commitments in the owner-occupier segment.

Queensland leads growth in housing finance

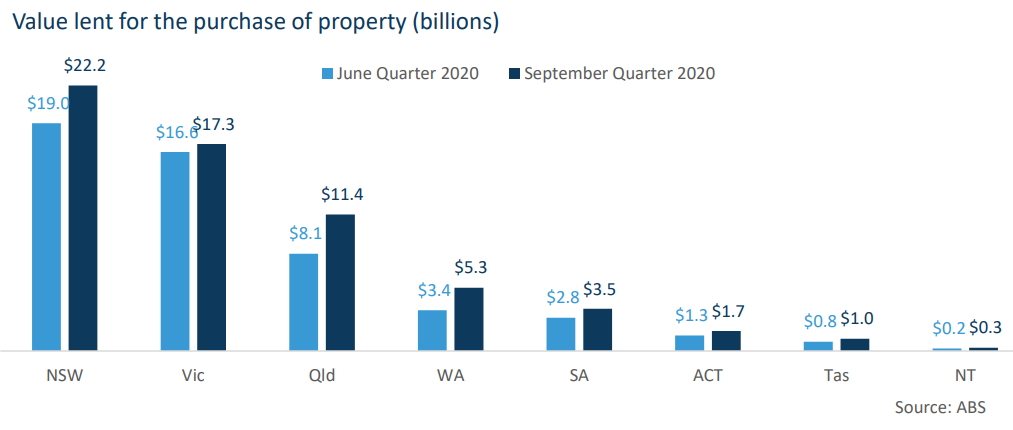

Of the states and territories, Queensland accounted for most of the increase in lending for the purchase of property. The value of housing finance commitments (excluding refinancing) increased 40.2% in Queensland over the September quarter, accounting for around 31% of the uplift in finance nationally. This was followed by NSW, which contributed 30% to the uplift nationally, as the state saw a 16.7% increase.

Western Australia had the largest increase in housing finance for the purchase of property over the September quarter, rising over 55%. This further supports the view that the WA and Perth dwelling markets are resuming an upswing following the disruption of COVID-19.

Despite extended restrictions on the transaction of property across Victoria for much of the quarter, the state still saw a 4% uplift in the value of finance for the purchase of property, which was entirely fuelled by owner-occupier purchases. Finance secured for the purpose of investment property purchase fell -4.3% across the state in September.

ABS data suggests external refinancing came down 9.6% over the quarter, after an unprecedented peak in May. However, the value of external refinancing is still elevated, and is 30.4% higher than in the September quarter of 2019.

As the RBA handed down a further reduction in bank funding costs over November, and mortgage rates continued to fall, refinancing should remain elevated. But it is worth noting the vast majority of discounted funding costs for banks are being passed through to fixed rate loan products. The exit fees that can be associated with fixed rate home loan arrangements may constrain refinance activity down the line, once a portion of the current wave of borrowers are locked into fixed-rate arrangements.

In the near term, CoreLogic estimates lending for the purchase of property will continue to remain elevated due to loose monetary policy. However, the steep increases in finance seen in recent months is unlikely to maintain such a strong trajectory, and quarterly growth rates in housing finance volumes are likely to slow as pent-up demand runs out of steam.

Owner occupiers continue to dominate lending

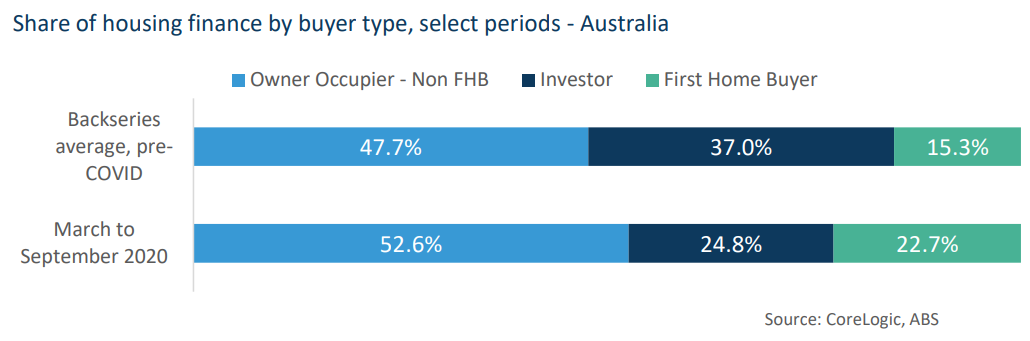

An increase in secured finance (excluding refinancing) to owner occupiers accounted for 85.6% of the uplift in money lent for the purchase of housing in the September quarter. The owner occupier, first home buyer cohort had the highest rate of growth in secured finance, at 24.4% in the quarter. This compares with an uplift of 23.1% for changeover owner-occupiers and an 11.3% rise in investors.

It is worth making the distinction that while first home buyers had the fastest growth in lending over the quarter, the majority of secured finance (53.1%) still went to ‘change over’ owner occupier buyers, such as upsizers and downsizers. A summary of the composition of lending since the onset of COVID-19 in March is compared with the back series average below, which starts in July 2002.

Investor participation in the housing market has been trending down since a national property market downturn in 2017. The retreat of investors and the rise of FHBs has only been exacerbated by COVID-19, as risk in investor-grade stock became elevated, and government stimulus targeted the construction of new homes and grants for FHBs. FHB purchases may be limited late next year, as temporary grants and concessions wind down, and house prices rise off the back of low mortgage rate settings.

In contrast, we could see a lift in investor participation as prospects for capital gains solidify, providing a further incentive for investors, along with more properties returning a positive cash flow thanks to such extremely low interest rates.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.