…investors were a bit too complacent on the uncertainty surrounding the election outcome, unlikely passage of a fiscal stimulus before the election and second wave of Covid-19…the short answer is that the worst of the correction is over in our view but we still think the next month is likely to remain volatile and uncertain as we navigate what is shaping up to be a much closer election than expected just a few weeks ago and risk of further lockdowns as the virus runs its course.

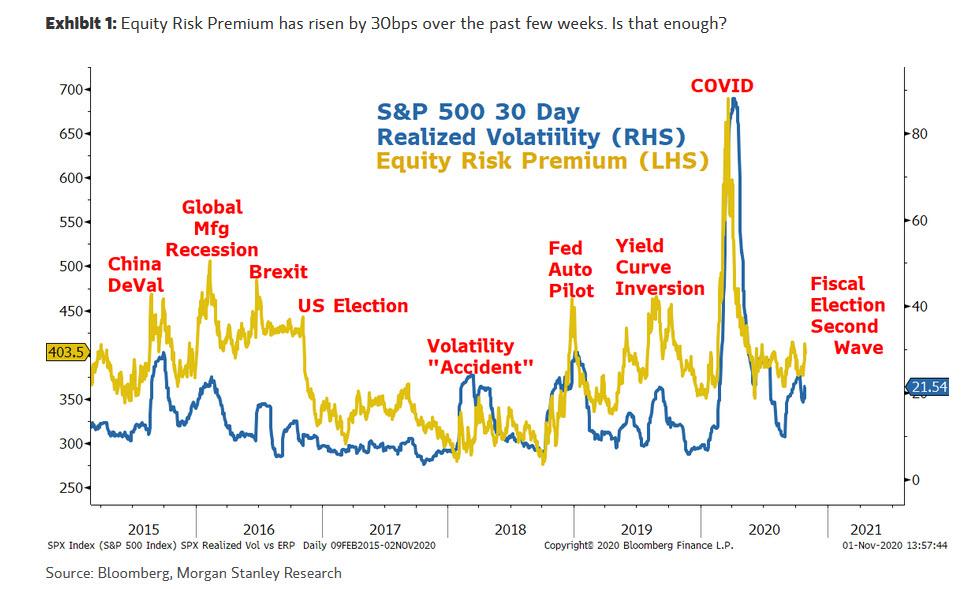

…a key part of his bearish call was based on the view that the equity risk premium should have a larger buffer built in given these very visible risks/events. Fast forward to today and that’s exactly what’s happened, with the Equity Risk Premium widening by approximately 30 bps to 405 bps from the 375 bps level when he made his first call. At the same time, with interest rates remaining steady rather than falling as they typically do when equity markets sell off, the P/E has compressed by approximately 10%.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.