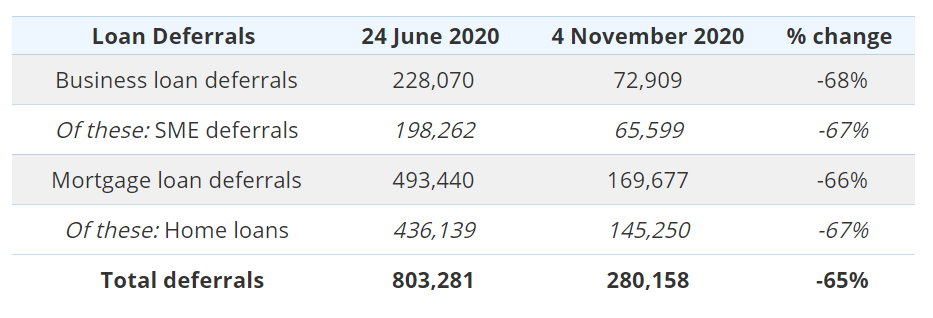

The Australian Bankers Association (ABA) has provided an update on its members deferred loans, which shows that the mortgage cliff that was towering over Australia’s property market has shrunk by two-thirds from its peak in June:

According to the latest data up to November 4, home loan deferrals by the seven largest banks are down to fewer than 145,000…

The number of loans on hold is expected to fall further in coming weeks as more reach the end of their six-month deferrals…

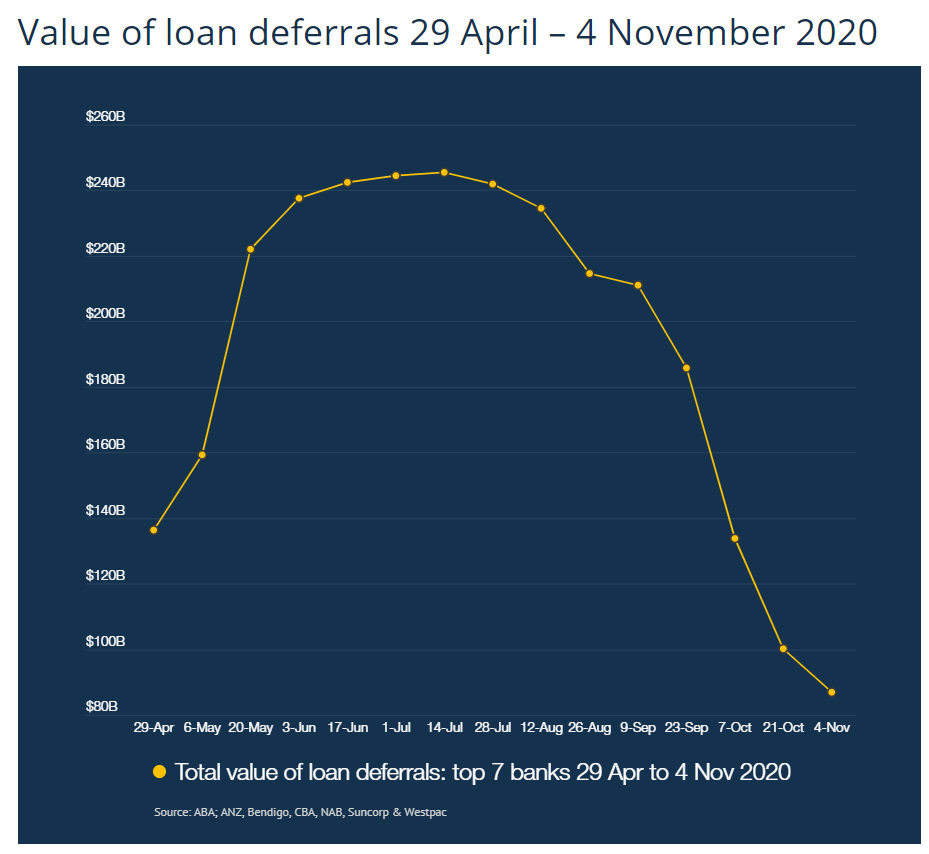

The value of deferred loans by the seven largest banks has now fallen below $100 billion – down to $86 billion. This figure peaked at more than $250 billion in June.

Clearly, the risks to the property market and economy have receded significantly over recent months.

While we are still likely to witness some stress at the margins, especially once income support measures are unwound early next year, the ‘mortgage cliff’ is no longer a systemic threat.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.