When it comes to successful lobbyists, you would be hard pressed to beat Australia’s superannuation industry.

Despite strong arguments against, the overwhelming majority of Australians still support increasing Australia’s superannuation guarantee (compulsory superannuation) to 12%:

A new independent report compiled on behalf of the Association of Superannuation Funds of Australia surveyed 1400 Australians aged 18 to 65 and found the following:

• 75 per cent say the superannuation guarantee (SG) rate should rise to 12 per cent by 2025.

• 52 per cent believe they will rely on a mix of super, savings and the age pension.

• 43 per cent are not confident they will have enough super and savings in retirement…

The report also found 75 per cent of people say they would struggle to live comfortably on the age pension alone.

The age pension remains at the same fortnightly base rate of $860.60 for a single person or $22,375 a year.

MB has long opposed lifting the superannuation guarantee to 12%, believing that it is expensive, inefficient and inequitable.

Specifically, we see the following key flaws in the system, which would be exacerbated by lifting the superannuation guarantee:

1/ Superannuation is voluntary for those that are self-employed or homemakers. It, therefore, misses millions of people.

2/ Superannuation can be spent at age 60 – many years before the official retirement age of 66 (rising to 67).

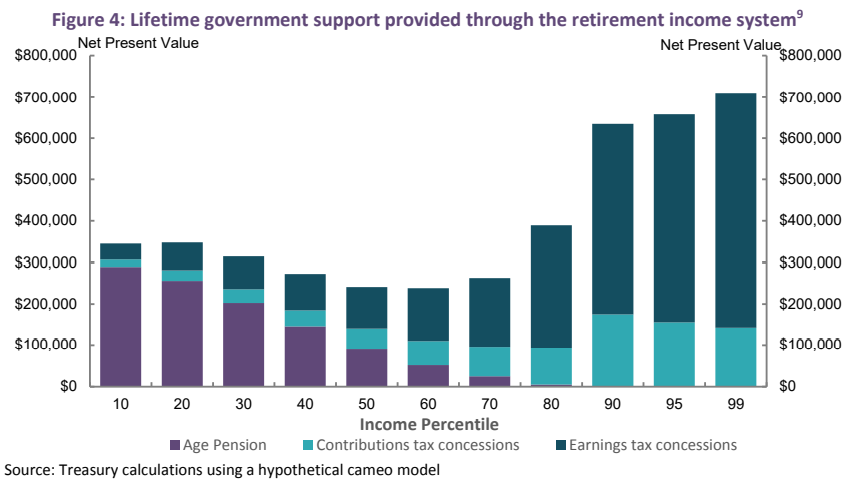

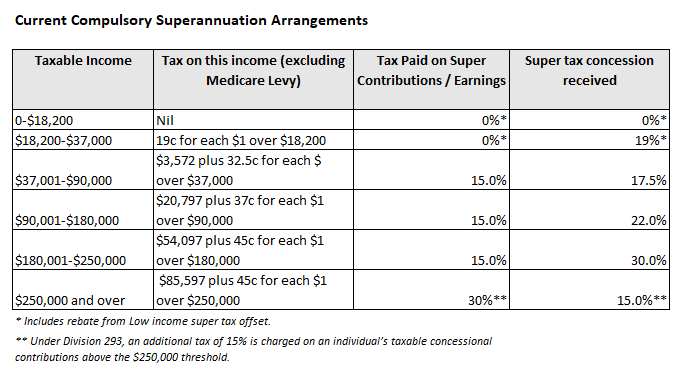

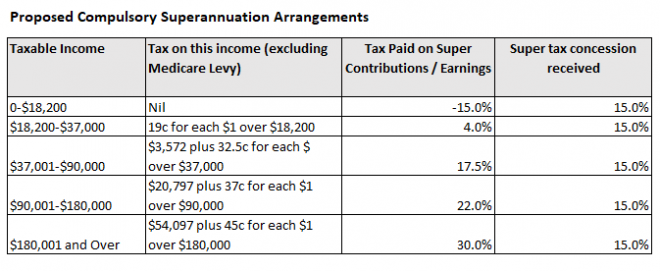

3/ Most superannuation concessions go to where they are not needed, i.e. high income earners:

4/ Superannuation balances at retirement depend on how long one works and how much they earn. In turn, superannuation misses lower income earners and those with broken work patterns.

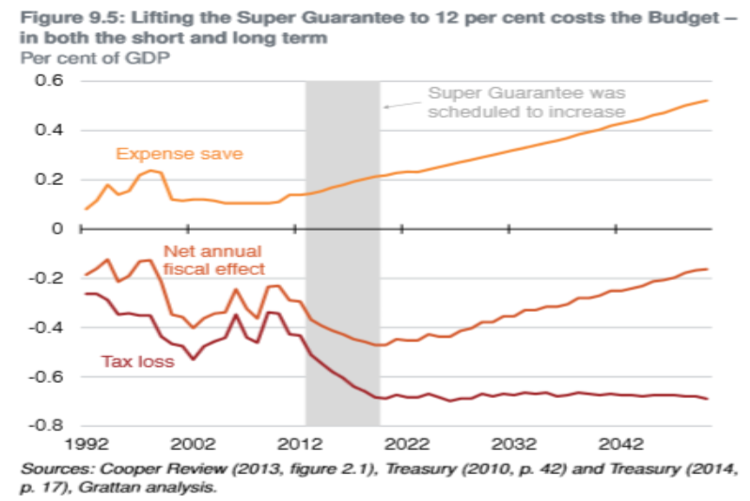

5/ Compulsory superannuation costs the federal budget $43 billion a year. This is more than superannuation saves in aged pension costs:

6/ Compulsory superannuation lowers wage growth. This is especially bad for lower income earners struggling to pay bills.

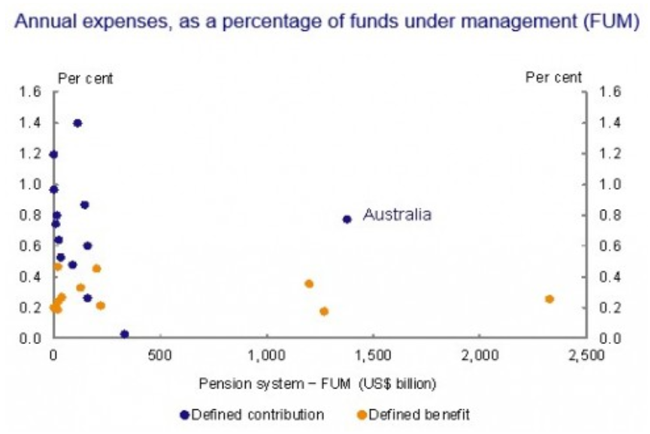

7/ The superannuation system is highly inefficient. Management fees among the highest in the world with Aussies spending twice as much on fees as electricity each year:

8/ Superannuation nest eggs are subject to market risks.

The Australia Institute’s chief economist, Richard Denniss, summed up the problems nicely last year:

Welcome to the topsy-turvy land of superannuation, in which taxpayers give the most assistance to those who need it least, and no assistance to those who need it most. John Oliver once said: “If you want to do something evil then put it in something boring.” If those responsible for managing our life savings weren’t so brilliant at making superannuation seem so boring, there would be riots in the street.

Much is made of the enormous size of Australia’s $2.9tn pool of superannuation savings, but we talk much less about the fact that the only reason it grew so big was that we literally force the vast majority of employees to spend 9.5% of their income buying superannuation every week. Let’s be clear: if we forced all Australians to get a massage every week or buy a new Australian car every year, we would have an enormous massage and car industry as well…

We hand out $43bn a year in tax concessions for super. It’s obscene and it only survives because the superannuation industry is so skilful at confusing people, boring people, or both…

Tax concessions for superannuation literally amplify inequality in Australia.

According to ASFA’s survey, 75% of people support lifting the superannuation guarantee because they believe they will struggle to live comfortably on the age pension alone. But these same people don’t realise that the reason that we cannot afford to lift the age pension is because we spend so much on poorly targeted superannuation concessions (i.e. $43 billion a year in 2019).

Lifting the superannuation guarantee to 12% will obviously increase the cost to the federal budget and make it even harder to raise the aged pension.

An obvious solution to improve both equity and federal budget sustainability would be to abandon raising the compulsory superannuation guarantee and instead replace the 15% flat tax on contributions/earnings with a flat-rate refundable tax offset (e.g. 15%):

This way, everyone that contributes to superannuation would receive the same tax concession, the system would be made progressive, and lower income earners would get a better deal.

But doing so would also deprive the industry of extra funds under management and the chance to earn fatter fees. Therefore, they continue to lobby for an increase in the superannuation guarantee to 12%, despite its deleterious impacts on the federal budget, wage growth, and inequality.