Mortgages are going nuts!

All I can say is: who cares. Why would I say that after years of fighting the bubble?

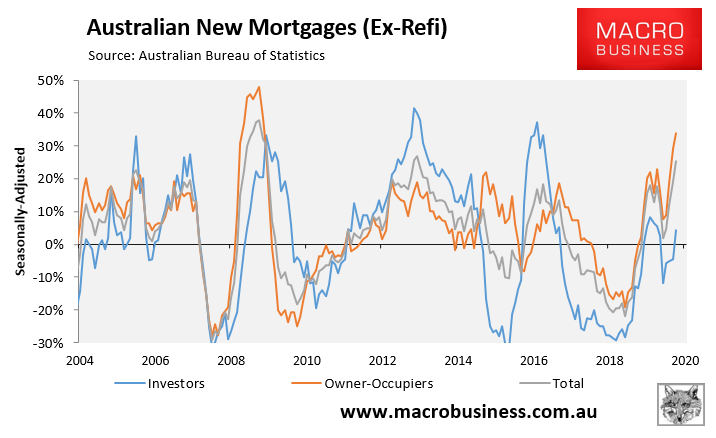

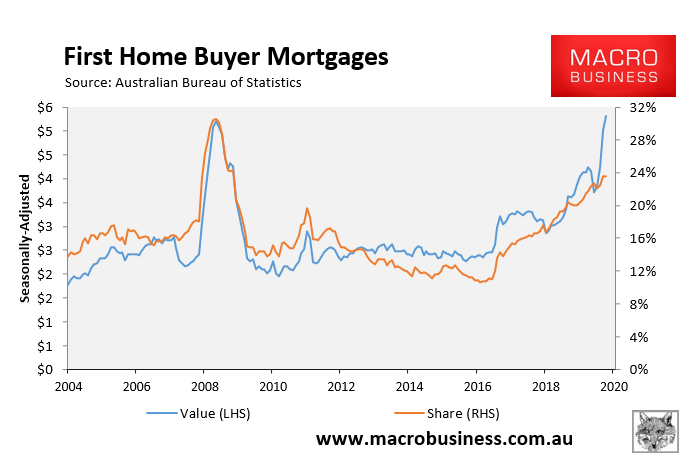

A few reasons. First, this is an owner-occupier boom. What has so incensed me about previous booms is that they’ve been manifestly unfair driven at various stages by rent-seeking investors, Chinese blood-money or mass immigration.

None of these are true today. This is an owner-occupier and first home buyer boom:

If ordinary Aussies want to blow a new house price bubble then who am I to stop them? It’s cheaper to buy than rent so why not.

Second, it may be stupid to inflate more bubble but it’s no longer hollowing out the economy. Australia is a global price taker on interest rates and we’ve finally gotten monetary policy to where it needs to be at zero with QE, so the Australian dollar is not artificially inflated anymore. Moreover, the last house price boom saw little activity spillovers and neither will this one so the AUD will stay weak.

Third, in part owing to the first two, I still don’t see any kind of national price boom. Sydney and Melbourne have huge oversupply. Other capitals look much better. Brisbane especially looks strong. Perth will crash again before long as iron ore corrects into a new bear market, and if others run who cares. They’re peripheral and no financial stability threat.

Fourth, through pure dumb luck, Australia has managed to negotiate its period of massive offshore borrowing imbalance without a crisis. Now we have the monetary settings that we need, offshore debt is being eaten by the RBA and the risk of external crisis is gone.

In short, the Aussie property bubble is a shadow of its former self:

- It no longer does so much harm to equity.

- It does much less economic harm to tradaeble sectors (though land prices remain an issue).

- It no longer creates enormous financial stability risk.

- It no longer pushes us towards China.

Sure, it’s still a big problem. The bubble has engulfed the political economy to mitigate all of these risks, and I will keep fighting it on this basis. But it is slowly but surely dying and will keep doing so as bank margins collapse permanently into the arms of the taxpayer. There is no coming back from this. The Australian banks are being nationalised in the march to 50bps mortgages.

That’s the rub. The Aussie property bubble is running its last fateful race without a lot of the much wider economic fallout that has tortured the right-thinking for two decades.

Pass the popcorn, I say!