The Consumer Policy Research Centre (CPRC) has partnered with Roy Morgan Research to conduct monthly surveys measuring the financial impacts and consumer experiences of COVID-19 across essential and important services markets, including housing, energy, telecommunications, credit and insurance.

The September Report has just been released which shows that around half of Australian renters are experiencing financial stress:

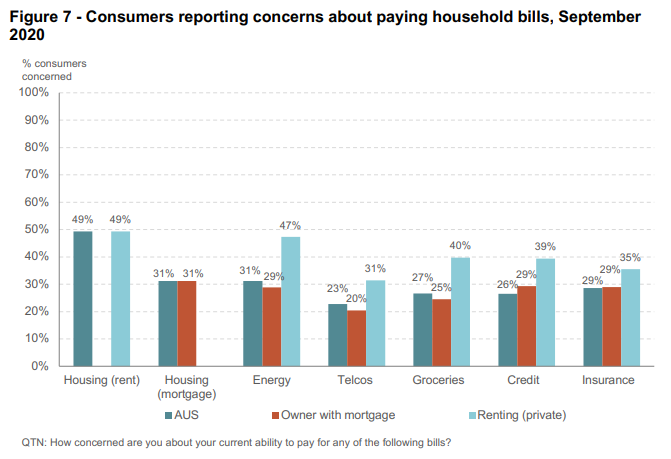

Rent payments were far and away the bill payment causing the most concern among all Australian consumers in September. Almost half of all renters (49%) were concerned about making their rental payments – with 1 in 5 renters very concerned (19% – not shown in figure 7). This contrasts with 31% of mortgage holders reporting concerns about making loan repayments – with far fewer very concerned (6%). We note that energy bill payments were an equally prominent concern for all consumers – also at 31%.

Our September survey results reveal a stark contrast in the specific concerns of renters and mortgage holders regarding their household bills:

• 47% of renters expressed concern about affordability of energy bills, compared with 29% of mortgagors (31% national average)

• 40% of renters expressed concern about affordability of groceries compared with 25% of mortgagors (27% national average)

• 39% of renters reported concern about their ability to pay their credit repayment bills compared with 29% of mortgagors (26% national average)

These comparisons align with the survey results shown in Figure 2 whereby 76% of renters reported they were somewhat or very concerned about their financial wellbeing, compared to 64% of owners with a mortgage.

A higher proportion of renters relying on debt and informal supports to get by, compared with mortgagors

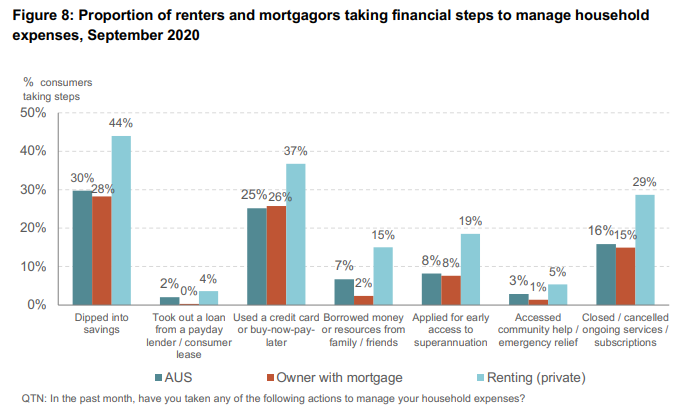

Almost three quarters of (72%) of renters reported taking financial steps to try to manage household expenses in September, compared with approximately half (51%) of national population and mortgagors (49%). As shown in Figure 8, the “steps” most commonly taken amongst renters were:

• 44% of renters dipped into savings compared with 28% of mortgagors (30% nationally)

• 37% of renters used credit/BNPL compared with 26% of mortgagors (25% nationally)

• 29% of renters closed or cancelled a service or subscription compared to 15% of mortgagors (16% nationally)

• 19% of renters accessed super early compared with 8% of mortgagors (8% nationally)

Higher proportion of renters taking action to manage bill payments

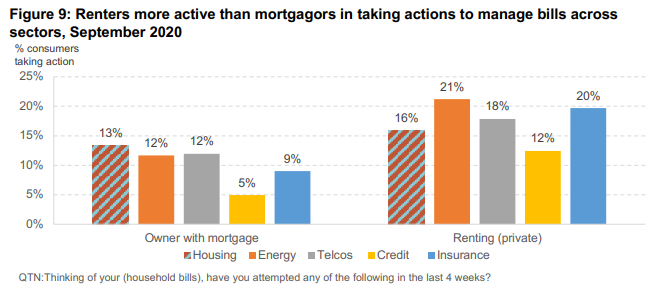

Higher bill and financial concerns seem to be translating into much more action (such as switching plans, providers or seeking payments assistance) from renters with their essential service providers.

Across all sectors, a larger proportion of renters took action to manage household bills compared with owners with a mortgage (Figure 9):

• 21% of renters took action to manage their energy costs (12% of mortgagors)

• 20% of renters actively managed their insurance costs, at more than twice the rate of mortgagors (9%)

• 18% of renters took action to manage their telco costs (12% of mortgagors)

• 12% of renters took action to manage their credit, more than twice that of mortgagors (5%)

• 16% of renters took action to manage their housing costs (13% of mortgagors)

In terms of specific actions taken, the survey results showed that renters were seeking payment assistance at higher rates than mortgagors across sectors in September. For example:

• 6% of renters sought payment assistance from landlord compared to 4% of mortgagors who sought payment assistance from their mortgage provider

• 8% of renters asked their energy company for payment assistance compared with 5% of mortgagors

• 7% of renters asked both their credit provider and insurance provider for payment assistance, while only 3% of mortgagors asked their credit and insurance provider for payment assistance

In addition to the range of steps taken, a much higher proportion of renters missed household bill payments across all sectors compared with mortgagors:

• 7% of renters missed a payment to their landlord, while only 2% of mortgagors missed a payment to their bank

• 9% of renters missed an energy bill, 3% of mortgagors

• 7% of renters missed a telco bill, 1% of mortgagors

• 10% of renters missed a credit bill, 3% of mortgagors

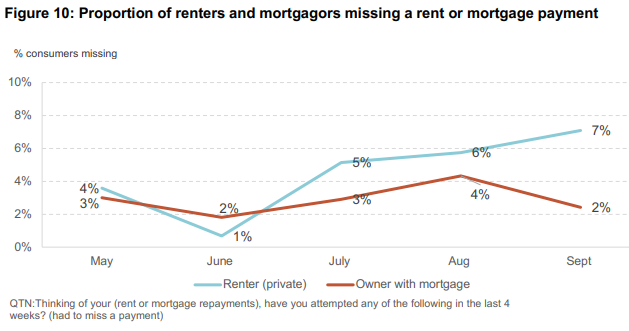

The experiences of renters and mortgagors has changed throughout COVID19 – with missed payments more common for renters from July

Trend data from CPRC monthly consumer surveys starting in May 2020, a reveals a stark contrast in the experiences of renters and home owners with a mortgage during COVID-19. Some differences between renters and mortgagors have been evident from the start of our survey, however other differences have been accentuated as the pandemic has progressed.

For example, the proportion of renters and mortgage holders outright missing rental or mortgage payments diverged after June (Figure 10). Since July, a growing proportion of renters reported missing housing payments compared with mortgagors, with 7% of renters reporting they had to miss a payment in September, well above the 2% of mortgagors who had to miss a payment.

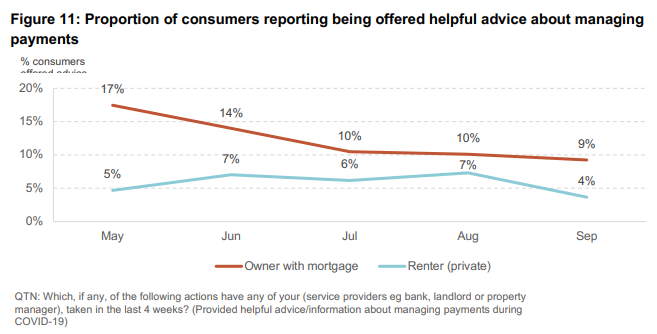

Results also reveal that a far higher proportion of mortgagors have been provided helpful advice about managing payments during COVID-19 compared with renters (Figure 11).

Over one in ten mortgagors reported that helpful information had been offered in each month from May to August, with this dropping to 9% in September. By comparison, a much smaller proportion of renters report their landlord/agent has offered helpful information about managing payment, with reports peaking at 7% in June and August, and dropping to the lowest level recorded at 4% in September.

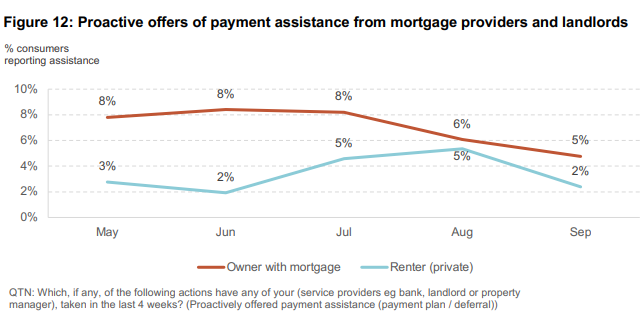

Banks and mortgage providers have also been more proactive in offering consumers payment assistance since the start of our survey in May (Figure 12). In May, 8% of mortgagors reported their mortgage provider proactive offered payment assistance, compared with 3% of renters reporting these actions from landlords / property managers. The proportion of mortgagors reporting offers of proactive payment dipped in August, but has continued to exceed the proportion of renters reporting proactive help in both August and September.

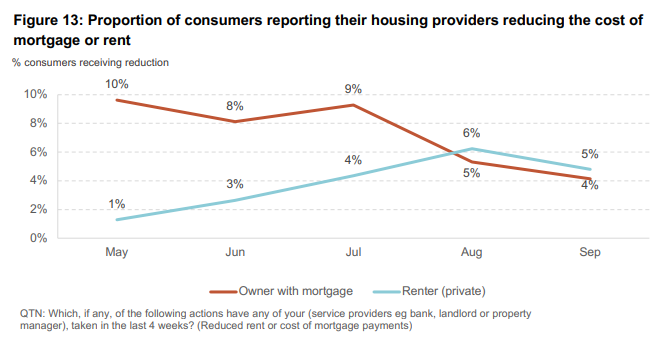

Finally, since the start of our survey in May, there has been a significant difference in the proportion of housing providers reducing the cost of mortgage repayments and rents (Figure 13). In May, 10% of mortgagors reported their provider had reduced the cost of their mortgage repayments, compared with 1% of renters. A large gap between renters and housing providers receiving reduced costs persisted until August – with slightly more renters reporting reduced costs from this time.

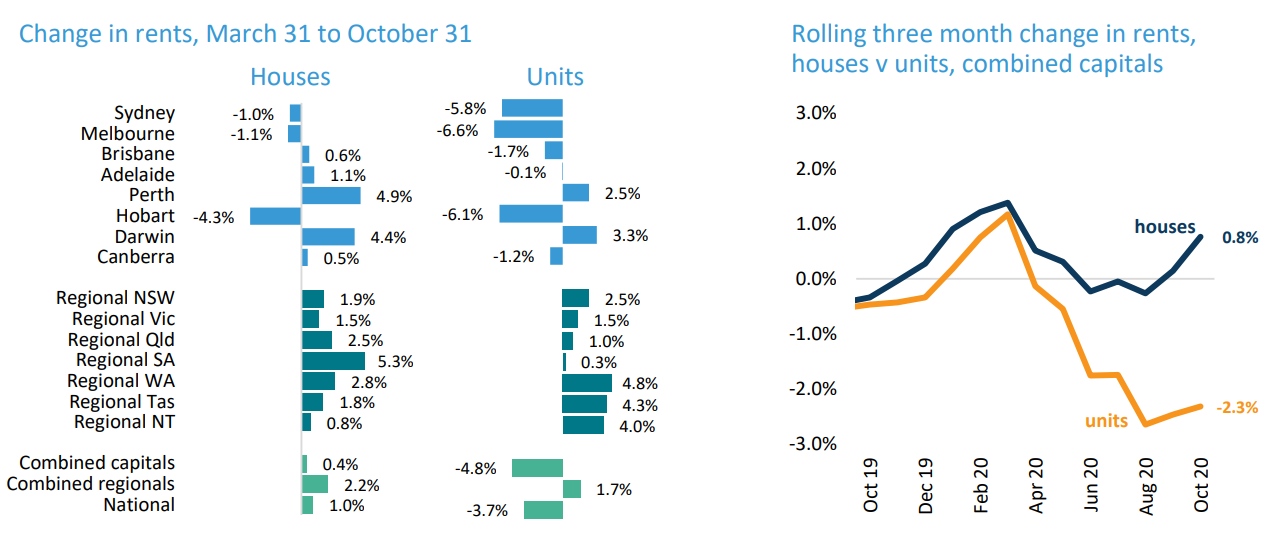

The only consolation is that rents have fallen since March, meaning renters’ costs have decreased:

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.