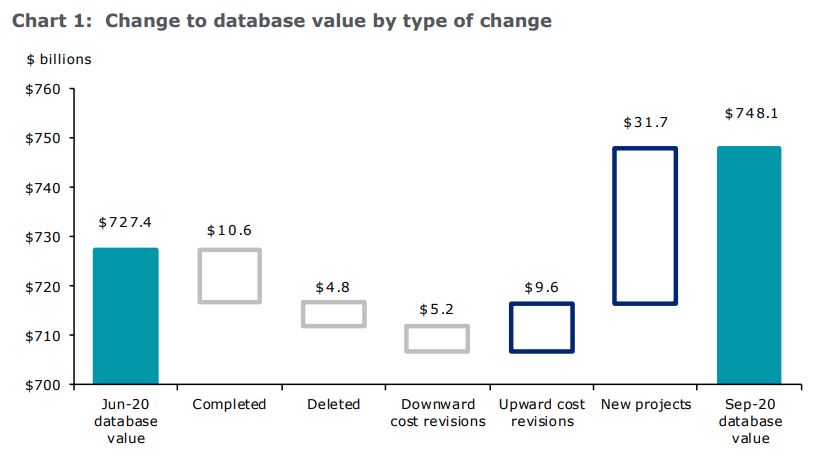

Deloitte Access Economics’ Investment Monitor is primarily a source of information for businesses and others about major engineering and commercial construction projects and their promoters. It is also a barometer of structural change in the Australian economy, and of the investment climate – now and in the future. The database for this edition of Investment Monitor contains details of 1,448 Australian investment projects valued at $20 million or more. The total recorded value of projects in the database is $748.1 billion. This represents a 2.8% increase from the previous quarter, with almost one half of this gain coming from planned transport investment.

Chart 1: Change to database value by type of change

• COVID-19 has created a lot of fear, including among investors. Scared investors don’t invest. And, without investment, we don’t get growth. And without growth, we don’t create jobs. That’s a potentially vicious cycle.

• When the recovery starts, business investment will play an important role. After all, it won’t really be a recovery until businesses are willing to bet on the future by expanding their productive capacity. But how soon will that be? And will things get worse before they get better?

• The key here is the date at which rising sales begin to place pressure on production, meaning that there’s an improving business case to invest. That date will differ from industry to industry and from business to business, but is likely some way off.

• Commercial construction may experience a particularly slow recovery due to the increased adoption of work-from-home practices and a smaller need for retail space because of the growth of e-commerce. More importantly still, this industry is working its way through its existing pipeline of work, but that pipeline isn’t being replaced at anything like a matching pace.

• Engineering construction will also slow, but mining investment will perform relatively well, partly because China’s economy is recovering from COVID-19 quicker than most.

• Overall, private business investment is forecast to fall sharply in 2020 and the decline in investment will exceed the decline in the wider economy. Deloitte Access Economics is forecasting private business investment to return to positive growth in 2021 before accelerating in 2022.

• Government investment is set to reach new heights in the coming years as infrastructure plays a key role in post-COVID stimulus efforts. The 2020-21 Federal Budget announced a further $10 billion for new and accelerated infrastructure projects over the next four years. This brings the total investment by the Federal Government to $14 billion since the outbreak of COVID-19. And there is scope for additional investment from state and territory governments as they release their budgets in the coming months.

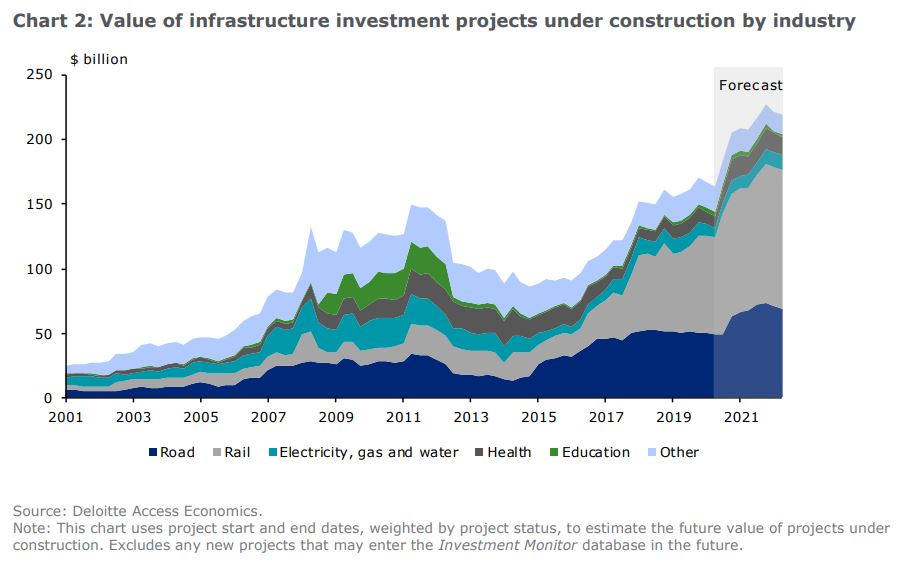

• This will see the total value of projects underway in the Investment Monitor database reach $225 billion in 2022. To put that in perspective it’s more than the amount spent during Australia’s liquified natural gas (LNG) boom. Almost three quarters of infrastructure investment will be in new transport projects, but there will also be significant increases in the amount spent on utilities, health and education.

Chart 2: Value of infrastructure investment projects under construction by industry

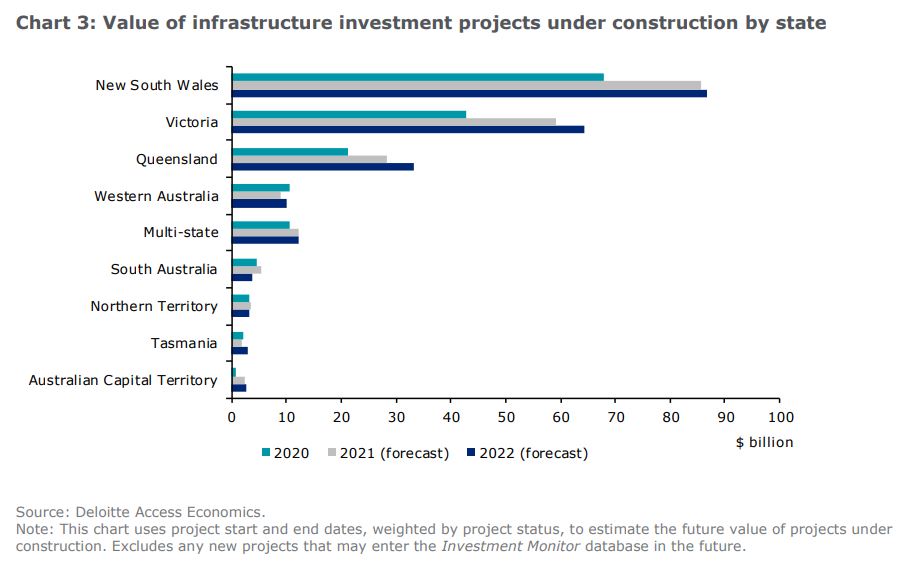

• Spending will also be concentrated in Australia’s east and south. New South Wales, Victoria and Queensland are expected to account for four fifths of total infrastructure projects under construction in 2022.

• A key point to note is that the costs of infrastructure have fallen, and the benefits are higher. On the cost front, governments can now borrow at record low interest rates to fund new investment. On the benefits front, higher infrastructure spending will help to soften the impact from winding back JobKeeper and JobSeeker. Australia’s population growth rate is also expected to recover to pre-COVID rates in coming years, albeit gradually so, thereby driving strong demand for infrastructure such as roads, rail lines, schools and hospitals. And there will be a slew of spill over benefits such as bolstering productivity and private sector activity. That means that the cut-off for projects considered ‘worthwhile doing’ has fallen notably.

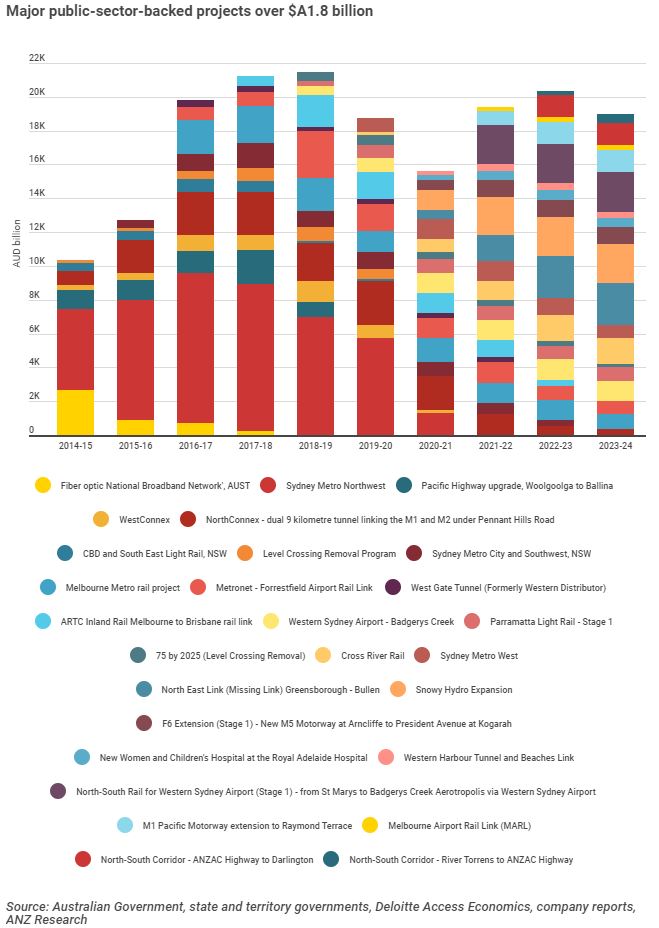

• Yet there are some concerns. The value of major contracts being awarded has fallen sharply through 2020. That has raised the question as to whether activity may stutter in the short term, at least until fast-tracked projects are underway. This places some pressure on the upcoming state budgets as well as efforts to award contracts in late 2020 and early 2021. There is also the risk that mistakes are made in the haste to get projects to market. But, on balance, the longer-term outlook remains very bright for infrastructure investment.

• Our state focus discusses the relative success of the Northern Territory in controlling the spread of COVID-19 and the resulting impact this has had on the territory’s economy. We also examine the ramp-up of production at the Ichthys LNG project and the outlook for further investment in the Northern Territory.

• Our special focus on the coal industry examines the sharp fall in the price of both coking and thermal coal in 2020, the impact of COVID-19 on global demand, the outlook for global supply, as well as long running structural challenges such as the transition towards less carbon intensive forms of electricity generation.

• Our special focus on the retail industry discusses the divergence in performance among Australian retailers in 2020, the rapid growth in e-commerce, the impact of fiscal support measures, as well as the outlook for the key driver of demand for retail investment – retail spending.

There’s far too much optimism embedded in that analysis. The Fed’s $14bn in new spending is tiny. We’re yet to see the big state surge. It will take time on both and while that happens old projects role off. Road and rail is not going to ramp in the way Deloitte hopes:

This will not add much to growth because the stock of projects is already so high. At least it will no longer add to unemployment from next year forward.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.