Total nonfarm payroll employment rose by 638,000 in October, and the unemployment rate declined to 6.9 percent, the U.S. Bureau of Labor Statistics reported today. These improvements in the labor market reflect the continued resumption of economic activity that had been curtailed due to the coronavirus (COVID-19) pandemic and efforts to contain it. In October, notable job gains occurred in leisure and hospitality, professional and business services, retail trade, and construction. Employment in government declined.

…In October, the unemployment rate declined by 1.0 percentage point to 6.9 percent, and the number of unemployed persons fell by 1.5 million to 11.1 million. Both measures have declined for 6 consecutive months but are nearly twice their February levels (3.5 percent and 5.8 million, respectively).

…The change in total nonfarm payroll employment for August was revised up by 4,000 from +1,489,000 to +1,493,000, and the change for September was revised up by 11,000 from +661,000 to +672,000. With these revisions, employment in August and September combined was 15,000 higher than previously reported.

But I still expect a double-dip as the virus runs riot:

Advertisement

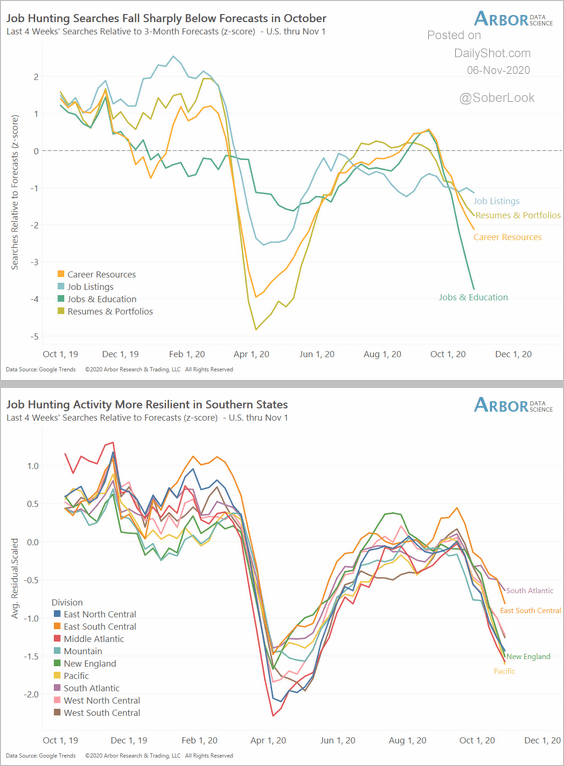

Shutting large parts of the economy:

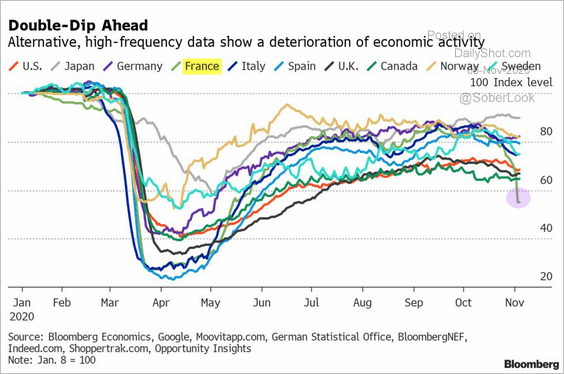

Same in Europe:

Advertisement

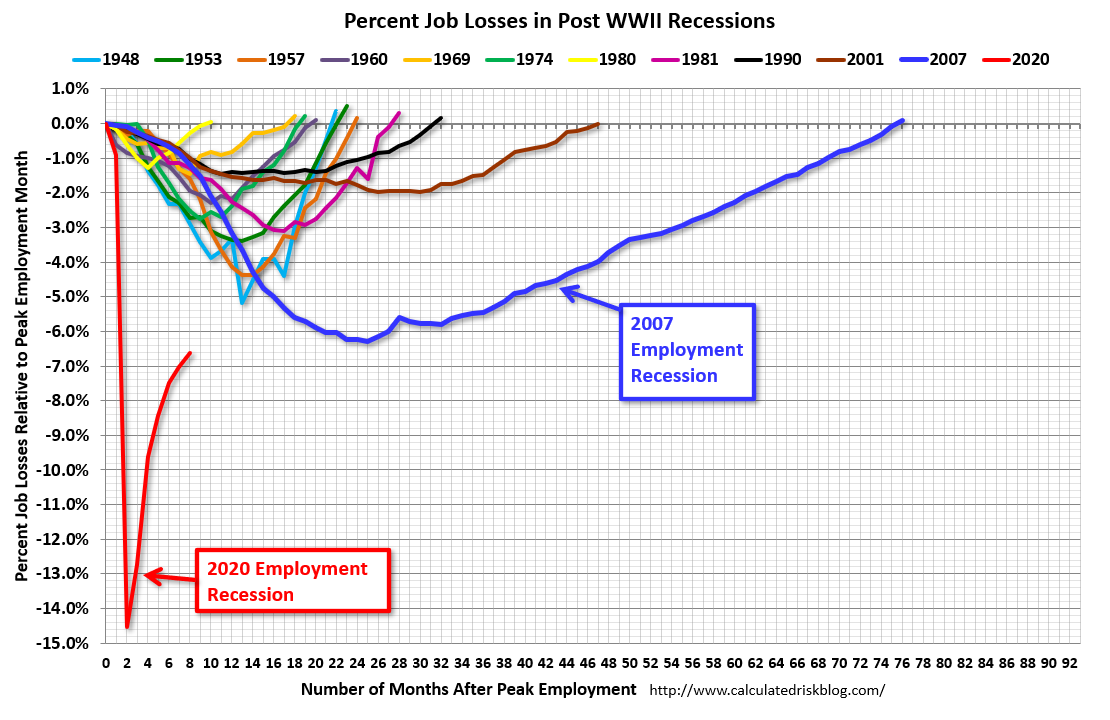

Though, as I’ve said previously, this iteration of lockdown will likely cost services much more than manufacturing as the global inventory cycle spins to restocking.

So, another deflation shock is underway and the US election made that worse by retaining a Republican senate already hosing off big stimulus. The implications of that are obvious as more of the work falls upon the Fed meaning for markets that:

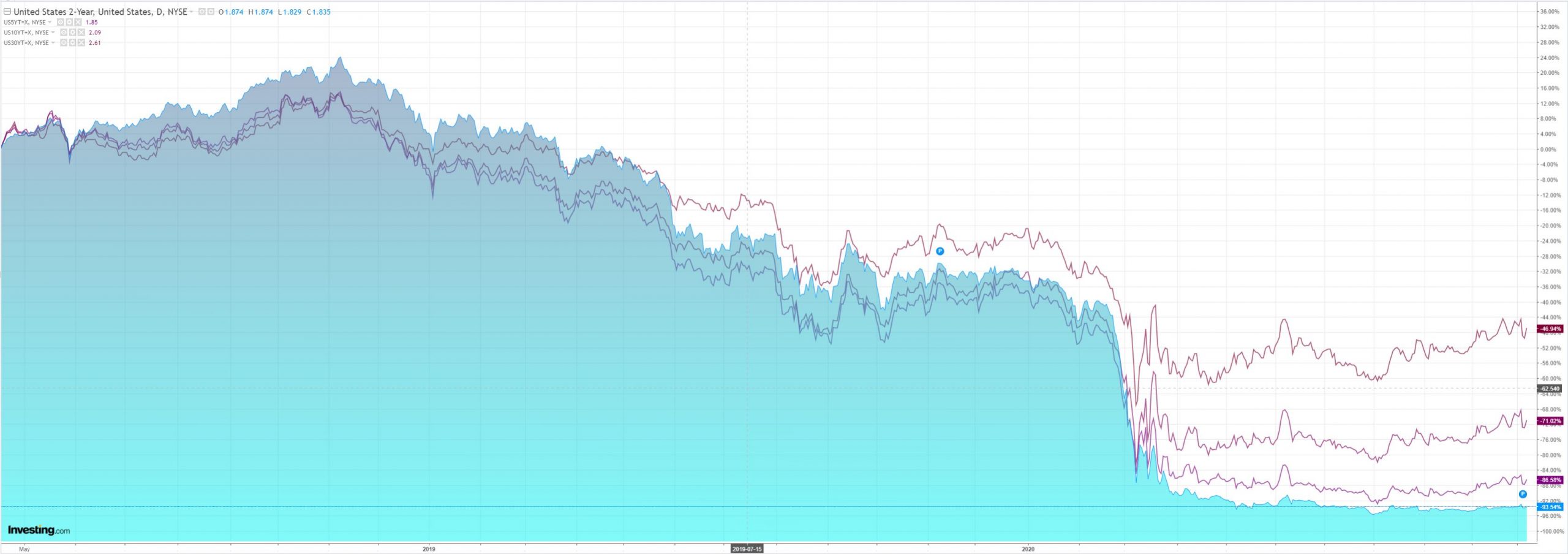

deflation trades are back in vogue (tech, growth, bonds);

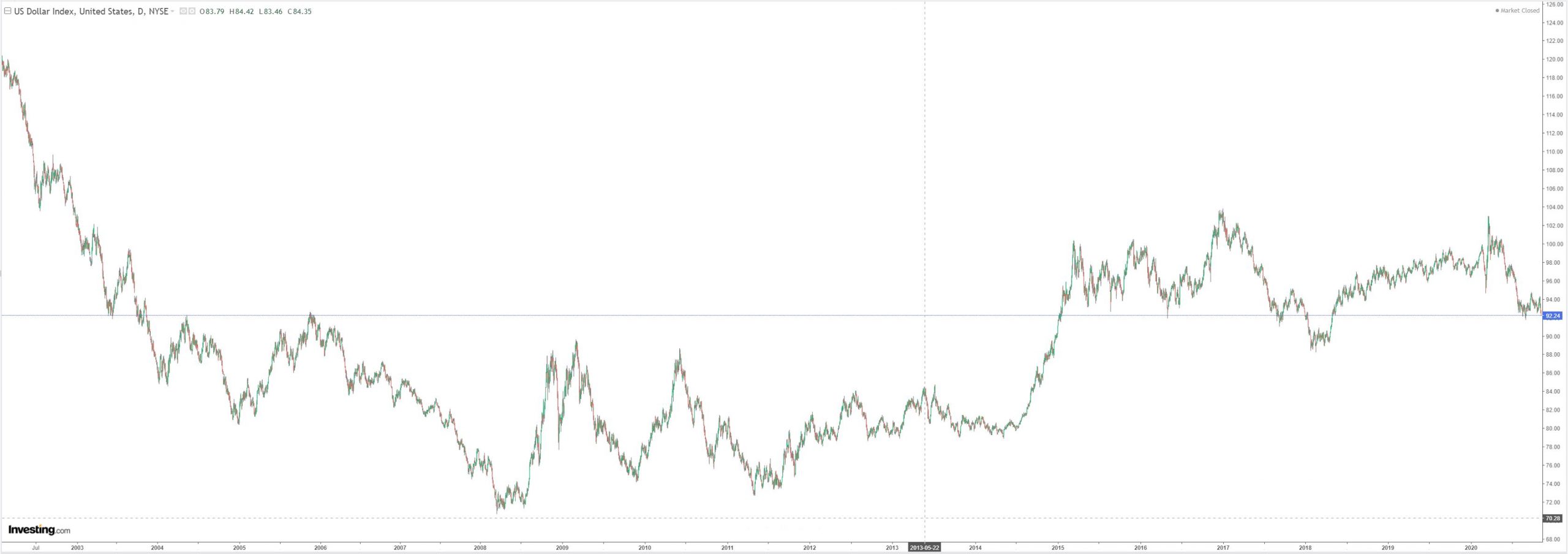

a weak DXY;

EM bid along with commodities on monetary tailwind for real assets;

gold and BTC.

Advertisement

Obviously, this is also Australian dollar positive for the time being, boosted as well by any thaw in relations between the Biden Administration and China and our virus success.

However, I do not expect that bid to get very far. There is a considerable risk of another market crash that would entirely reverse this trade in a run for the DXY safe haven if the virus is not brought under control.

Even if it is, the headwinds are also very strong:

Advertisement

it may require market risk-off to get the Fed moving again;

weak Australian recovery;

uber-dovish RBA joining the currency war;

a pivot in global growth later in 2021 as developed economies lift with vaccines and while China slows on easing stimulus;

Australia-China decoupling, and

tumbling iron ore prices through mid-2021 as the supply/demand equation normalises.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.