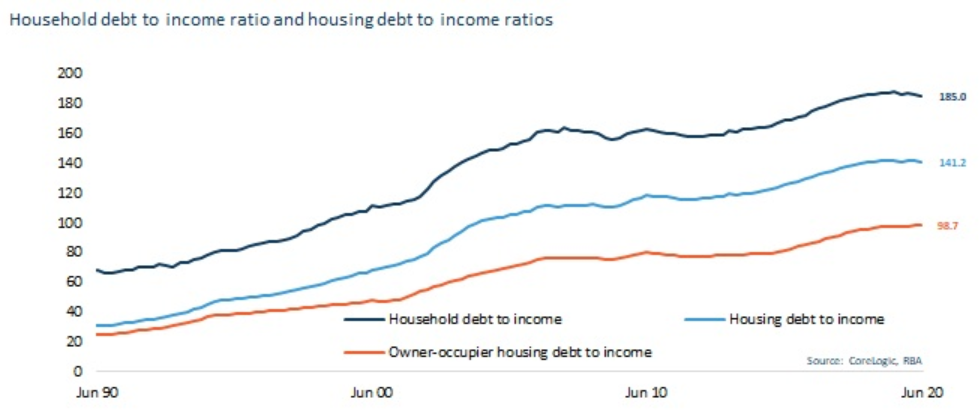

Australian household debt levels have increased substantially over the past thirty years, with the ratio of household debt to annual disposable income rising from 68% in June 1990 to a recent peak of 188.5% in June 2019. Since June last year, the ratio has reduced slightly to 185.0%.

Most of the debt held by households is housing debt, which comprises around 76% of overall household debt. Thirty years ago housing debt comprised a much smaller 46% of overall household debt. The skew towards housing debt can also be seen in the latest Household Income and Wealth survey from the Australian Bureau of Statistics, which showed the median value of debt held against owner occupied dwellings was $102,600, compared with a median debt level of $5,000 for student loans, $3,000 on credit cards and $3,700 on car loans.

The full text of this article is available to MacroBusiness subscribers

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.