By Gareth Aird, head of Australian economics at CBA:

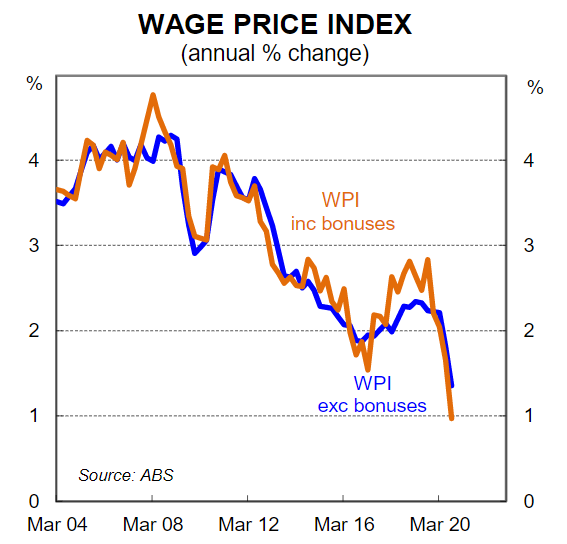

The Wage Price Index (WPI) rose by just 0.1% in Q3 20 and the annual rate stepped down to 1.4%.

Private sector wages grew by 0.1% while public sector wages rose by 0.2% over the quarter.

Wages growth will be weak over the next two years, but tax cuts will see the take home pay of most workers rise in 2020/21.

The 0.1% increase in the WPI over Q320 was less than the consensus looking for 0.2%,but it’s not a material miss. Put simply, wages growth has effectively ground to a halt because of the COVID-19 pandemic. Wages growth in the private sector has been just 0.1% over both the June and September quarters. It has been a bit stronger in the public sector (0.5% in Q2 and 0.2% in Q3). It should be noted that wage subsidies (i.e. JobKeeper) falls outside of the collection scope of the WPI.

The sharp slowdown in wages growth highlights just how flexible wages are in Australia. On the surface weaker wages growth looks like a negative development over the past two quarters. But with such a large economic shock and drop in production the sudden slowdown in wages growth is more likely to have resulted in less people losing their jobs than would otherwise be the case. History shows that if wages are too rigid there can be greater job losses in an economic downturn as businesses are faced with the prospect of continuing to pay workers higher wages as sales drop. Lower wages growth only becomes problematic if it becomes entrenched. That is the clear risk if the economic recovery takes too long.

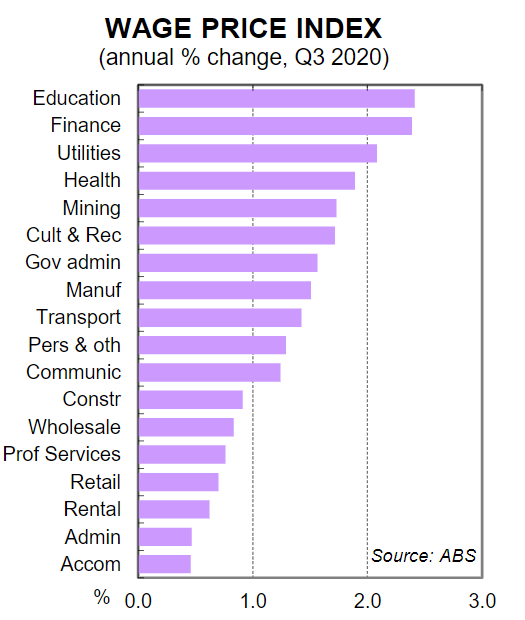

The wages data by industry is only published in original terms so it won’t be until Q2 21 that we will can make a proper comparison of wage changes across industries due to the pandemic. Notwithstanding it looks like the sharpest slowdown in wages growth has occurred in the industries of accommodation, administration, rental and retail (see chart below).

Wages growth will be weak over the next few years because spare capacity in the labour market will make it hard for workers to negotiate a pay rise. But wages growth is not the same thing as growth in the take home pay packets of workers. Changes in tax rates influence what an employee keeps out of their salary. The Stage 2 tax cuts, which were pulled forward in the October 2020 Budget, will see the take home pay of a fulltime worker on the average salary of $A89k keep an extra $A1080 a year. That is a 1.6% increase in take home pay in 2020/21 based on no change in wage.

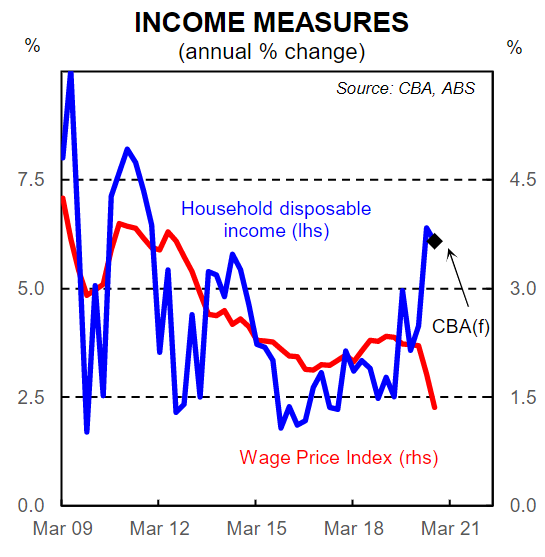

It is after tax income that matters most for households and the economy more broadly. Indeed it is changes in household disposable income that influence the capacity of the household sector to spend. As we have regularly noted household disposable income has stepped up significantly over the COVID-19 period because of the huge fiscal stimulus injected into the household sector. The disparity between less spending due to restrictions and health-related concerns and more income due to Government stimulus has seen a massive war chest of savings accrued. On our calculations it looks like when we start2021 the Australian household sector is likely to have around $A100bn (5% of GDP) in additional savings that have been built up since COVID-19 arrived in Australia(this excludes the early withdrawal of superannuation). The expected drawdown of those savings will provide a significant tailwind to consumption next year despite weak wages growth.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.