From Gareth Aird, head of Australian economics at CBA:

Key Points:

The list of encouraging signals in the Australian economic data is growing and there are genuine reasons to believe the domestic economic recovery is going to be strong over the next two years.

An unprecedented level of fiscal and monetary policy stimulus coupled with an expected drawdown in accumulated savings and the further easing of COVID‑related restrictions will support economic growth and job creation.

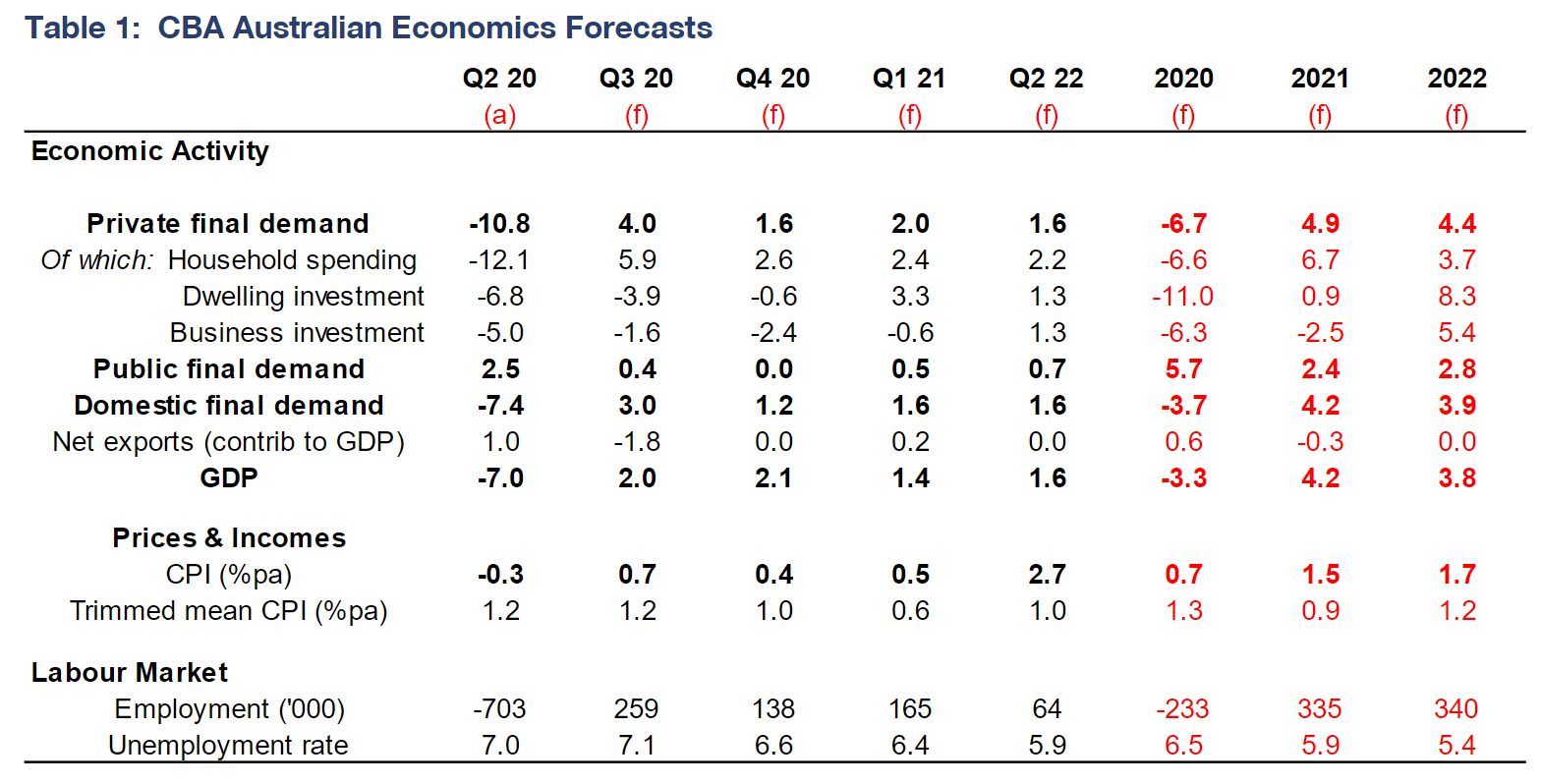

We now expect a fall in GDP of 3.3% in 2020 to be followed by an increase in GDP of 4.2% in 2021 and 3.8% in 2022.

We expect the unemployment rate to be 5.75% at end‑2021 and 5.0% at end‑2022.

Overview

When GDP and employment collapsed in Australia over Q2 20 comparisons were made with the Great Depression. We had not seen such a sharp deterioration in economic data since the 1930s. But the similarities between the Great Depression and the COVID-19 pandemic from an economic perspective only pertain to the Q2 20 activity data. There is not much about the Australian economy in 2020 that is analogous to the Great Depression, particularly the huge monetary and fiscal support injected into the economy.

We remarked earlier in the year that we were in the midst of a manufactured contraction in the economy that was a direct result of policy decisions to limit the spread of COVID-19. GDP is simply a measure of production over a period of time and nobody should have been particularly surprised that output drops sharply when large parts of the economy are shut down. By the same token, it was a natural response for spending and employment to lift as parts of the economy were re-opened. Indeed the Government’s fiscal support packages were designed to keep as much of the economic furniture intact so that when restrictions were eased activity could rebound swiftly.

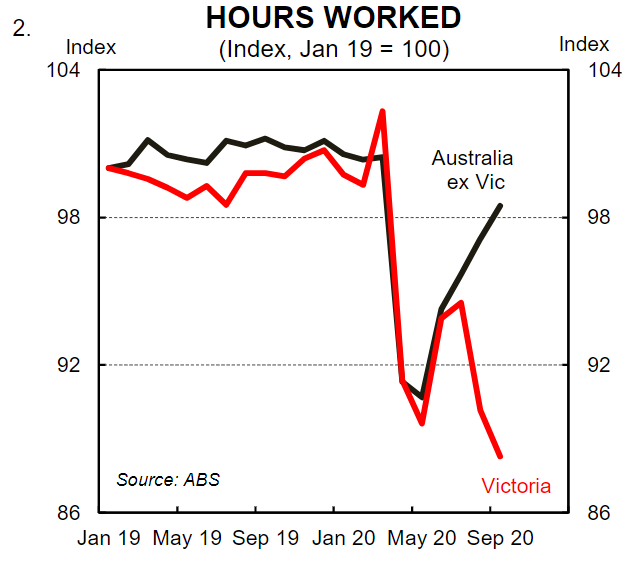

It is clear that the economic data at the national level has improved since the middle of the year (charts 1 & 2).Indeed we expect a decent bounce in GDP over H2 20 to show up in the Q3 20 and Q4 20 national accounts (our forecasts are tabled on page 5). But at this juncture the focus shifts to what the strength and duration of the economic recovery will look like in 2021and beyond. On that score we are optimistic. There is plenty of evidence creeping into the data that signals strong outcomes next year are more likely than not. As a result we have upwardly revised our profile for GDP in 2021 and by extension we have lowered our profile for the unemployment rate. We have also extended our forecast profile to end-2022. This note discusses five factors that lie behind our optimistic and above-consensus view on the Australia economic outlook.

(i) COVID-19 –the threat has diminished in Australia

A discussion on the economic outlook should start with a look at COVID-19 itself. Restrictions put in place to stop the spread of COVID-19 explain the bulk of the swings in economic data over 2020. Indeed the big disparity between economic outcomes by state, particularly in Victoria relative to the rest of the country, can be attributed to COVID-19 and the restrictions that have been imposed and lifted throughout the year.

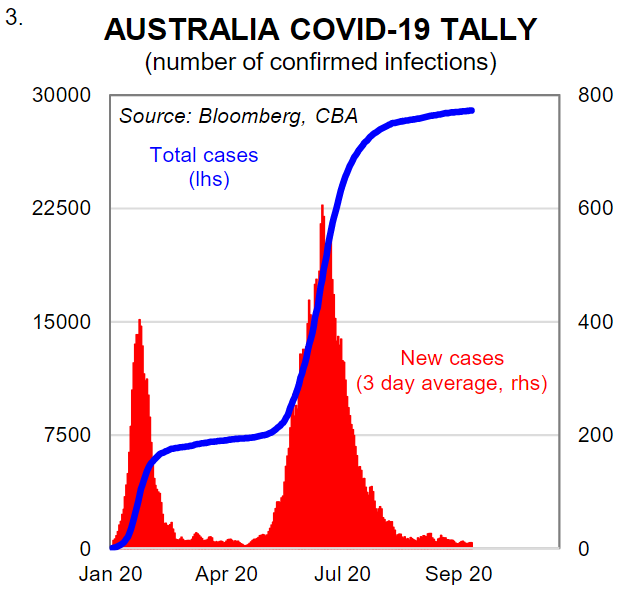

At the time of publication Australia has gone five days in a row without a single community transmission of COVID-19. All new infections over the past five days have been identified in overseas arrivals in hotel quarantine. Australian policymakers did not explicitly pursue a COVID-19 elimination strategy, but by design or default we have effectively achieved that. If nobody is contracting COVID-19 in the community then it is only a matter of time before restrictions on domestic activity are more fully removed. This will automatically provide a lift to spending and employment. In addition, households will not limit activity due to concerns about catching the virus if nobody in the community has COVID-19. Again this provides a boost to spending, particularly services-related consumption. This has been the case, for example, in WA where there has been an almost complete economic recovery and essentially full removal of restrictions within the state.

Here we should stress that our upgraded central scenario does not assume that a COVID-19 vaccine is readily available and widely distributed in 2021. Rather we take a conservative approach and assume that a vaccine in Australia does not arrive until Q1 2022. A vaccine is simply an upside risk to the central case we present here. Clearly the probability of a vaccine arriving in 2021 has improved after news emerged this week that large global pharmaceutical companies may have developed a highly effective vaccine. However, its safety is yet to be proven, which means it is not clear when/if it will become readily available. In any event we think that Australia has made sufficient inroads with COVID-19 elimination that the domestic economy can recover strongly in 2021without a vaccine, provided any outbreaks are traced and well contained and significant restrictions are not reimposed.

(ii) Consumer confidence is at a 7-year high

The household perception of the economy is a key driver around consumer decisions to spend or save. Confident consumers are more likely to spend income, while cautious consumers are more likely to save it. That relationship has been impacted over the last six months because households haven’t been able to spend on a range of goods and services due to COVID-19, regardless of how they feel (more on that below). But in general confidence and spending decisions are aligned.

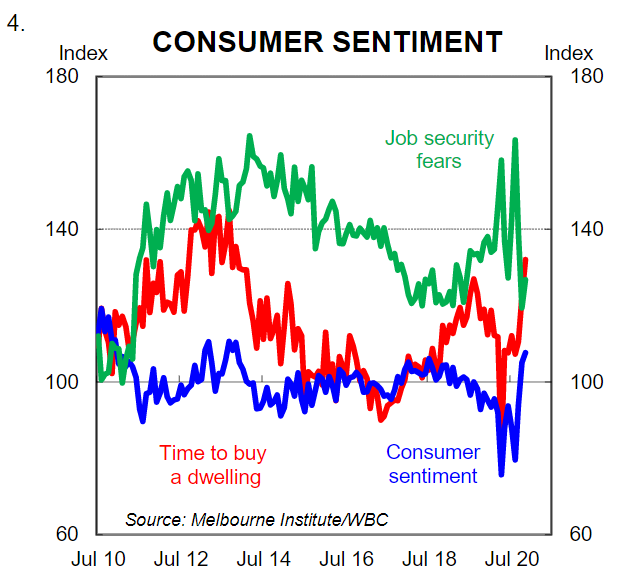

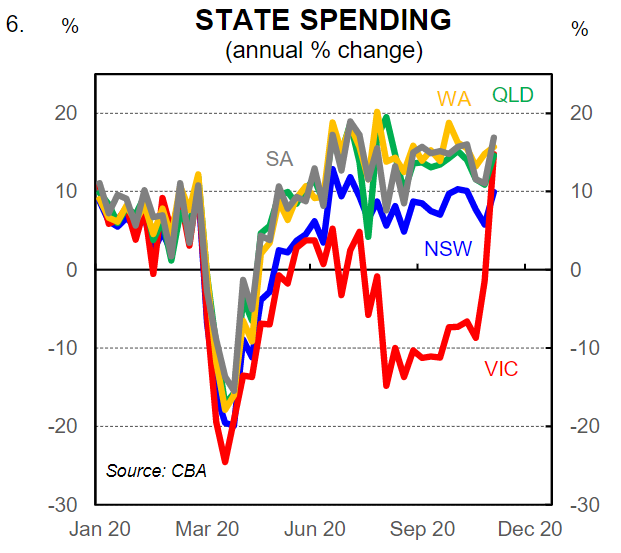

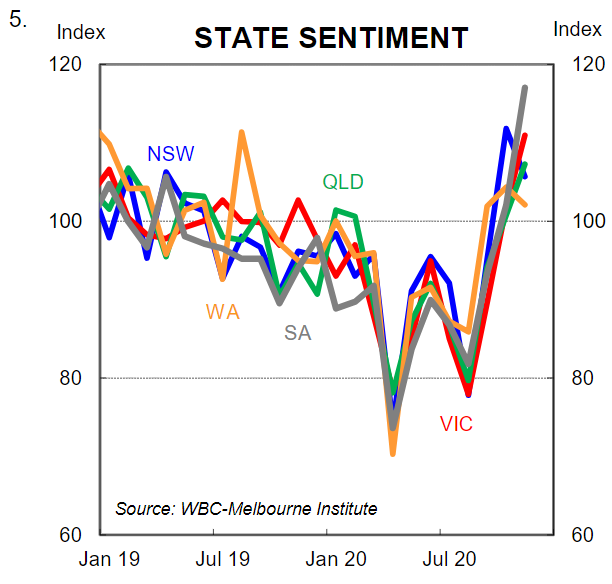

According to the WBC/Melbourne Institute monthly consumer sentiment report there has been a strong rebound in consumer confidence over the past four months (charts 5 & 6). Confidence is up by 35% since August and the level of confidence in November was 107.7 –a seven year high. In many respects these results are extraordinary given what has occurred over the past six months. Taken at face value this bodes very well for the economic outlook. The data indicates that the level of confidence in the economic outlook will be a support for household expenditure rather than a hindrance. Rising confidence begets more entrenched levels of higher confidence as a positive feedback loop develops between expectations and reality. We think that we are at that stage now and our most recent spending data by state supports our claims (chart 6).

It is worth noting that business confidence has also rebounded sharply, albeit not to the same highs as consumer confidence. Business confidence as measured in the NAB monthly business survey rose to its highest level since mid-2019in October. Rising business confidence is a natural response to higher consumer confidence as expectations around future demand are raised.

(iii) The ‘fiscal cliff’ will be successfully navigated via a drawdown in savings

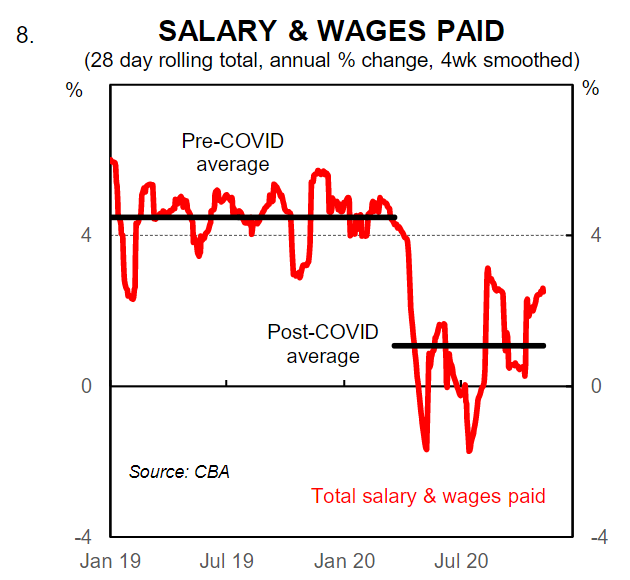

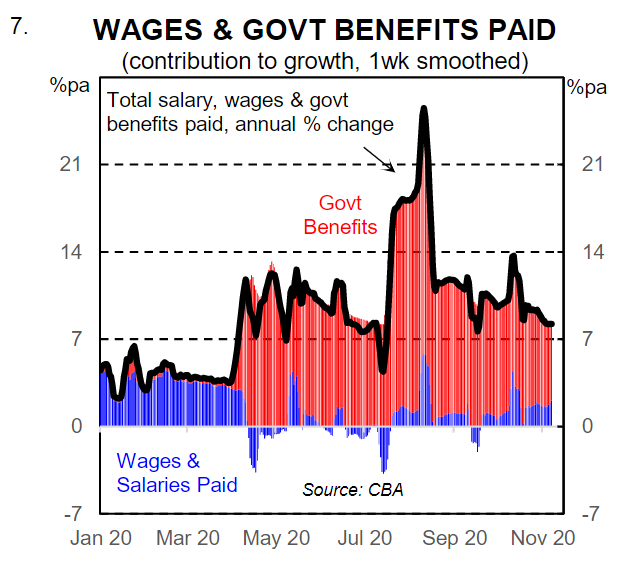

Updated analysis from payments into CBA bank accounts indicates that household income growth has held broadly steady since the JobKeeper and JobSeeker payments were tapered at the end of September (chart7). Growth in Government payments has stepped down, but that has been offset by a lift in wages and salaries due to the improvement in the labour market (chart 8). The upshot is that the annual growth rate in our partial read on household income that comprises wages and salaries paid plus government benefits paid remains well above its pre-COVID-19 level (latest data to 6 November). Indeed it is likely to step up over the coming months. Hours worked will lift because of the reopening of Victoria. And income tax cuts, which effectively kick in now, will boost the take home pay of workers.

The positive shock to household income at a time when spending has been negatively impacted because of restrictions has resulted in an unpresented spike in savings. We estimate that an additional $A45bn or 2.3% of GDP was saved over Q2 20 (over and above what is normally saved given the household sector is a net saver). We expect to see a similar outcome when the Q3 20 national accounts print in on 2 December. Both spending and income have risen over Q3 20 and on our estimates an additional $A39bn or 2.0% of GDP was saved over Q3 20 compared to a ‘normal’ level of saving. This means that the household sector will have built up a massive war chest of savings over six months that is worth around 4.3% of GDP. These savings exclude the early withdrawal of superannuation and are calculated as the difference between income and expenditure less ‘normal savings’.

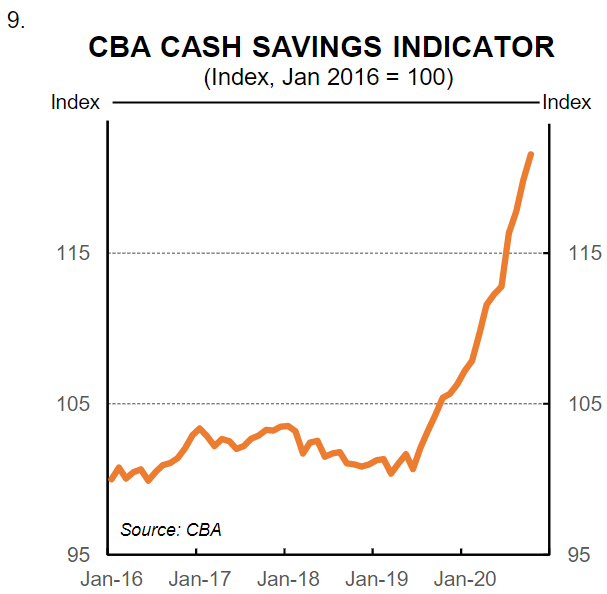

Our CBA cash savings indicator, which is based on the average total savings balance per household, including home lending related savings and transaction or savings accounts, paints a similar picture. It has surged over the past six months to sit 15.3% higher on year ago levels as at October (chart 9). Indeed our data indicates that household coffers have continued to swell over the early part of Q4 20.

The sums are simply extraordinary. On our calculations it looks like when we start 2021 the Australian household sector is likely to have around $A100bn (5% of GDP) in additional savings that have been accrued since COVID-19 arrived in Australia-again this excludes the early withdrawal of superannuation.

The upshot is that we will see a savings drawdown in 2021. This will provide a significant tailwind to consumption as pent up demand is unleashed. We readily acknowledge that there is uncertainty around what proportion of savings will be used to fund expenditure and how fast accumulated savings will be spent. But the elevated level of consumer confidence means a material drawdown is likely, particularly when factoring in why the savings were accrued.

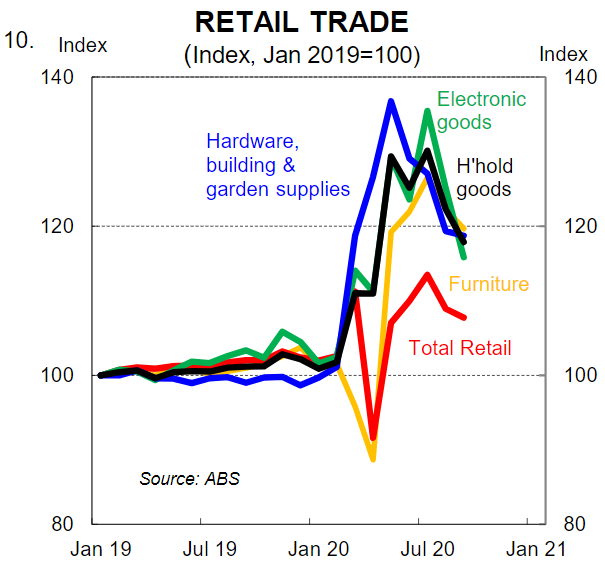

Savings surged because the government injected money into the household sector at a time when it was not possible to purchase many goods and services due to the pandemic. But we saw big increases in spending on a whole range of household goods that were still available for purchase (chart 10). This is clear evidence that the willingness to spend has been there, just not the way.

In our estimation the savings drawdown will put enough upward pressure on demand to enable JobKeeper to expire without a negative shock to the labour market materialising. JobKeeper is simply a wage subsidy that was designed to keep employees attached to their employers while restrictions artificially limited demand and negatively impacted sales. But once restrictions are more fully eased and demand bounces, the removal of a wage subsidy does not mean a business will retrench its staff. It simply means that wages will be paid from sales as has always been the case.

(iv) The housing market is no longer a source of risk

In our view there have been two key sources of downside risk from the pandemic related to the housing market: (i) home prices falling sharply; and(ii) residential construction dropping significantly primarily because of lower net overseas migration (NOM). Those risks have diminished materially.

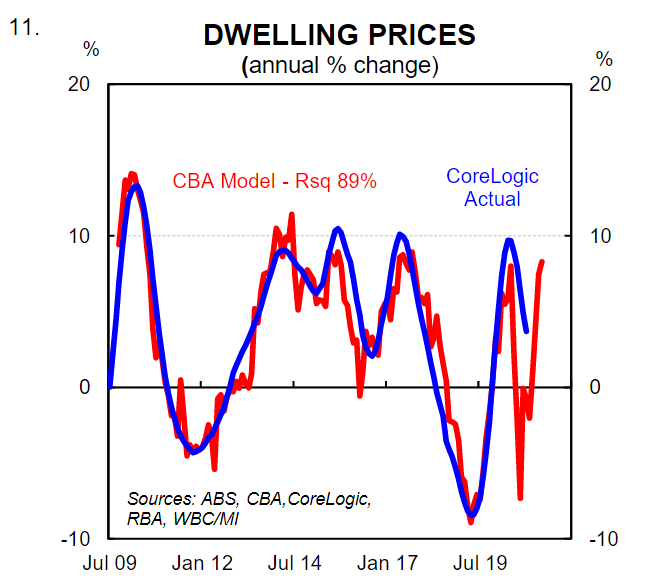

On home prices it is clear that price falls will only end up being modest nationally. Indeed prices are rising now in most capital cities. We updated our dwelling price forecasts in early September to look for a 6% peak to trough forecast and a strong rebound in prices in H2 21. We believe the risks to our forecasts are skewed to upside. The RBA has lowered interest rates since we updated our home price forecasts and mortgage rates have declined as a result. In addition near term momentum indicators of the housing market have continued to strengthen and our home price model is signalling that solid price rises could be imminent (chart 11). As such, we expect a positive wealth effect to be in play over 2021 whereby rising home prices are a tailwind on household consumption, particularly on bigger ticket items like motor vehicles.

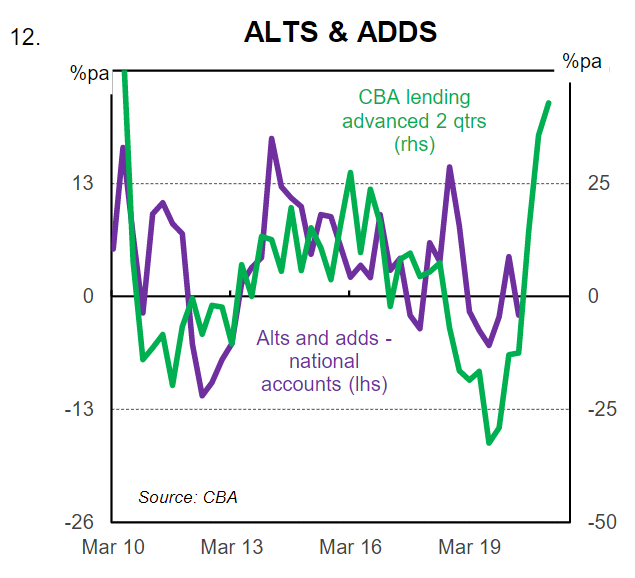

On housing construction the forward looking indicators are encouraging. In August we published a thematic note where we noted that some unusual dynamics were impacting the outlook for housing construction. More specifically, we noted that new construction was likely to fall significantly due to lower net overseas migration, but that record low interest rates would support alterations and additions. Our views around renovation activity have come to fruition. Our lending data indicates there will be a big step up in alterations and additions which are worth 40% of total residential construction (chart 12).

Where we have been genuinely surprised is around the building approvals data for new homes. The message here is that new construction will not drop too significantly. That poses a new risk around oversupply. But that risk is somewhat tempered by the prospect of a vaccine which will see net overseas migration return, albeit we think at a lower level than pre-COVID. We no longer expect dwelling investment to be a drag on the economy in 2021 and forecast growth in renovation activity to offset lower new construction (which will not decline as much as we previously expected).

(v) Domestic tourism is set to boom

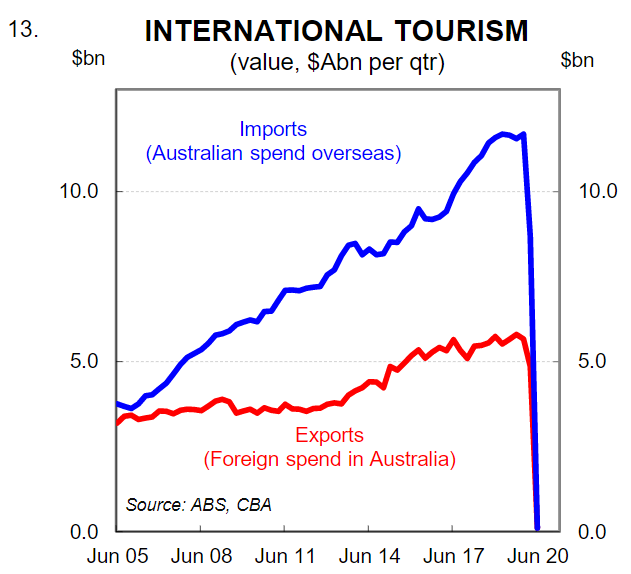

Regular readers may recall that back in July we published a piece looking at the impact of international borders closures on the Australian economy. We highlighted that while international border closures would hurt Australian businesses that rely on foreign tourists, the overall macro-economic impact would be far less damaging. We reached that conclusion because Australians spend on average twice as much holidaying abroad compared with what is spent by overseas residents having a holiday in Australia (in 2019 Aussies spent $A47bn overseas vs $A23bn spent by overseas holidaymakers in Australia–chart 13).

We remarked in the note, “the message therefore from policymakers becomes an easy one –if you were going to have an overseas holiday this year then please take one domestically and support Australian businesses! We suspect that regional Australia could do well from an expected lift in domestic tourism”.

Now in many ways that story has not been able to unfold because there have been borders put up between states which serves as a big restriction on domestic tourism. Some parts of regional Australia have been doing well from domestic tourism, but things would be a lot stronger if interstate borders were fully open. Given the current status of COVID-19 in Australia we think that it cannot be too long before interstate borders are fully reopened. That will generate a massive lift in domestic tourism given the overseas borders remain closed and households are flush with cash. We expect next year to be a very positive story for regional Australia as domestic tourism booms.

Updated forecasts

We have upwardly revised our profile for GDP. Our expectation for GDP to contract by 3.3% in 2020 is unchanged (we upwardly revised our assessment of H2 20 GDP in mid-September). But we now expect a much stronger recovery in 2021 and we have extended our forecast profile to end-2022.

We now forecast GDP growth of 4.2% in 2021 (versus 2.5% previously). And we expect economic growth of 3.8% in2022. Our updated GDP profile sees us lower our profile for the unemployment rate. We now expect the unemployment rate to be 5.75% at end-2021 (vs 6.5% previously). And we forecast the unemployment rate to be 5.0% at end-2022. By comparison the RBA expects the unemployment rate to be 6.0% at end-2022.

We assume a significant reduction in the savings rate because growth in consumption will outpace growth in income over the next two years. Indeed the savings rate will drop quite quickly initially. There is simply no reason for the savings rate to remain elevated, particularly when households as a collective are optimistic around the economic outlook.

Our central scenario is for inflation to remain low over our forecast horizon because the economy will have an output gap until end-2022. However we continue to point out to readers that there is upside risk to modelled inflation because there is a large disparity at present between wages growth and household income growth. The longer this disparity persists the greater the risk that inflation outcomes are higher than modelled inflation would imply. We think that there is a non-trivial risk that inflation rises at a faster pace than our forecasts indicate. In our view the risks around our inflation forecasts are clearly skewed to the upside. Table 1 below contains our updated quarterly profile for GDP, employment, unemployment and inflation.

Monetary policy implications

Our updated forecasts for the economy do not have any implications for our views on the RBA cash rate target over our forecast horizon (end-2022). We expect the cash rate to be left on hold at 0.10%. Indeed in the Governor’s Statement accompanying the November Board meeting where a suit of easing measures were introduced it was noted that, “the Board is not expecting to increase the cash rate for at least three years”.

However, we think that the economy will be on a sufficiently entrenched path of improvement by the middle of next year that the RBA will need to either remove or increase the target yield on the 3 year Australia Commonwealth Government Bond (ACGB). For as long as the target on the3 year ACGB sits at the same level as the cash rate the RBA is implying that the cash rate will remain on hold for the next three years. The middle of next year is still some time away, but it is worth considering now how these dynamics are likely to play out given our updated views on the outlook for the Australian economy.

In summary we believe the metaphorical ‘bridge’ has been built very well and sets Australia up for a prosperous next two years. We think that provided transmission of COVID-19 in Australia remains low, particularly community transmission, the strength of the economic recovery in 2021 will surprise many.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.

It is worth noting that business confidence has also rebounded sharply, albeit not to the same highs as consumer confidence. Business confidence as measured in the NAB monthly business survey rose to its highest level since mid-2019in October. Rising business confidence is a natural response to higher consumer confidence as expectations around future demand are raised.(iii) The ‘fiscal cliff’ will be successfully navigated via a drawdown in savingsUpdated analysis from payments into CBA bank accounts indicates that household income growth has held broadly steady since the JobKeeper and JobSeeker payments were tapered at the end of September (chart7). Growth in Government payments has stepped down, but that has been offset by a lift in wages and salaries due to the improvement in the labour market (chart 8). The upshot is that the annual growth rate in our partial read on household income that comprises wages and salaries paid plus government benefits paid remains well above its pre-COVID-19 level (latest data to 6 November). Indeed it is likely to step up over the coming months. Hours worked will lift because of the reopening of Victoria. And income tax cuts, which effectively kick in now, will boost the take home pay of workers.

It is worth noting that business confidence has also rebounded sharply, albeit not to the same highs as consumer confidence. Business confidence as measured in the NAB monthly business survey rose to its highest level since mid-2019in October. Rising business confidence is a natural response to higher consumer confidence as expectations around future demand are raised.(iii) The ‘fiscal cliff’ will be successfully navigated via a drawdown in savingsUpdated analysis from payments into CBA bank accounts indicates that household income growth has held broadly steady since the JobKeeper and JobSeeker payments were tapered at the end of September (chart7). Growth in Government payments has stepped down, but that has been offset by a lift in wages and salaries due to the improvement in the labour market (chart 8). The upshot is that the annual growth rate in our partial read on household income that comprises wages and salaries paid plus government benefits paid remains well above its pre-COVID-19 level (latest data to 6 November). Indeed it is likely to step up over the coming months. Hours worked will lift because of the reopening of Victoria. And income tax cuts, which effectively kick in now, will boost the take home pay of workers. The positive shock to household income at a time when spending has been negatively impacted because of restrictions has resulted in an unpresented spike in savings. We estimate that an additional $A45bn or 2.3% of GDP was saved over Q2 20 (over and above what is normally saved given the household sector is a net saver). We expect to see a similar outcome when the Q3 20 national accounts print in on 2 December. Both spending and income have risen over Q3 20 and on our estimates an additional $A39bn or 2.0% of GDP was saved over Q3 20 compared to a ‘normal’ level of saving. This means that the household sector will have built up a massive war chest of savings over six months that is worth around 4.3% of GDP. These savings exclude the early withdrawal of superannuation and are calculated as the difference between income and expenditure less ‘normal savings’.Our CBA cash savings indicator, which is based on the average total savings balance per household, including home lending related savings and transaction or savings accounts, paints a similar picture. It has surged over the past six months to sit 15.3% higher on year ago levels as at October (chart 9). Indeed our data indicates that household coffers have continued to swell over the early part of Q4 20.The sums are simply extraordinary. On our calculations it looks like when we start 2021 the Australian household sector is likely to have around $A100bn (5% of GDP) in additional savings that have been accrued since COVID-19 arrived in Australia-again this excludes the early withdrawal of superannuation.The upshot is that we will see a savings drawdown in 2021. This will provide a significant tailwind to consumption as pent up demand is unleashed. We readily acknowledge that there is uncertainty around what proportion of savings will be used to fund expenditure and how fast accumulated savings will be spent. But the elevated level of consumer confidence means a material drawdown is likely, particularly when factoring in why the savings were accrued.Savings surged because the government injected money into the household sector at a time when it was not possible to purchase many goods and services due to the pandemic. But we saw big increases in spending on a whole range of household goods that were still available for purchase (chart 10). This is clear evidence that the willingness to spend has been there, just not the way.In our estimation the savings drawdown will put enough upward pressure on demand to enable JobKeeper to expire without a negative shock to the labour market materialising. JobKeeper is simply a wage subsidy that was designed to keep employees attached to their employers while restrictions artificially limited demand and negatively impacted sales. But once restrictions are more fully eased and demand bounces, the removal of a wage subsidy does not mean a business will retrench its staff. It simply means that wages will be paid from sales as has always been the case.(iv) The housing market is no longer a source of riskIn our view there have been two key sources of downside risk from the pandemic related to the housing market: (i) home prices falling sharply; and(ii) residential construction dropping significantly primarily because of lower net overseas migration (NOM). Those risks have diminished materially.On home prices it is clear that price falls will only end up being modest nationally. Indeed prices are rising now in most capital cities. We updated our dwelling price forecasts in early September to look for a 6% peak to trough forecast and a strong rebound in prices in H2 21. We believe the risks to our forecasts are skewed to upside. The RBA has lowered interest rates since we updated our home price forecasts and mortgage rates have declined as a result. In addition near term momentum indicators of the housing market have continued to strengthen and our home price model is signalling that solid price rises could be imminent (chart 11). As such, we expect a positive wealth effect to be in play over 2021 whereby rising home prices are a tailwind on household consumption, particularly on bigger ticket items like motor vehicles.On housing construction the forward looking indicators are encouraging. In August we published a thematic note where we noted that some unusual dynamics were impacting the outlook for housing construction. More specifically, we noted that new construction was likely to fall significantly due to lower net overseas migration, but that record low interest rates would support alterations and additions. Our views around renovation activity have come to fruition. Our lending data indicates there will be a big step up in alterations and additions which are worth 40% of total residential construction (chart 12).Where we have been genuinely surprised is around the building approvals data for new homes. The message here is that new construction will not drop too significantly. That poses a new risk around oversupply. But that risk is somewhat tempered by the prospect of a vaccine which will see net overseas migration return, albeit we think at a lower level than pre-COVID. We no longer expect dwelling investment to be a drag on the economy in 2021 and forecast growth in renovation activity to offset lower new construction (which will not decline as much as we previously expected).(v) Domestic tourism is set to boomRegular readers may recall that back in July we published a piece looking at the impact of international borders closures on the Australian economy. We highlighted that while international border closures would hurt Australian businesses that rely on foreign tourists, the overall macro-economic impact would be far less damaging. We reached that conclusion because Australians spend on average twice as much holidaying abroad compared with what is spent by overseas residents having a holiday in Australia (in 2019 Aussies spent $A47bn overseas vs $A23bn spent by overseas holidaymakers in Australia–chart 13).We remarked in the note, “the message therefore from policymakers becomes an easy one –if you were going to have an overseas holiday this year then please take one domestically and support Australian businesses! We suspect that regional Australia could do well from an expected lift in domestic tourism”.Now in many ways that story has not been able to unfold because there have been borders put up between states which serves as a big restriction on domestic tourism. Some parts of regional Australia have been doing well from domestic tourism, but things would be a lot stronger if interstate borders were fully open. Given the current status of COVID-19 in Australia we think that it cannot be too long before interstate borders are fully reopened. That will generate a massive lift in domestic tourism given the overseas borders remain closed and households are flush with cash. We expect next year to be a very positive story for regional Australia as domestic tourism booms.Updated forecastsWe have upwardly revised our profile for GDP. Our expectation for GDP to contract by 3.3% in 2020 is unchanged (we upwardly revised our assessment of H2 20 GDP in mid-September). But we now expect a much stronger recovery in 2021 and we have extended our forecast profile to end-2022.We now forecast GDP growth of 4.2% in 2021 (versus 2.5% previously). And we expect economic growth of 3.8% in2022. Our updated GDP profile sees us lower our profile for the unemployment rate. We now expect the unemployment rate to be 5.75% at end-2021 (vs 6.5% previously). And we forecast the unemployment rate to be 5.0% at end-2022. By comparison the RBA expects the unemployment rate to be 6.0% at end-2022.We assume a significant reduction in the savings rate because growth in consumption will outpace growth in income over the next two years. Indeed the savings rate will drop quite quickly initially. There is simply no reason for the savings rate to remain elevated, particularly when households as a collective are optimistic around the economic outlook.Our central scenario is for inflation to remain low over our forecast horizon because the economy will have an output gap until end-2022. However we continue to point out to readers that there is upside risk to modelled inflation because there is a large disparity at present between wages growth and household income growth. The longer this disparity persists the greater the risk that inflation outcomes are higher than modelled inflation would imply. We think that there is a non-trivial risk that inflation rises at a faster pace than our forecasts indicate. In our view the risks around our inflation forecasts are clearly skewed to the upside. Table 1 below contains our updated quarterly profile for GDP, employment, unemployment and inflation.Monetary policy implicationsOur updated forecasts for the economy do not have any implications for our views on the RBA cash rate target over our forecast horizon (end-2022). We expect the cash rate to be left on hold at 0.10%. Indeed in the Governor’s Statement accompanying the November Board meeting where a suit of easing measures were introduced it was noted that, “the Board is not expecting to increase the cash rate for at least three years”.However, we think that the economy will be on a sufficiently entrenched path of improvement by the middle of next year that the RBA will need to either remove or increase the target yield on the 3 year Australia Commonwealth Government Bond (ACGB). For as long as the target on the3 year ACGB sits at the same level as the cash rate the RBA is implying that the cash rate will remain on hold for the next three years. The middle of next year is still some time away, but it is worth considering now how these dynamics are likely to play out given our updated views on the outlook for the Australian economy.In summary we believe the metaphorical ‘bridge’ has been built very well and sets Australia up for a prosperous next two years. We think that provided transmission of COVID-19 in Australia remains low, particularly community transmission, the strength of the economic recovery in 2021 will surprise many.

The positive shock to household income at a time when spending has been negatively impacted because of restrictions has resulted in an unpresented spike in savings. We estimate that an additional $A45bn or 2.3% of GDP was saved over Q2 20 (over and above what is normally saved given the household sector is a net saver). We expect to see a similar outcome when the Q3 20 national accounts print in on 2 December. Both spending and income have risen over Q3 20 and on our estimates an additional $A39bn or 2.0% of GDP was saved over Q3 20 compared to a ‘normal’ level of saving. This means that the household sector will have built up a massive war chest of savings over six months that is worth around 4.3% of GDP. These savings exclude the early withdrawal of superannuation and are calculated as the difference between income and expenditure less ‘normal savings’.Our CBA cash savings indicator, which is based on the average total savings balance per household, including home lending related savings and transaction or savings accounts, paints a similar picture. It has surged over the past six months to sit 15.3% higher on year ago levels as at October (chart 9). Indeed our data indicates that household coffers have continued to swell over the early part of Q4 20.The sums are simply extraordinary. On our calculations it looks like when we start 2021 the Australian household sector is likely to have around $A100bn (5% of GDP) in additional savings that have been accrued since COVID-19 arrived in Australia-again this excludes the early withdrawal of superannuation.The upshot is that we will see a savings drawdown in 2021. This will provide a significant tailwind to consumption as pent up demand is unleashed. We readily acknowledge that there is uncertainty around what proportion of savings will be used to fund expenditure and how fast accumulated savings will be spent. But the elevated level of consumer confidence means a material drawdown is likely, particularly when factoring in why the savings were accrued.Savings surged because the government injected money into the household sector at a time when it was not possible to purchase many goods and services due to the pandemic. But we saw big increases in spending on a whole range of household goods that were still available for purchase (chart 10). This is clear evidence that the willingness to spend has been there, just not the way.In our estimation the savings drawdown will put enough upward pressure on demand to enable JobKeeper to expire without a negative shock to the labour market materialising. JobKeeper is simply a wage subsidy that was designed to keep employees attached to their employers while restrictions artificially limited demand and negatively impacted sales. But once restrictions are more fully eased and demand bounces, the removal of a wage subsidy does not mean a business will retrench its staff. It simply means that wages will be paid from sales as has always been the case.(iv) The housing market is no longer a source of riskIn our view there have been two key sources of downside risk from the pandemic related to the housing market: (i) home prices falling sharply; and(ii) residential construction dropping significantly primarily because of lower net overseas migration (NOM). Those risks have diminished materially.On home prices it is clear that price falls will only end up being modest nationally. Indeed prices are rising now in most capital cities. We updated our dwelling price forecasts in early September to look for a 6% peak to trough forecast and a strong rebound in prices in H2 21. We believe the risks to our forecasts are skewed to upside. The RBA has lowered interest rates since we updated our home price forecasts and mortgage rates have declined as a result. In addition near term momentum indicators of the housing market have continued to strengthen and our home price model is signalling that solid price rises could be imminent (chart 11). As such, we expect a positive wealth effect to be in play over 2021 whereby rising home prices are a tailwind on household consumption, particularly on bigger ticket items like motor vehicles.On housing construction the forward looking indicators are encouraging. In August we published a thematic note where we noted that some unusual dynamics were impacting the outlook for housing construction. More specifically, we noted that new construction was likely to fall significantly due to lower net overseas migration, but that record low interest rates would support alterations and additions. Our views around renovation activity have come to fruition. Our lending data indicates there will be a big step up in alterations and additions which are worth 40% of total residential construction (chart 12).Where we have been genuinely surprised is around the building approvals data for new homes. The message here is that new construction will not drop too significantly. That poses a new risk around oversupply. But that risk is somewhat tempered by the prospect of a vaccine which will see net overseas migration return, albeit we think at a lower level than pre-COVID. We no longer expect dwelling investment to be a drag on the economy in 2021 and forecast growth in renovation activity to offset lower new construction (which will not decline as much as we previously expected).(v) Domestic tourism is set to boomRegular readers may recall that back in July we published a piece looking at the impact of international borders closures on the Australian economy. We highlighted that while international border closures would hurt Australian businesses that rely on foreign tourists, the overall macro-economic impact would be far less damaging. We reached that conclusion because Australians spend on average twice as much holidaying abroad compared with what is spent by overseas residents having a holiday in Australia (in 2019 Aussies spent $A47bn overseas vs $A23bn spent by overseas holidaymakers in Australia–chart 13).We remarked in the note, “the message therefore from policymakers becomes an easy one –if you were going to have an overseas holiday this year then please take one domestically and support Australian businesses! We suspect that regional Australia could do well from an expected lift in domestic tourism”.Now in many ways that story has not been able to unfold because there have been borders put up between states which serves as a big restriction on domestic tourism. Some parts of regional Australia have been doing well from domestic tourism, but things would be a lot stronger if interstate borders were fully open. Given the current status of COVID-19 in Australia we think that it cannot be too long before interstate borders are fully reopened. That will generate a massive lift in domestic tourism given the overseas borders remain closed and households are flush with cash. We expect next year to be a very positive story for regional Australia as domestic tourism booms.Updated forecastsWe have upwardly revised our profile for GDP. Our expectation for GDP to contract by 3.3% in 2020 is unchanged (we upwardly revised our assessment of H2 20 GDP in mid-September). But we now expect a much stronger recovery in 2021 and we have extended our forecast profile to end-2022.We now forecast GDP growth of 4.2% in 2021 (versus 2.5% previously). And we expect economic growth of 3.8% in2022. Our updated GDP profile sees us lower our profile for the unemployment rate. We now expect the unemployment rate to be 5.75% at end-2021 (vs 6.5% previously). And we forecast the unemployment rate to be 5.0% at end-2022. By comparison the RBA expects the unemployment rate to be 6.0% at end-2022.We assume a significant reduction in the savings rate because growth in consumption will outpace growth in income over the next two years. Indeed the savings rate will drop quite quickly initially. There is simply no reason for the savings rate to remain elevated, particularly when households as a collective are optimistic around the economic outlook.Our central scenario is for inflation to remain low over our forecast horizon because the economy will have an output gap until end-2022. However we continue to point out to readers that there is upside risk to modelled inflation because there is a large disparity at present between wages growth and household income growth. The longer this disparity persists the greater the risk that inflation outcomes are higher than modelled inflation would imply. We think that there is a non-trivial risk that inflation rises at a faster pace than our forecasts indicate. In our view the risks around our inflation forecasts are clearly skewed to the upside. Table 1 below contains our updated quarterly profile for GDP, employment, unemployment and inflation.Monetary policy implicationsOur updated forecasts for the economy do not have any implications for our views on the RBA cash rate target over our forecast horizon (end-2022). We expect the cash rate to be left on hold at 0.10%. Indeed in the Governor’s Statement accompanying the November Board meeting where a suit of easing measures were introduced it was noted that, “the Board is not expecting to increase the cash rate for at least three years”.However, we think that the economy will be on a sufficiently entrenched path of improvement by the middle of next year that the RBA will need to either remove or increase the target yield on the 3 year Australia Commonwealth Government Bond (ACGB). For as long as the target on the3 year ACGB sits at the same level as the cash rate the RBA is implying that the cash rate will remain on hold for the next three years. The middle of next year is still some time away, but it is worth considering now how these dynamics are likely to play out given our updated views on the outlook for the Australian economy.In summary we believe the metaphorical ‘bridge’ has been built very well and sets Australia up for a prosperous next two years. We think that provided transmission of COVID-19 in Australia remains low, particularly community transmission, the strength of the economic recovery in 2021 will surprise many.