Australia’s mortgage cliff shrinks to $133 billion

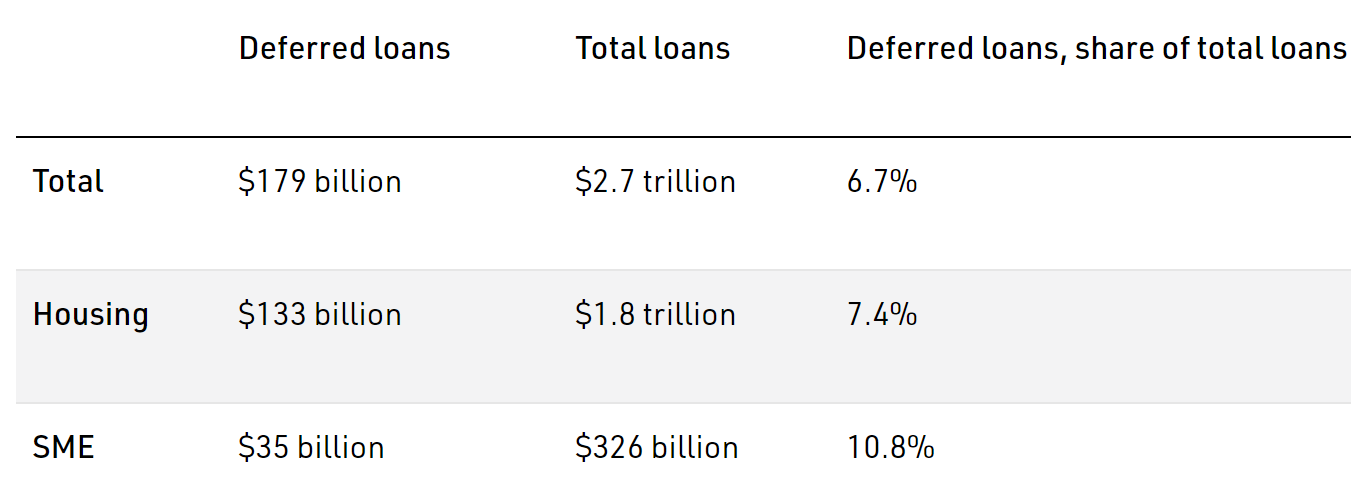

The Australian Prudential Regulatory Authority (APRA) on Friday updated its loan deferrals data to September 2020, which revealed that there were still $179 billion loans outstanding as at 30 September, accounting for 6.7% of total loans outstanding by value:

The volume of deferred mortgages was $133 billion in September, accounting for 7.4% of total housing loans outstanding by value. This was down from a peak of $192 billion in May (11% of outstanding mortgages).

In number terms, 324,894 mortgages were deferred as at 30 September, accounting for 6% of total mortgage facilities. This was down 68,573 from September (when 393,467 mortgages were deferred) and down 163,355 from May’s peak when 488,249 mortgages were deferred (accounting for 9% of mortgage facilities).

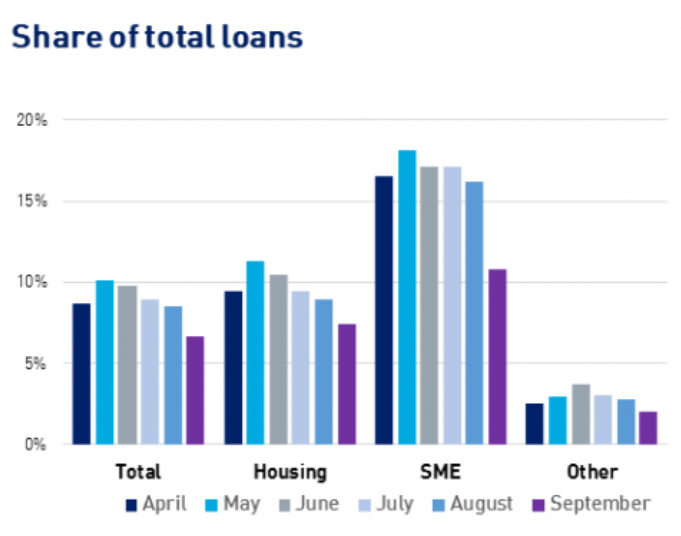

In fact, the share of mortgages deferred in September (7.4% by value) was the lowest its been since the beginning of the pandemic:

APRA has permitted banks to extend mortgage repayment relief until March 2021.

It will be interesting to see what happens when the various emergency income supports – e.g. JobKeeper and the JobSeeker supplement, as well as early access to superannuation – are unwound over the next six months.