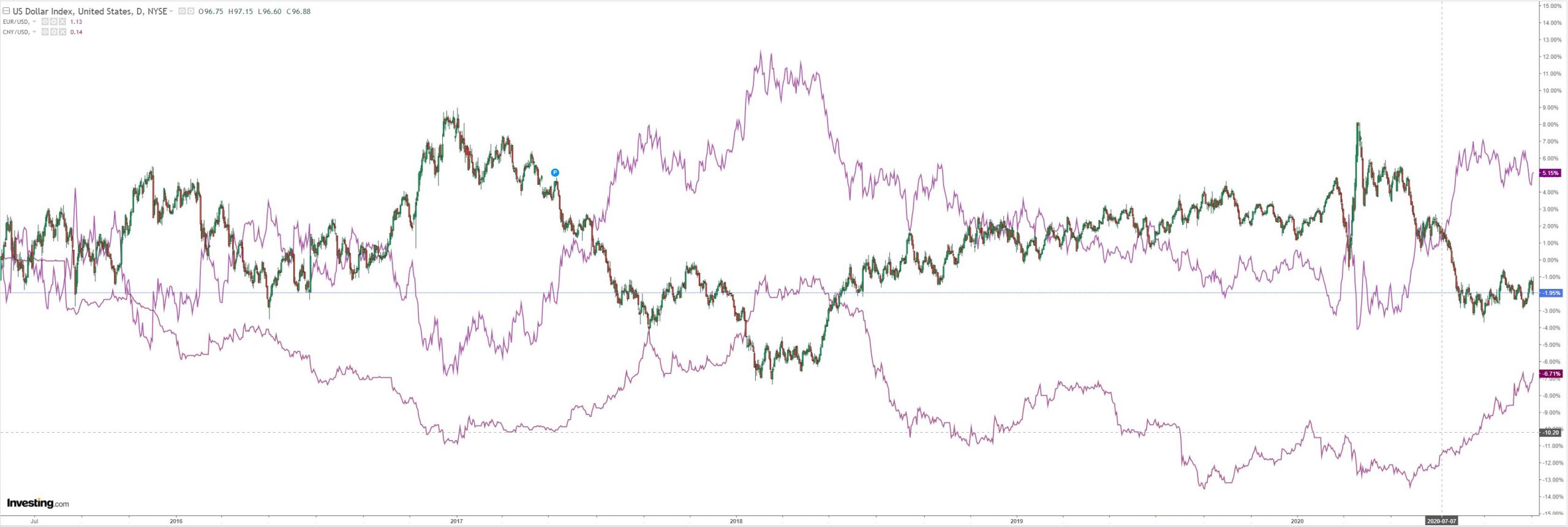

DXY sank last night:

The Australian dollar had one wild day:

Gold was subdued:

Commodities bounced:

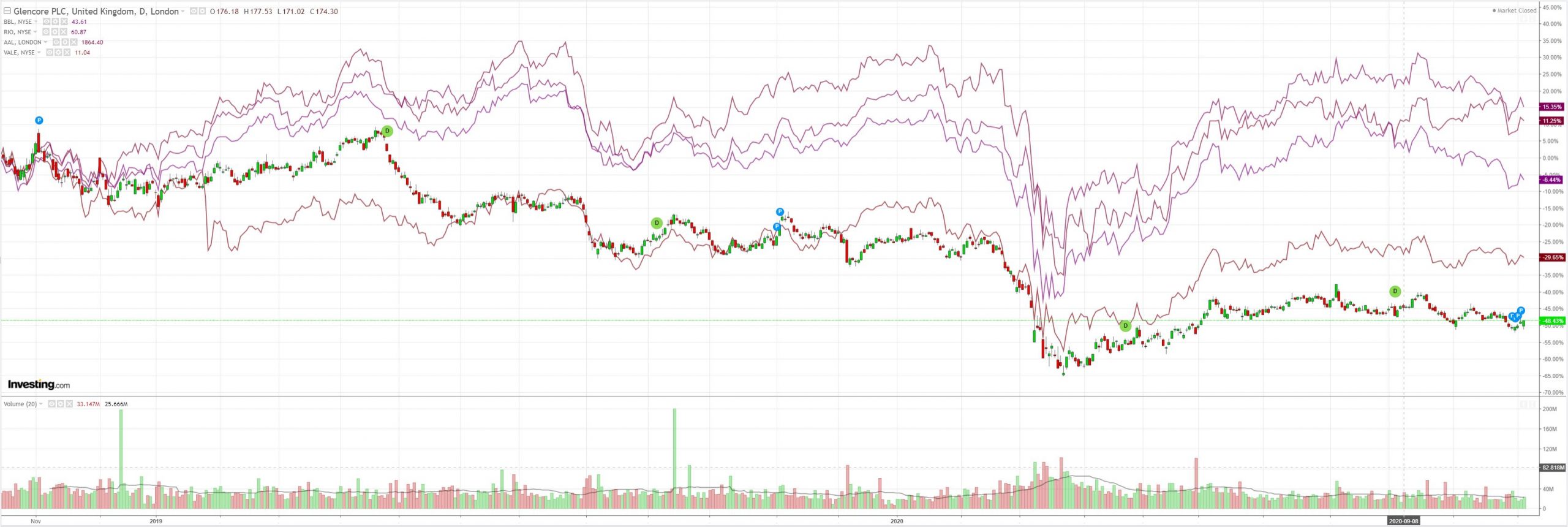

Miners fell:

EM stocks went nuts:

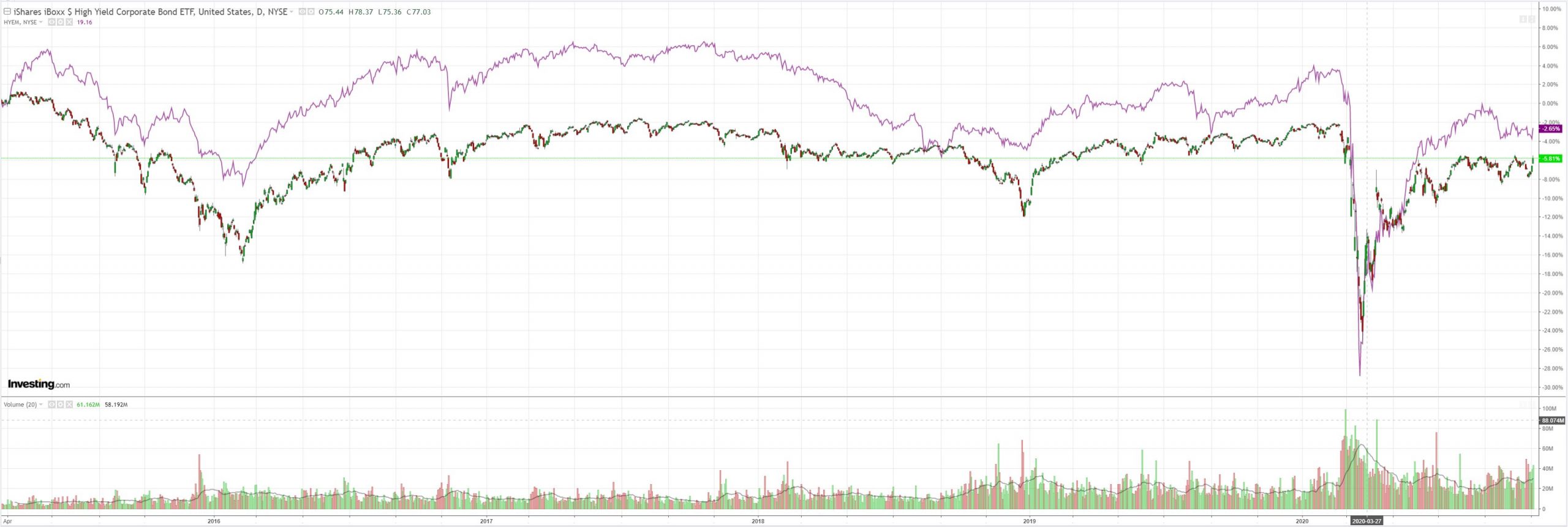

As junk jumped:

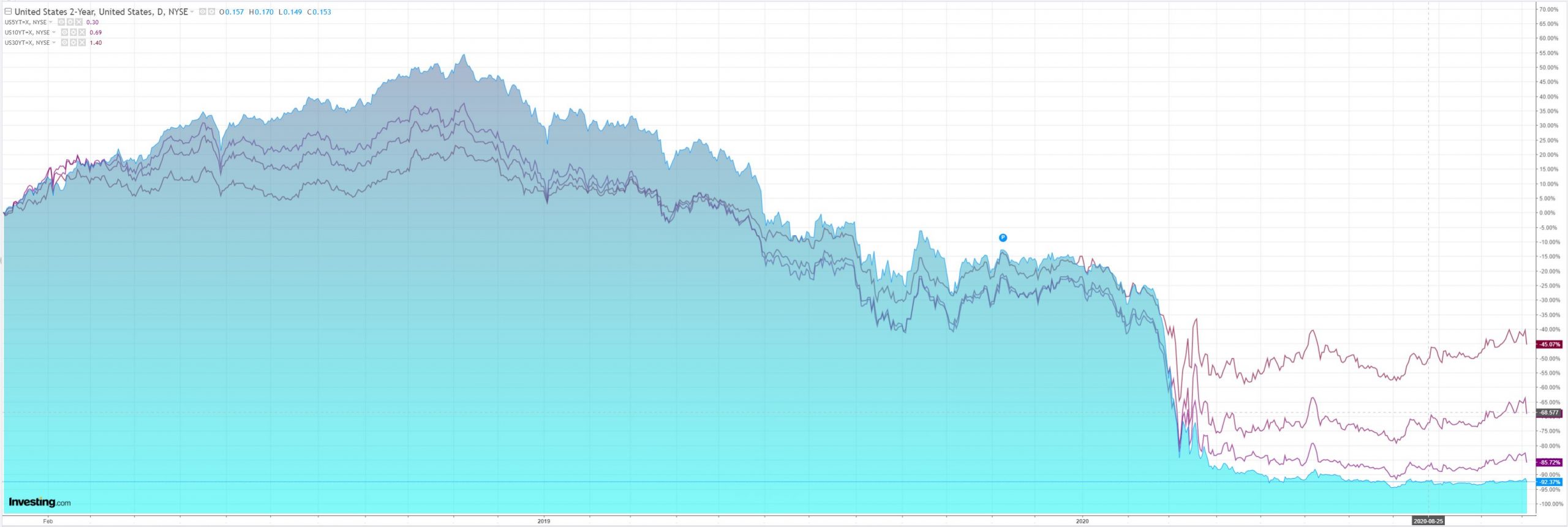

While Treasuries crashed:

And stocks soared:

Westpac has the wrap:

Event Wrap

US service sector ISM fell to 56.6 (est. 57.4, prior 57.8), reflecting the potential of a slowdown in growth in Q4, as well as the failure of pre-election stimulus talks. A pullback in the employment component to 50.1 was notable. Final Markit service PMI firmed to 56.9 (est. 56.0, prior 56.0) – its highest reading since 2015, on the back of stronger new business, although it too showed a pullback in employment. October’s ADP employment report showed a disappointing 365k rise against estimates of 650k.

Eurozone final Markit service sector PMIs edged above their flash readings (of 46.2) to 46.9, pushing the region’s composite PMI to the inflection level of 50.0.

UK final Markit service sector PMI fell to 51.4 (flash 52.3), pulling the composite down to 52.1 (flash 52.9), amid pandemic and lockdown concerns and fears of “a double-dip recession”.

Event Outlook

Australia: Westpac expects the trade surplus to widen in Sept to $5.2bn as imports pull-back and exports lift (market f/c: $3.7bn).

NZ: Domestic activity indicators have been picking up, supporting ANZ business confidence in Nov (prior: -15.7).

Euro Area: The rebound in retail sales will stall in Sep as containment measures to manage COVID-19’s resurgence are instituted (prior: 4.4%, market f/c: -1.5%).

UK: The BoE will take careful note of growing downside risks at its policy meeting as England begins its second nationwide lockdown.

US: The market expects initial jobless claims to fall slightly from 751k to 735k.

The FOMC’s November meeting will conclude today; we expect the meeting communications to focus on risk and uncertainty rather than the positive Q3 GDP result.

So, after a few weeks of Trump legal tantrum, on the balance of probabilities Democrats will take the White House and Republicans retain the senate. This sets the US economy up for:

- 10 weeks of a lame-duck regime determined to exact its revenge (probably by unleashing the virus);

- a new Biden Administration that will have to lock down the moment it takes power:

- and not enough stimulus throughout any of it:

In its wisdom, the market has determined that this sequence of events is outrageously bullish for stocks as the economy rolls into another depression in both the US and Europe:

Call me skeptical. Even though it raises the prospect of more help from the Fed and the much yearned for negative interest rates. That won’t come without a market crash first, which remains a very distinct possibility.

As for forex and the AUD, it will get pushed around by whatever happens next in this grand fiction formerly known as capitalism.