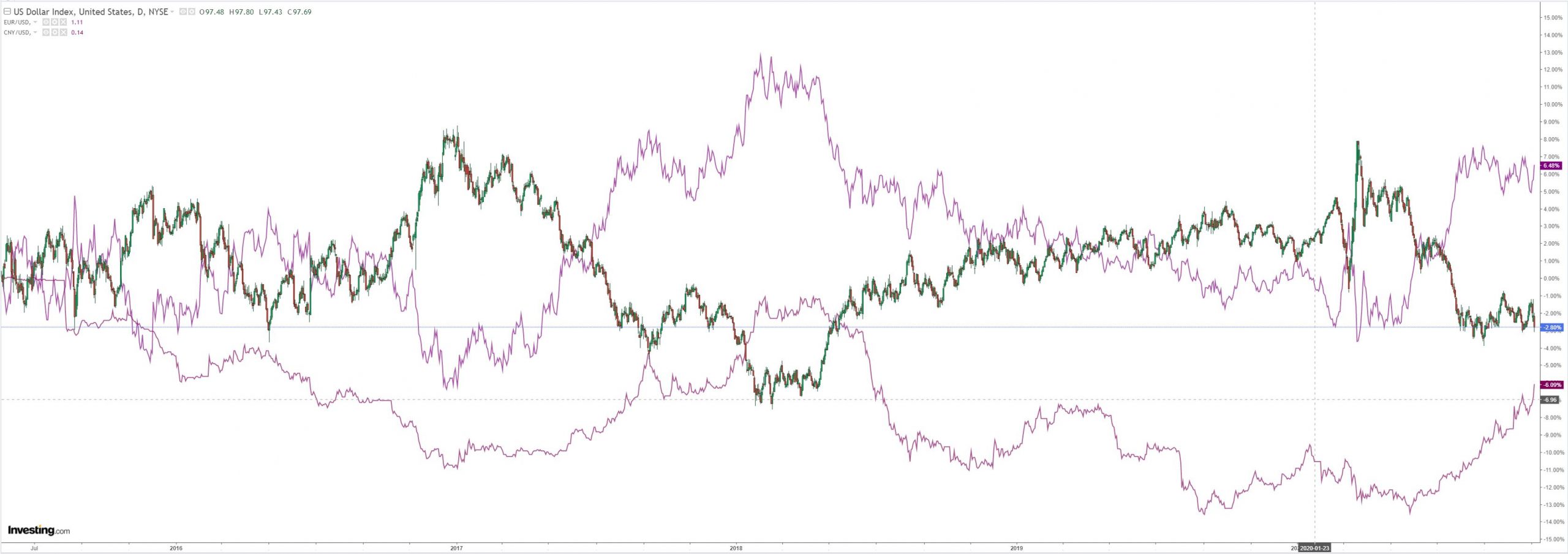

DXY was slammed last night:

The Australian dollar is a cork in the storm:

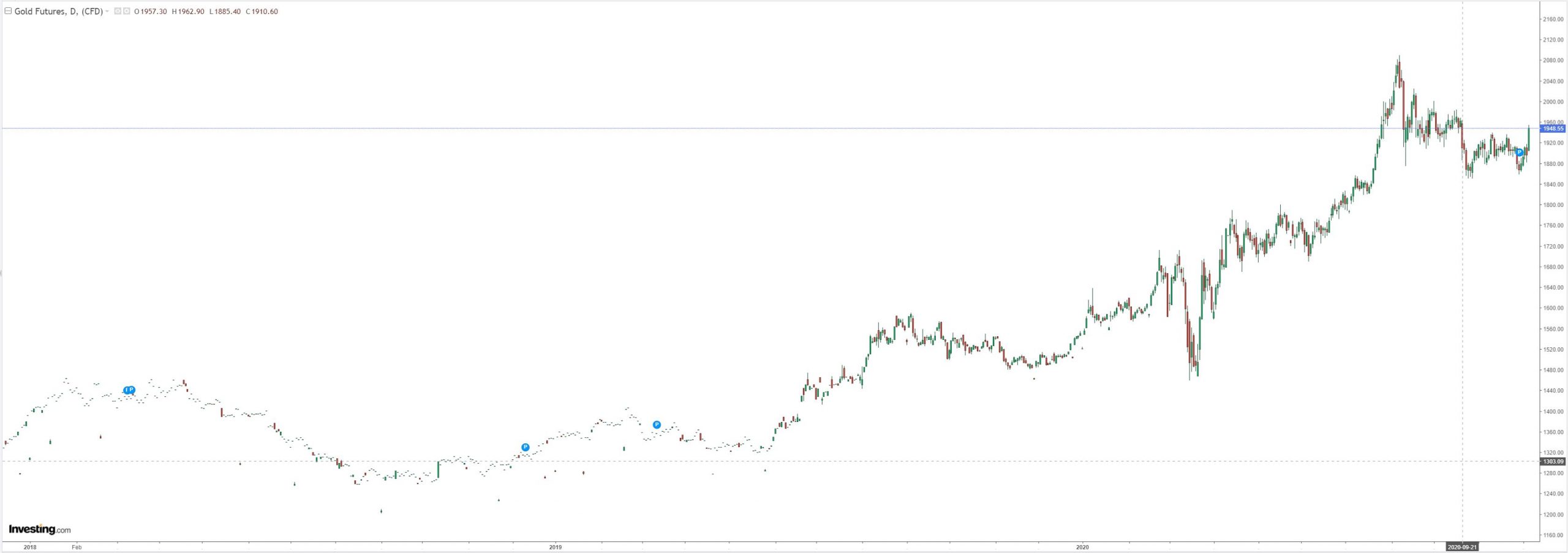

Gold jumped:

Oil fell:

Metals ground higher:

Miners were mostly stronger:

EM stocks gapped into madness:

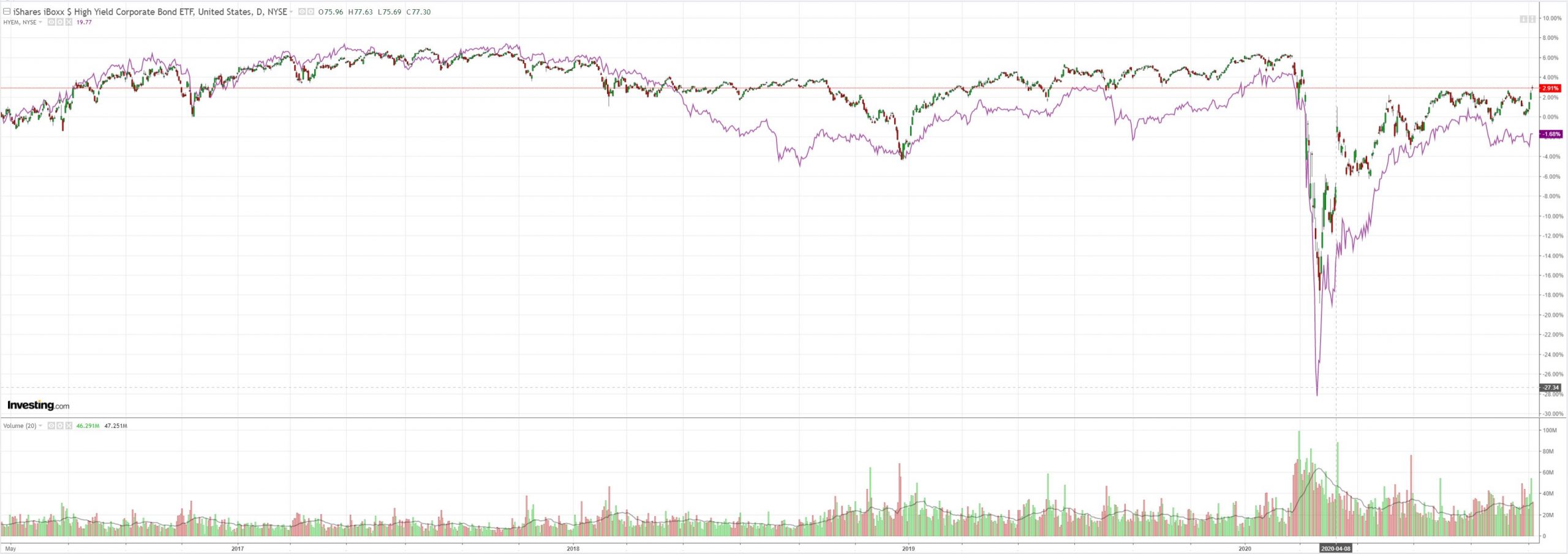

Junk whoa:

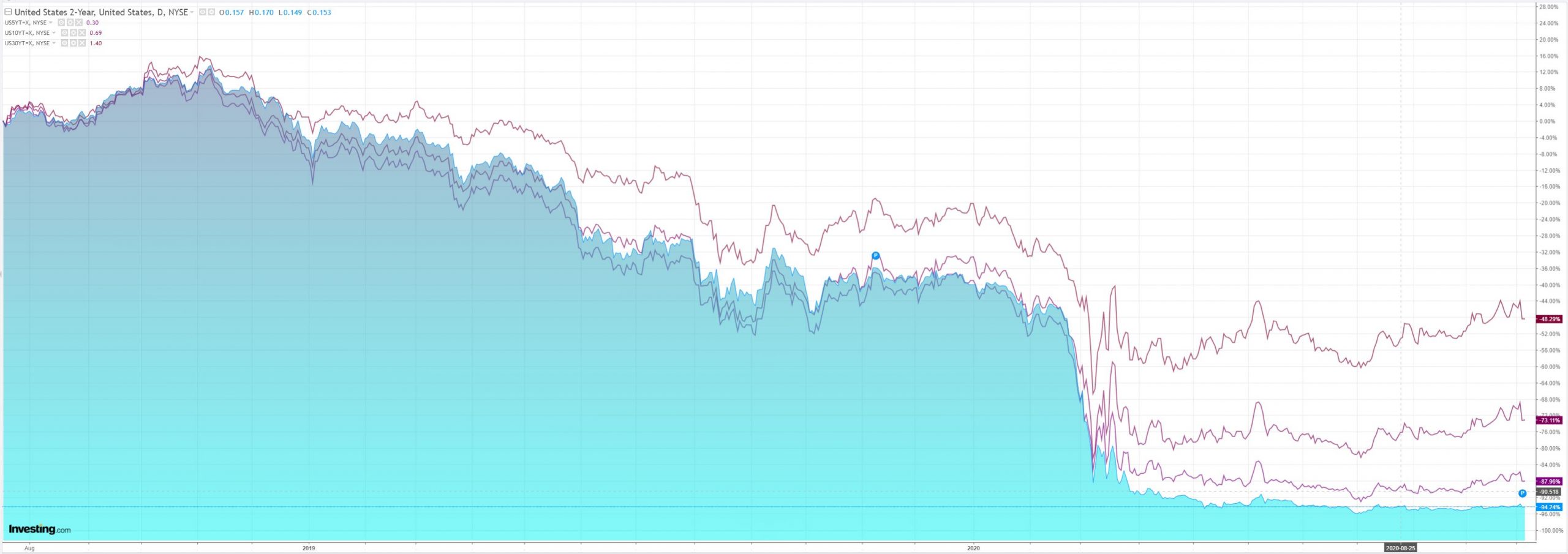

US yields were stable:

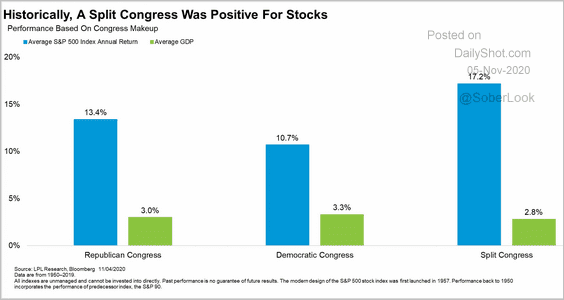

Stcoks were anything but:

We’ve caught the express train from a dangerous double-top to verging on new highs for the bubble. The reason? Because Joe Biden can’t do anything post-election with a Republican senate the Fed will have to do MOAR so buy stocks!

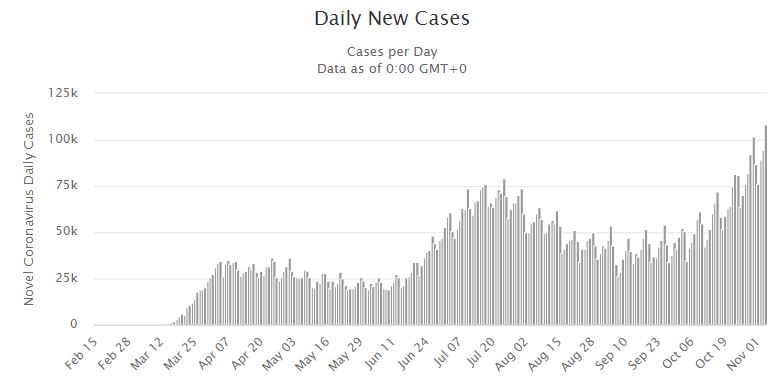

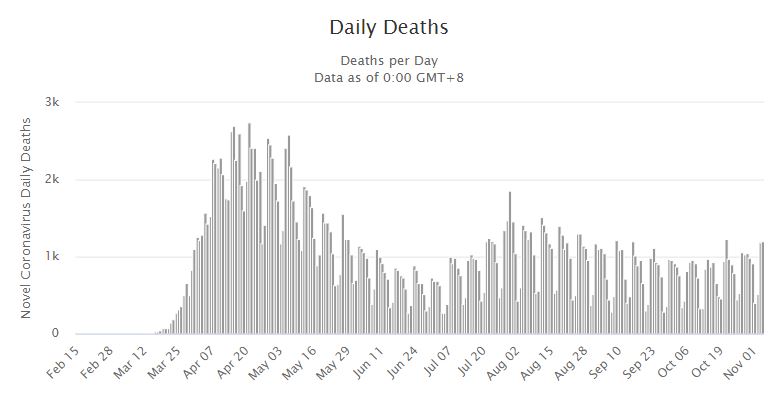

Needless to say, with valuations already extreme and the virus running wild:

An already slowing US economy with limited at best fiscal support coming:

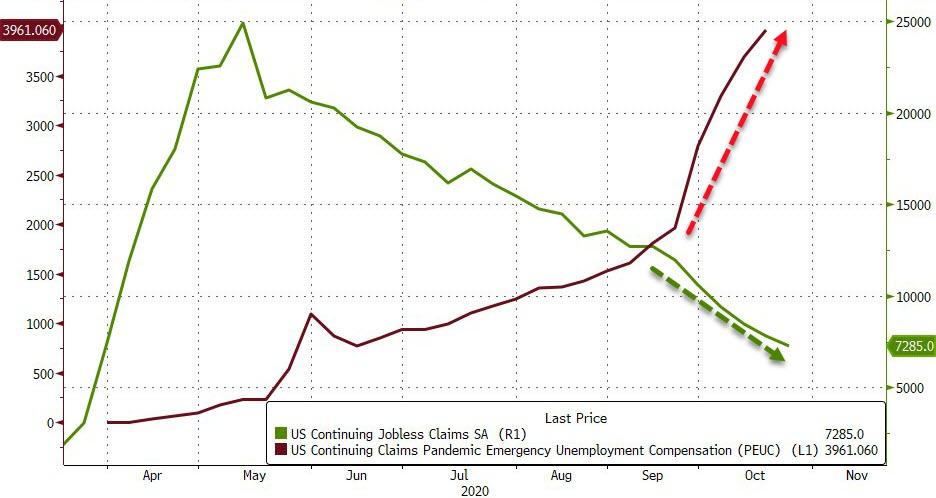

And a slowing jobs recovery:

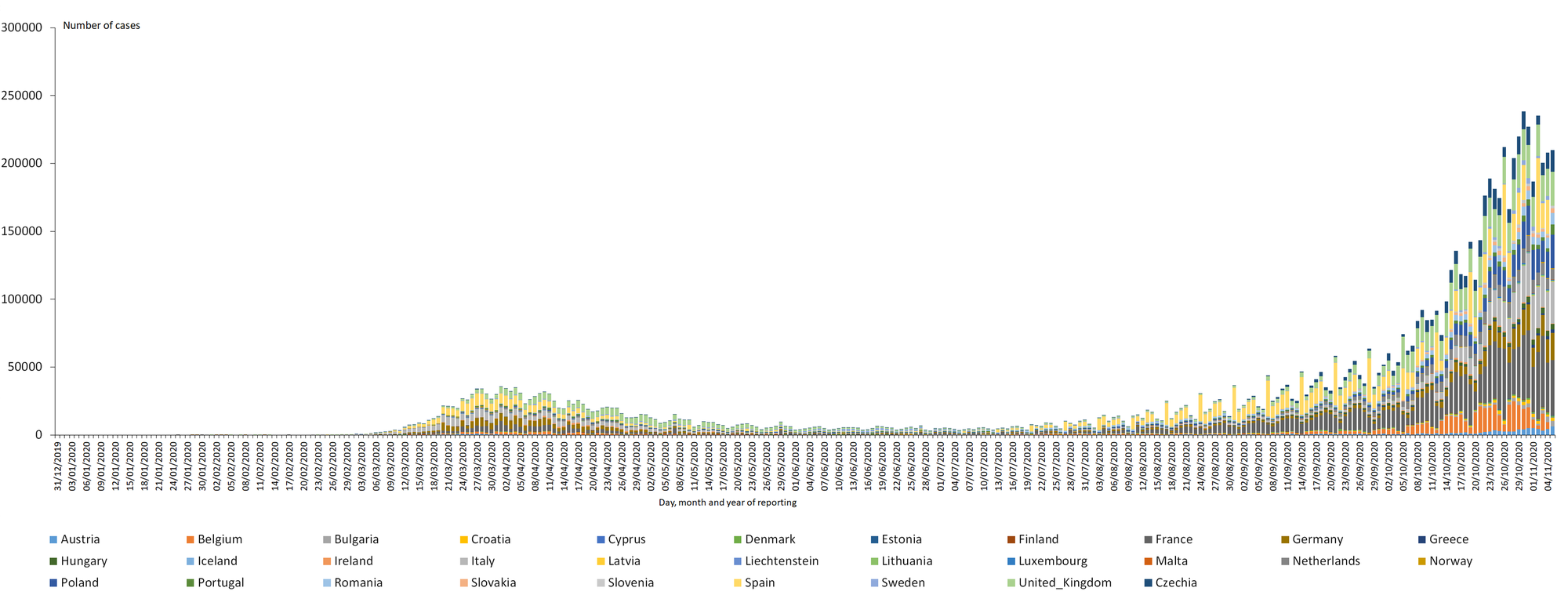

Plus Europe shut down:

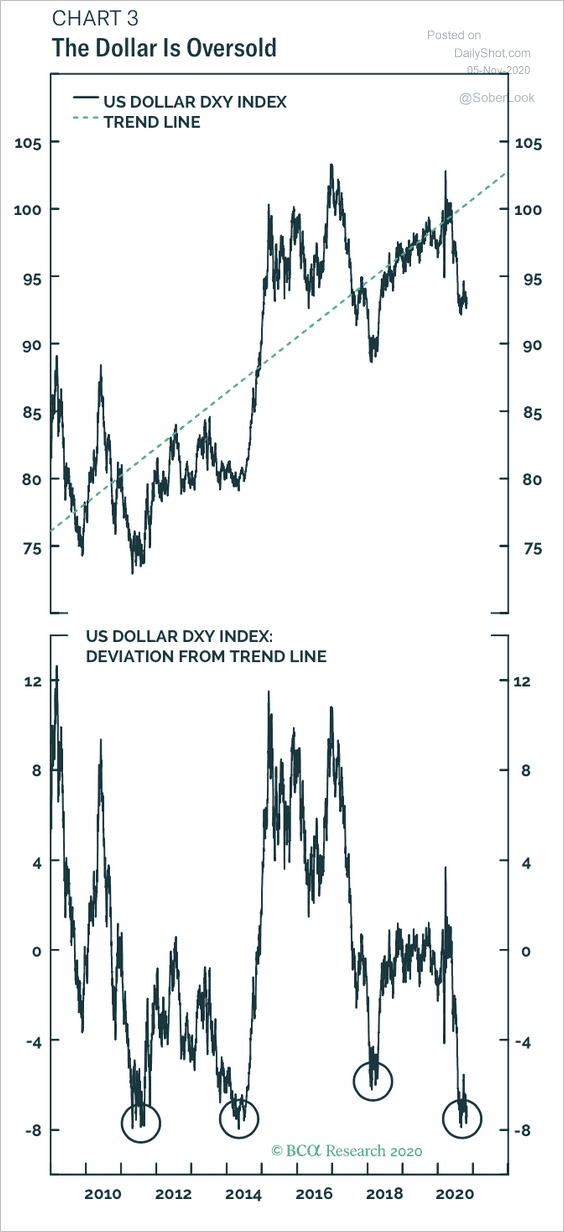

And DXY extremely oversold:

One has to ask again what has happened to risk pricing as earnings are clearly headed for a new shock. The answer is “don’t fight the Fed”. Ironically, with this Pavlovian response so thoroughly embedded, the Fed doesn’t actually need to do anything, which it didn’t:

The Federal Reserve is committed to using its full range of tools to support the U.S. economy in this challenging time, thereby promoting its maximum employment and price stability goals.

The COVID-19 pandemic is causing tremendous human and economic hardship across the United States and around the world. Economic activity and employment have continued to recover but remain well below their levels at the beginning of the year. Weaker demand and earlier declines in oil prices have been holding down consumer price inflation. Overall financial conditions remain accommodative, in part reflecting policy measures to support the economy and the flow of credit to U.S. households and businesses.

The path of the economy will depend significantly on the course of the virus. The ongoing public health crisis will continue to weigh on economic activity, employment, and inflation in the near term, and poses considerable risks to the economic outlook over the medium term.

The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. With inflation running persistently below this longer-run goal, the Committee will aim to achieve inflation moderately above 2 percent for some time so that inflation averages 2 percent over time and longer-term inflation expectations remain well anchored at 2 percent. The Committee expects to maintain an accommodative stance of monetary policy until these outcomes are achieved. The Committee decided to keep the target range for the federal funds rate at 0 to 1/4 percent and expects it will be appropriate to maintain this target range until labor market conditions have reached levels consistent with the Committee’s assessments of maximum employment and inflation has risen to 2 percent and is on track to moderately exceed 2 percent for some time. In addition, over coming months the Federal Reserve will increase its holdings of Treasury securities and agency mortgage-backed securities at least at the current pace to sustain smooth market functioning and help foster accommodative financial conditions, thereby supporting the flow of credit to households and businesses.

In assessing the appropriate stance of monetary policy, the Committee will continue to monitor the implications of incoming information for the economic outlook. The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee’s goals. The Committee’s assessments will take into account a wide range of information, including readings on public health, labor market conditions, inflation pressures and inflation expectations, and financial and international developments.

So long as DXY falls then fakeflation redux can run. But how far it gets is, once again, entirely a matter for sentiment.

Ditto Australian dollar.