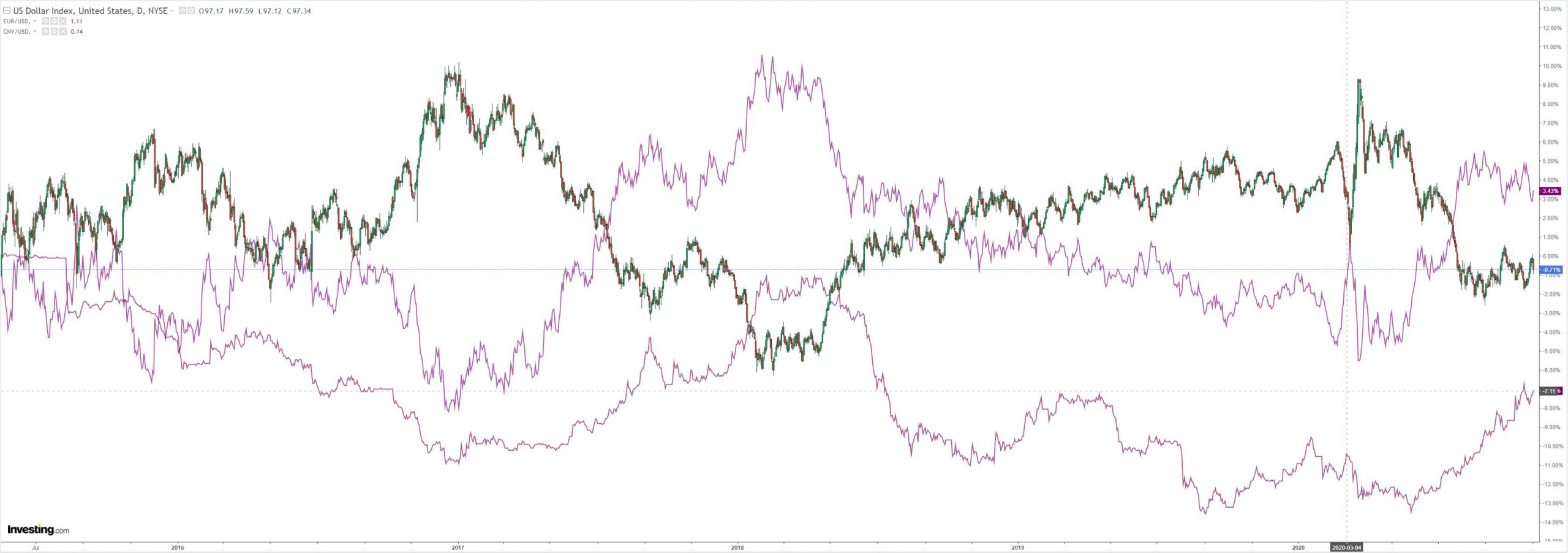

DXY got hammered last night:

The Australian dollar blasted off:

Gold was firmer:

Oil too:

And metals:

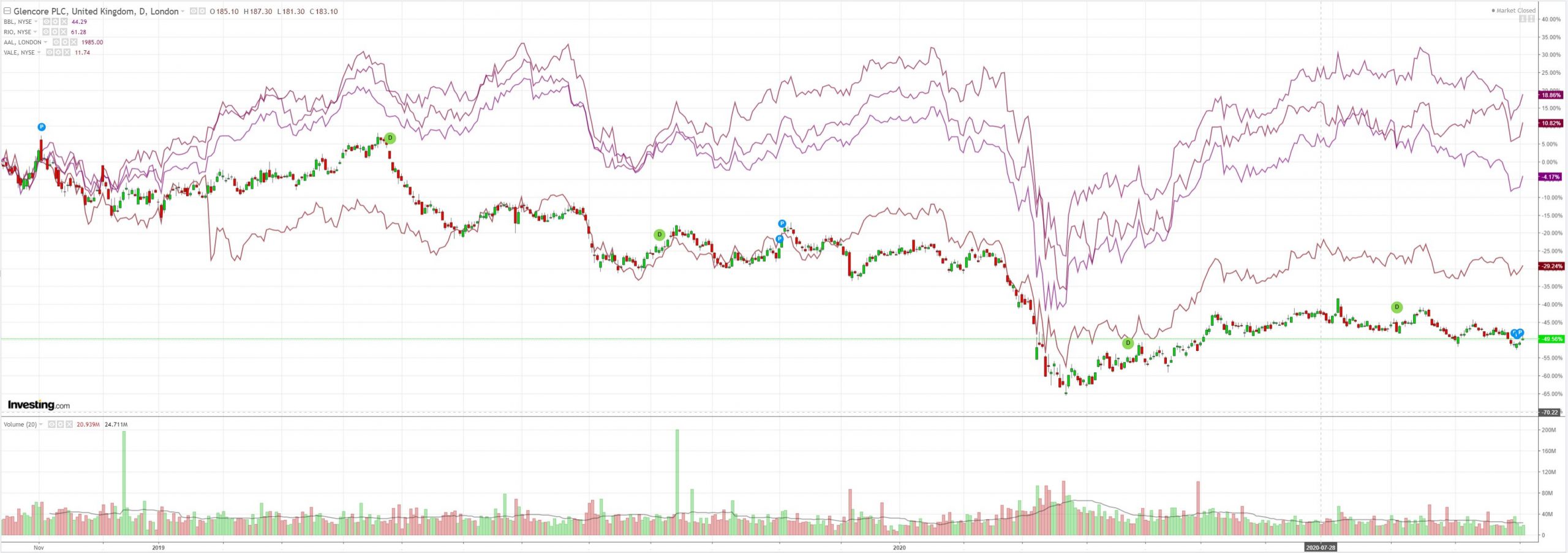

Miners went vertical:

EM stocks lifted:

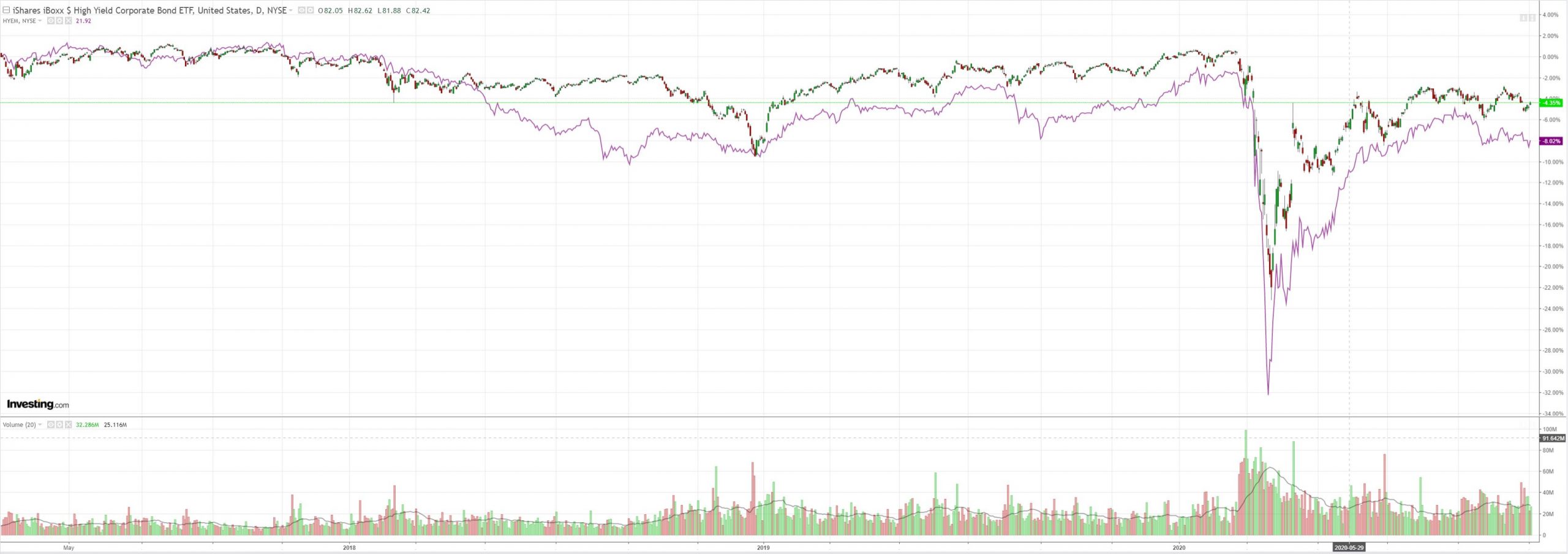

Junk firmed:

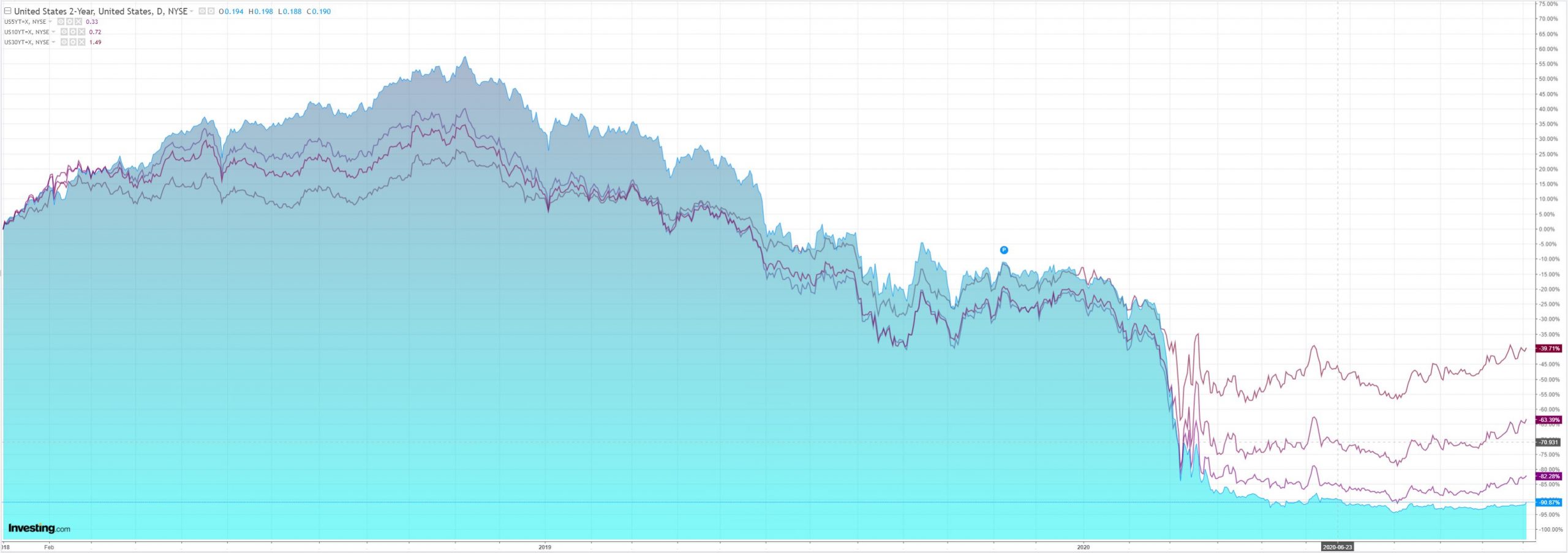

Treasuries sold again on the inflation bogey:

Buy stocks!

Westpac has the wrap:

Event Wrap

US September factory orders rose +1.1%m/m (est. +1.0%m/m, prior +0.6%m/m revised from +0.7%m/m). Ex-transport came in at +0.5%m/m (est. +0.6%m/m. prior +0.9%m/m revised from +0.7%m/m). Durable goods orders were little changed from their preliminary readings.

Event Outlook

Australia: Preliminary estimates showed a 1.5% decline in Sep retail sales; but Q3 real retail sales will still be up very strongly, circa 6%. Weekly payrolls (to Oct 17) continue to record small moves around a flat trend (prior: -0.4%).

NZ: Westpac expects the Q3 unemployment rate to rise to 5.5% in Q3 (market f/c: 5.3%) following a surprise drop to 4.0% in Q2 as lockdowns hindered job-seekers. Wage inflation will likely be subdued in the post-Covid environment (Westpac f/c: 0.3%, market f/c: 0.2%).

China: The Caixin services PMI should point to external and domestic demand remaining robust (prior: 54.8, market f/c: 55).

Europe: Government lockdowns are expected to hit the Markit services PMIs hard in the Euro Area and UK.

US: ADP employment is expected to see a gain of 650k on continued service-sector hiring (prior: 749k). Another month of expansion appears likely in the Oct Markit service and ISM service PMIs given measures of mobility improved in the month (prior and market f/c: 56). The trade deficit narrowed in Sep, with imports falling slightly as exports recovered (prior: -$67.1bn, market f/c: $63.9bn).

Results for the 2020 US Presidential Election are expected to start coming in around midday Wednesday ADST (2pm NZT).

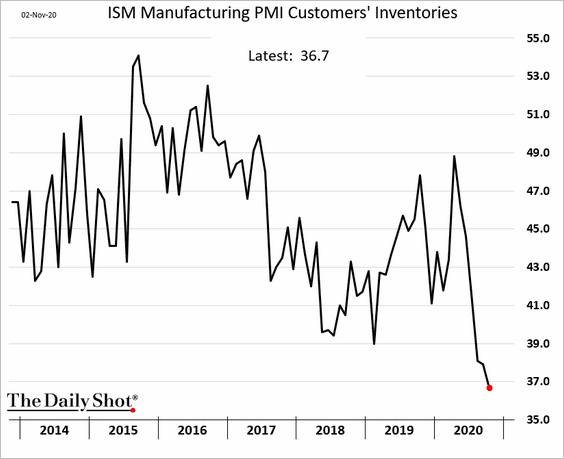

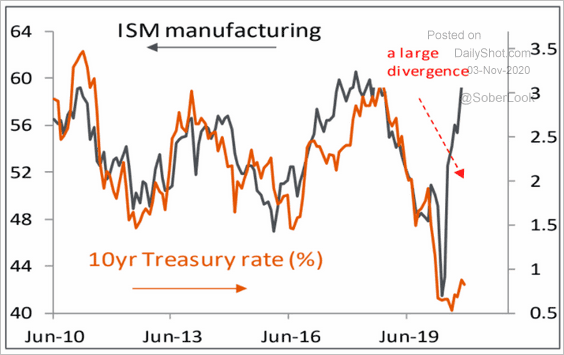

A few points on the data. The tearaway ISM is important in terms of this chart:

This has a lot of economic support embedded in it despite the second wave pandemic shock across the Atlantic. The first round of lockdowns triggered a huge inventory cycle in manufacturing and the rebuild will take six to twelve months. It means that as services roll into a swan dive, manufacturing and trade will not.

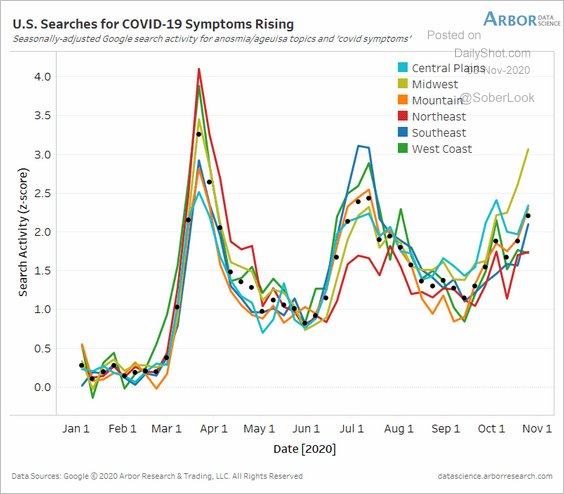

That said, services will!

With predictable results:

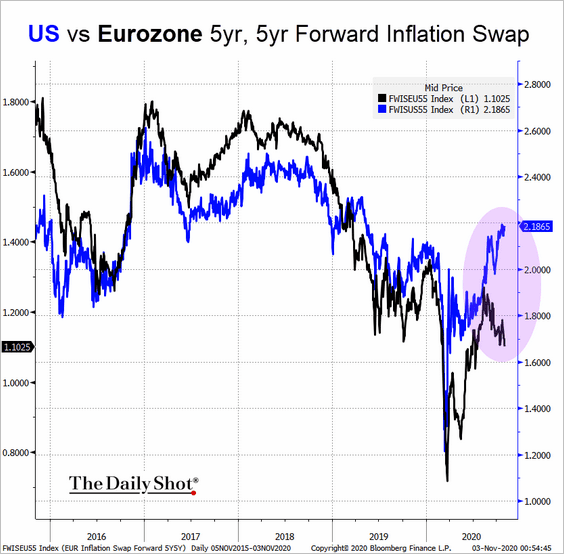

The most intriguing question at this point for forex is will DXY keep falling as the Biden Administration arrives? Normally it takes a US recovery to do it. That’s off the table. And the imagined fiscal support is already driving a massive upswell in US versus European yields:

The election will decide it, I guess. Blue Wave equals weak DXY. Blue/Red favours strong DXY as does Red Coup.

The Australian dollar is the plaything of this outcome for now.