DXY is stalled perhaps in part by the European virus which hardly makes a EUR bid exciting:

The Australian dollar likewise

Gold bounced:

Advertisement

Oil took off. There’s a glut but the market wants more:

Metals were firm:

Advertisement

Miners have reversed spectacularly:

EMs fell:

Junk is fine:

Advertisement

As US yields back-up some more:

Which did not help stocks as the tech, growth and momentum bubble deflates:

Advertisement

Westpac has the wrap:

Event Wrap

US NFIB small business confidence survey held steady at 104.0 (vs. est. 104.1), remaining above the average for 2019 (103.0).

Eurozone ZEW investor confidence survey weakened slightly. The benchmark German expectations index slipped to 39.0 (est. 44.3, prior 56.1), with current conditions falling to -64.3 (est. -63.5, prior -59.5). The Eurozone expectations component pulled back to 32.8 (prior 52.3), with current conditions almost unchanged at -76.4 (prior -76.6).

Other national level data in Europe was mixed, albeit dated. French 3Q unemployment was high at 9%, (vs. est. 7.5%), but Sep. industrial production was solid at +1.4%m/m (vs. est. +0.7%m/m). Italian Sep. industrial production fell -5.6%m/m (vs. est. -2.0%m/m).

UK labour data was solid. September’s unemployment rate was in line, rising to 4.8% (3m/yoy) from 4.5% in August, with the 3m/3m decline in employment at -164k – slightly more than the est. of -150k (prior -153k).

Event Outlook

Australia: The Westpac-MI Consumer Sentiment Survey surged 11.9% in October, driven by the well-received Federal Budget, ongoing success containing the pandemic locally, and increasing expectations of further RBA easing. Domestic developments have been mostly positive ahead of the November update, but outbreaks offshore have worsened materially.

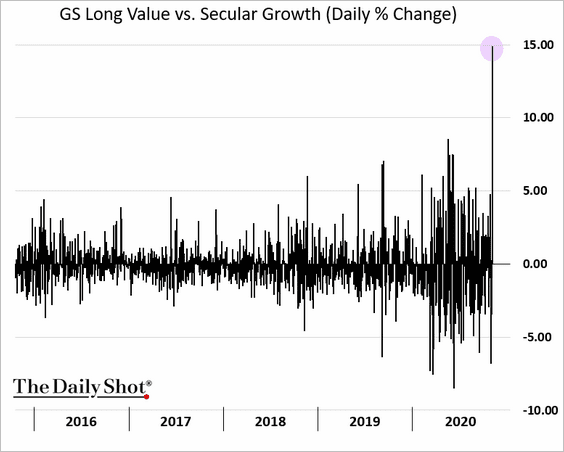

To get an idea of how radical was yesterday’s market moves as growth swung to value get a load of this:

Here’s a chart from Wolfe Research which shows just how extreme this reversal has been. It deals with the price moves from Monday’s trading session, and breaks down all listed US companies listed by industry groups before placing each of them into various baskets, measuring things including dividend yield, book-to-market and return on equity. It then charts the way in which the equities of those companies falling into each basket performed over the course of yesterday. As you can see, book-to-market (ie companies that are cheap relative to their book value) and high dividend yield stocks crushed it. High expected growth and momentum stocks got pummelled (open in a new tab to make it large): In fact, the moves were pretty damn bonkers: Based on historical data, the book-to-market enjoyed a 12x standard deviation rally, while price momentum and short-term growth factors suffered from 20x and 25x sigma sell-offs, respectively, on November 9.

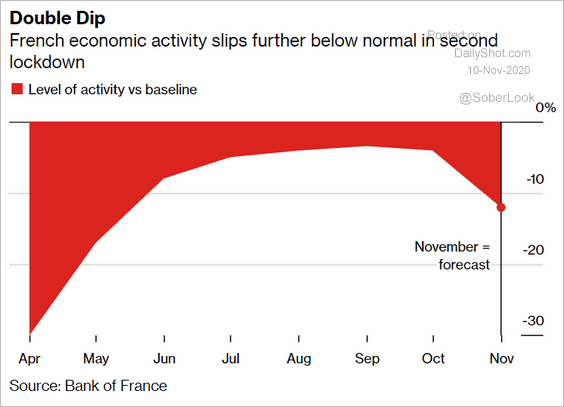

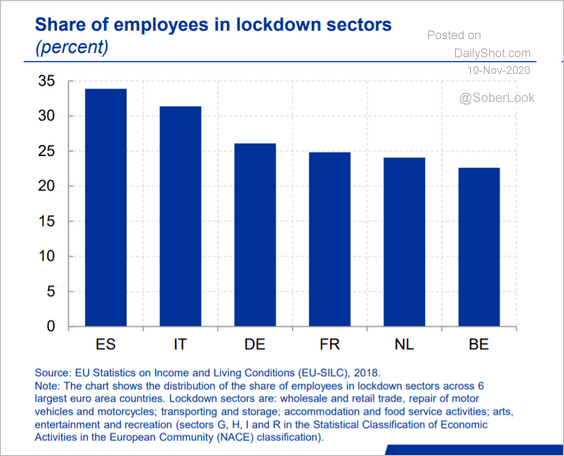

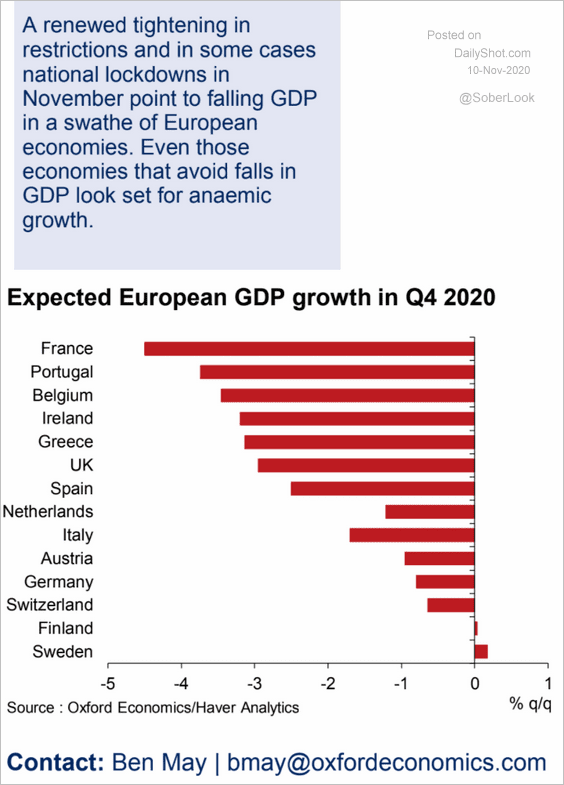

The market continued with it today. But there’s a big problem. It’s called the virus. Europe is stalling big time:

Advertisement

And the US is next:

With no or minimal fiscal support:

Advertisement

When the hospitals are overwhelmed and the mortality rate skyrockets, the US private sector is going to lock down in defiance of Trump’s revenge on the American people.

Don’t get me wrong, the vaccine wave is real and coming later in 2021 but there’s another tsunami already crashing into the shore and it does not favour value.

The Australian dollar is unlikely to rise while that is the case.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.