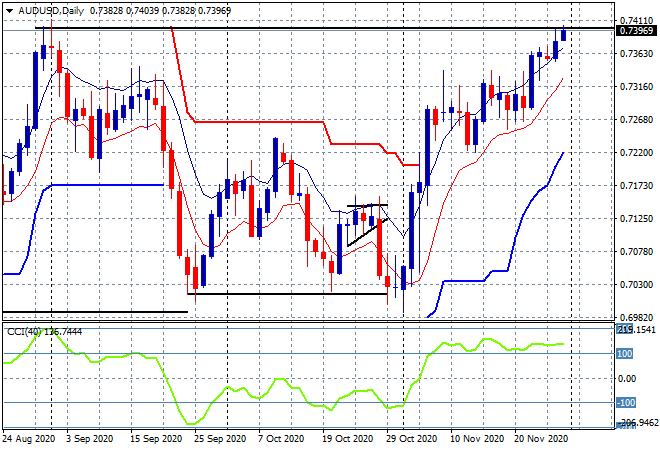

The Australian dollar has been on fire since the US presidential election and the announcement of some successful COVID vaccines, having breached 74 cents against USD and matching its August highs:

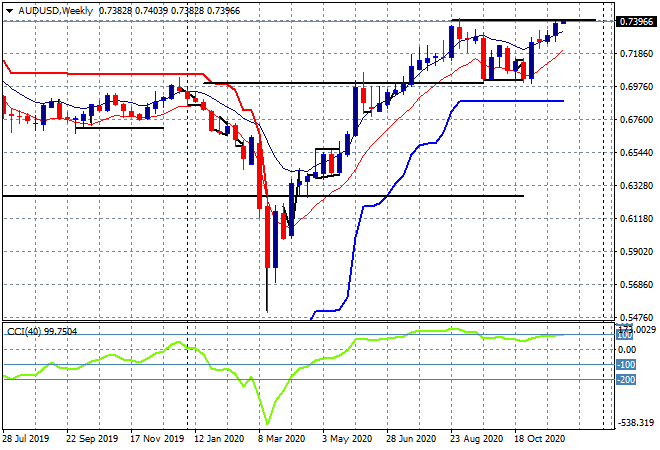

This has been a long road of recovery for the Pacific Peso, having dropped from circa 70 cents to the low 50’s before matching the rise of equity markets and now past those pre-pandemic highs:

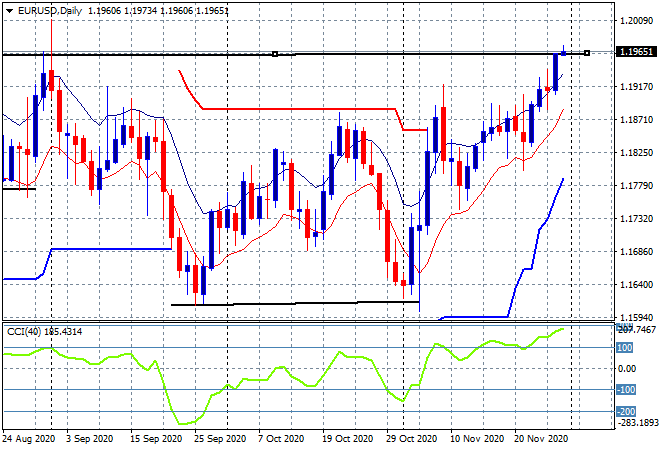

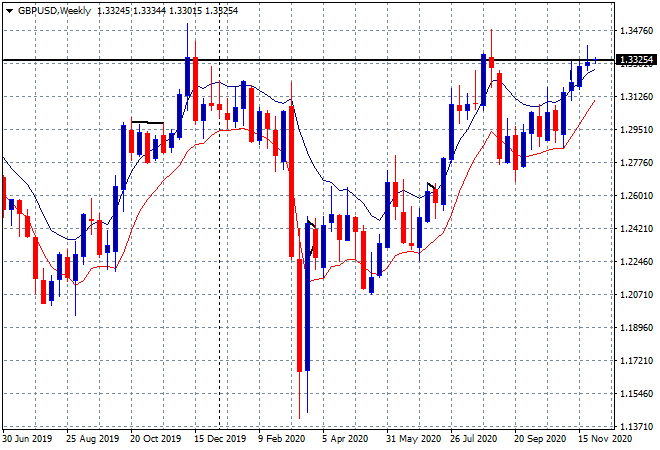

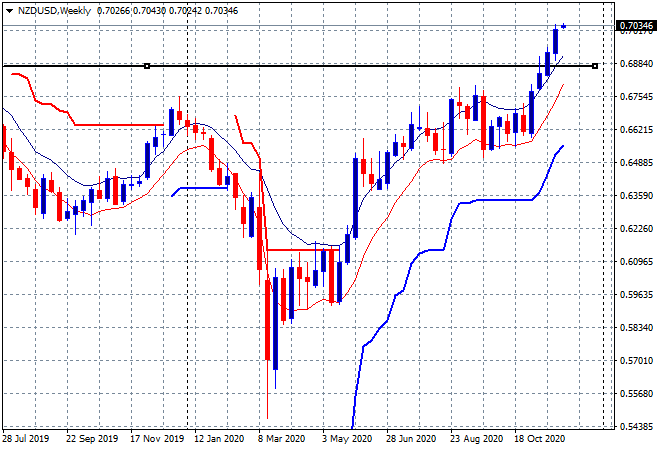

But it’s not just the Aussie, with Kiwi, Pound Sterling and Euro all embiggened by the “turning ’round the corner” situation that the vaccine developments made possible, with the added bonus of an actual adult in the White House in the new year:

Notably, the Kiwi has surpassed all expectations as the RBNZ was heading towards a negative rate, although this maybe about to change with as more easing hopes are dashed. From Bloomberg:

Finance Minister Grant Robertson added fuel to the fire last week when he suggested the central bank take into account house prices in setting policy, with the move seen as diminishing the chances of further easing.

Markets now expect the central bank to leave its official cash rate unchanged at 0.25%, with overnight index swaps pricing in a 30% probability of one 25-basis point reduction by end-2021. Just a month ago, they almost fully priced in a -0.25% cash rate next year.

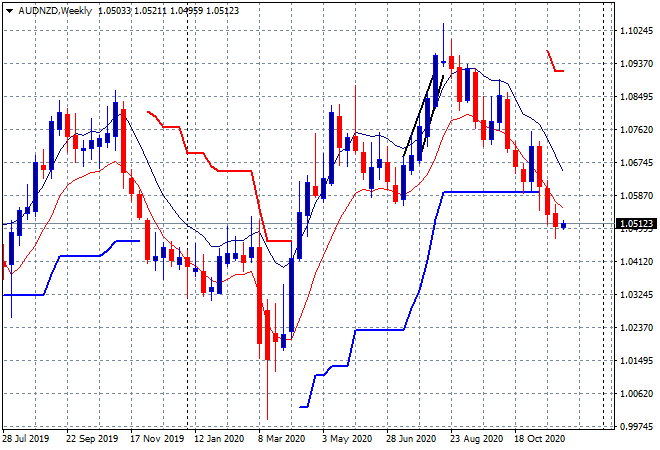

Technicals show the kiwi’s rally against the Aussie is looking stretched as slow stochastics, a momentum indicator, indicates the New Zealand dollar is in overbought territory. This suggests that the Aussie’s decline against the kiwi may have run its course.

Furthermore, the bank is looking to bring back mortgage lending restrictions two months earlier than planned, having ditched prudence in May this year as the pandemic shutdown bit down on house prices. From RA:

Despite the large decline in economic activity earlier in the year, housing market activity and housing credit growth have rebounded strongly,” the RBNZ says. “A growing share of this lending is going to borrowers with low deposits, making these borrowers’ balance sheets more vulnerable to a correction.”

“If this trend were to continue, the stock of low-deposit home loans on banks’ books would gradually rise to a level that would constitute a risk to financial stability.”

A similar scenario is developing with the RBA meeting tomorrow, the final one for the year and indeed until February 2021. It’s also before the 3Q GDP print, although most of the inputs are a known – with the particularly troubling lack of private capital spending again unable to offset the profligate mortgage debt creation in its place.

A longer than expected recovery in 2021 is on the cards here, which could be a big headwind for the Aussie dollar, although the AUDNZD cross might play catchup first, having diverged from the other currency trends post the Biden election result: