DXY was down last night:

But the Australian dollar fell anyway:

Gold weakened again, oil lifted:

Metals are on a tear:

Miners struggled:

EM stocks did OK:

Junk is back:

Treasuries were bid:

Stocks did the two-step reversion from value to growth as yields fell. Can’t lose:

Westpac has the wrap:

Event Wrap

US weekly initial jobless claims were slightly higher than expected at 742k (est. 700k), but continuing claims pulled back to 6.37mn (est. 6.40mn, prior 6.80mn). October existing home sales were strong – the annualised level jumped to 6.85mn (markets expected a dip to 6.47mn given the sharp near 10% spike in Sept to 6.57mn). Gains were seen across all regions, with average prices rising 15.5% vs. Oct. last year to USD313k.

The Philadelphia Fed business survey fell less than expected to 26.3 (est. 23.0, prior 32.3) – still strong and higher than any reading in 2019. Although current activity and new orders pulled back, the employment component rose (to 27.1 from 12.7). The Kansas City Fed survey also fell, but as expected, to 11 from 13, with new orders (to 19 from 26) and export orders (to -10 from +1) softening, but the 6-month ahead expectations relatively solid at 20 (prior 21).

Fed officials also spoke of the economy losing momentum and needing fiscal support. Although markets expect further Fed easing, Mester stated that it is “not clear to me that monetary policy is the right tool” and that she would “not prejudge the December FOMC meeting”. Kaplan suggested that the maturity of QE could be lengthened, but he does not favour increasing the quantity. He said all the economic risks are to the downside, adding that the next couple of quarters will be challenging.

Eurozone current account surplus rose in October, in line with other regional trade data, to EUR25.5bn (prior revised to EUR20.9bn from EUR19.9bn).

EU/UK post-Brexit trade talks: the cancellation of in person EU briefings from EU chief trade negotiator was seen in early trading as a potential sign of an imminent deal. However, the announcement that one negotiator had contracted COVID was the real reason.

ECB’s Lagarde openly encouraged the EC to enact the Recovery Fund, she and other ECB members underscoring the fragility of the region’s economy which needs fiscal and monetary support, the latter again being stressed in terms of additional PEPP and TLTROs.

Event Outlook

Australia: Westpac is looking for a 0.5% decline in October retail sales. Supportive factors include the dramatic improvement in Consumer Sentiment and Victoria’s ability to get the outbreak under control. However, the Westpac Card Tracker suggests that sales were down in the month. There is considerable uncertainty around the number, with risks on both sides. Following this, the 2019/20 annual accounts will provide an update on output by state. To round out the domestic data, the ABS will release the “Business Impacts of COVID-19 Survey” for November.

Japan: The October CPI is poised to slip to -0.4%; the 2% target continues to move further out of range. The November Nikkei manufacturing PMI (prior 48.7) and services PMI (prior 47.7) have recovered from their troughs, but an inability to print above 50 indicates that both sectors remain in contraction.

Euro Area: November consumer confidence will be seriously tested by the renewed lockdowns (market f/c: -18.0).

UK: Fresh lockdowns will serve as a serious headwind to November GfK consumer sentiment (market f/c: -34) and October retail sales (market f/c 0.0%). Meanwhile, October public sector borrowing will reflect the ongoing efforts to support the economy (market f/c GBP31.5b).

US: The FOMC’s Kaplan (00:30 AEDT), Barkin and Bostic (01:00 AEDT), and George (05:30 AEDT) will speak.

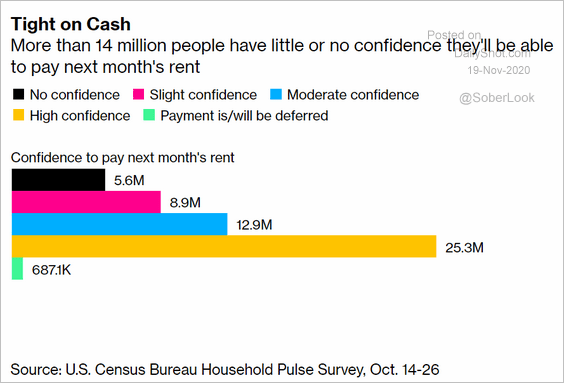

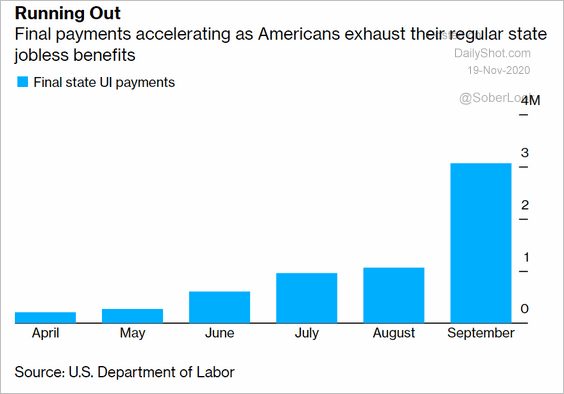

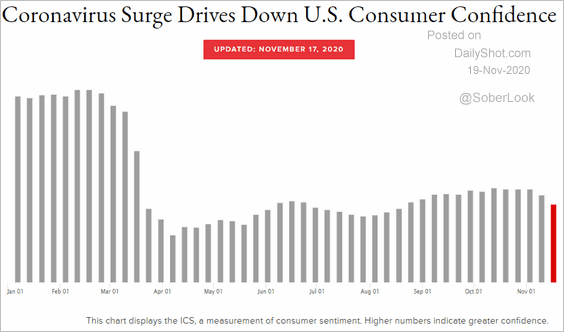

The US economy continues to slowly weaken under virus threat:

But the lockdown is in slow motion so the virus can keep spreading:

Difficult to know when numbers will peak. Probably before Joe Biden assumes office. The death rate follows hospitalisations and lockdowns follow deaths so we’ll be seeing mid-year scale restrictions by Xmas:

After that comes this:

The next few months will be terrible, politically and economically, and a lot of people will be impoverished and die unnecessarily. But vaccination is coming — and when it does, I suspect we’ll recover much faster than people expect 1/

— Paul Krugman (@paulkrugman) November 18, 2020

I’m inclined to agree. Especially in the US where it will be sink or swim for individuals taking the vaccine meaning borders to everywhere reopen.