The full report of the review commissioned by the federal government into retirement income will be released on 20 November, but its key findings have been made known.

Importantly, the report suggests that lifting the compulsory superannuation rate to 12% could disadvantage low-income earners and reduce workers’ lifetime incomes:

“A rate of compulsory superannuation that would result in people having an increase in their living standards in retirement may involve an unacceptable reduction in living standards prior to retirement, particularly for lower-income earners,” an extract of the report, provided by the government, says. “This is based on the view, supported by the weight of evidence, that increases in the super guarantee rate result in low wages growth, and would affect living standards in working life.

“The weight of evidence suggests the majority of increases in the super guarantee come at the expense of growth in take-home wages. The view is based on empirical research, economic theory, evidence across a number of countries and the original policy intent of superannuation guarantees.

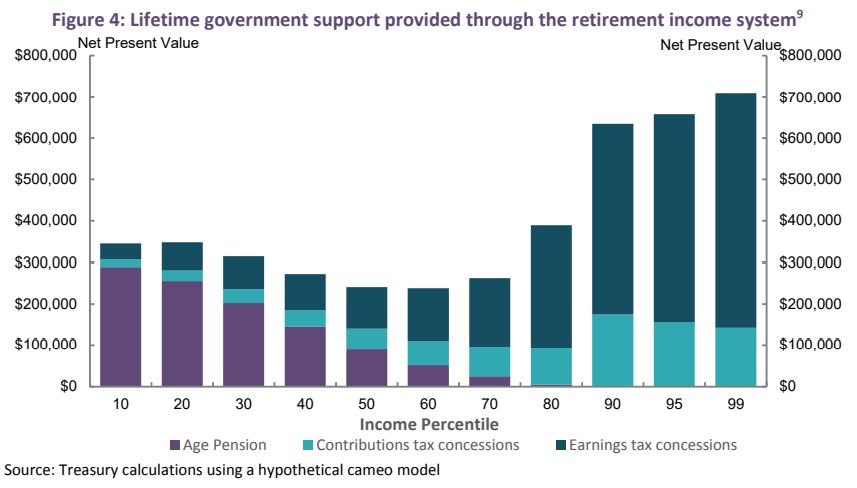

Australia’s compulsory superannuation system already exacerbates inequality by handing the lion’s share of tax concessions to high income earners:

According to the retirement income review, inequality will worsen if the superannuation guarantee is lifted to 12%:

“Increases in the superannuation guarantee rate will increase lifetime government support for higher-income earners by more than lower- and middle-income earners.”

Thus, retirement income review has arrived at similar conclusions to MB, which has opposed lifting the superannuation guarantee to 12% because:

- It would suppress future wage growth and disposable income, adversely impacting lower-income earners already struggling to make ends meet.

- It would increase inequality, since higher income earners receive the bulk of super concessions.

- It would worsen the long-term sustainability of the federal budget, given the cost of superannuation concessions outweighs the benefits from lower pension outlays.

Ultimately, the main beneficiary from lifting the superannuation guarantee to 12% would be super funds themselves, because it would provide them with more funds under management and enable them to earn fatter fees to the detriment of taxpayers and workers.

Lifting the superannuation guarantee to 12% was always bad policy and should be dumped.