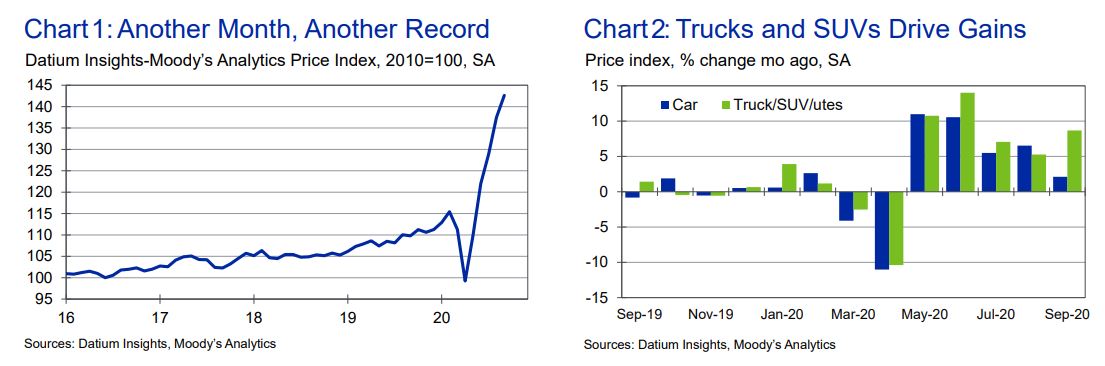

Prices of wholesale used vehicles rose for the fifth consecutive month in September, according to the Datium Insights-Moody’s Analytics Price Index. Prices rose 3.8% compared with August and are now a staggering 29.9% higher than they were at the same point in 2019 (see Chart 1). All else being equal, now is the best

time to be selling a used car, truck, SUV or ute on record.

The continued price gains in September were a bit less than they have been in previous months. The month-over-month change was the slowest increase since the improbable take-off in prices began in May.

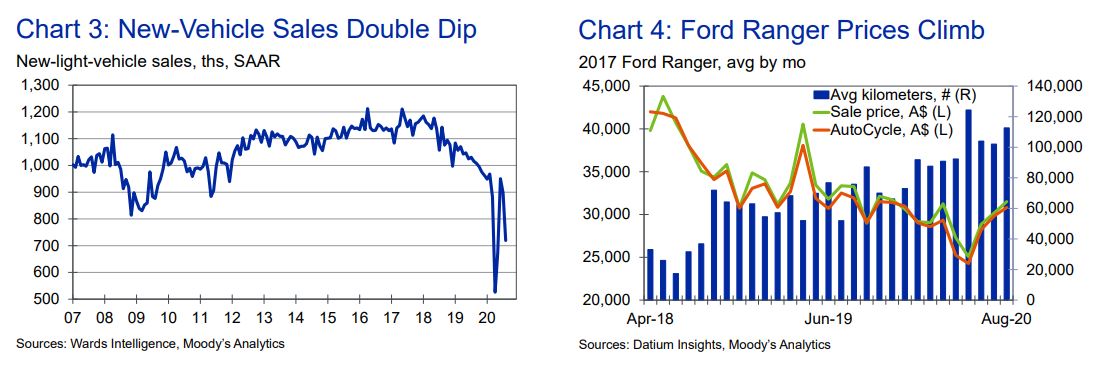

The somewhat slower growth was held back by passenger cars, which grew by 2.1% compared with August prices, while larger-vehicle segments increased by 8.7% (see Chart 2).

The split in price movement between cars and trucks/SUVs is a divergence from what had previously been a tandem movement of the two market segments since the start of the recession. Preference for larger vehicles has been gaining rapidly over the past six years. During this period, sales of passenger cars have fallen to less than 30% of total new-vehicle sales. These preferences have not changed because of the pandemic and recession. Conversely, current circumstances have likely accelerated the change; petrol prices have been consistently low since February and are down 20% from a year earlier.

The increased demand for trucks and SUVs has been difficult to satisfy in the current environment. Production of new vehicles was halted worldwide at the beginning of the outbreak, leading to shortages of popular vehicles in lots across the world. Plants were restarted and the supply constraints for new vehicles eased, but the number of used vehicles continues to be limited.

Limited supply of used vehicles is caused by the reduction in new vehicles sold. Most new-auto purchases come with the trade-in of another vehicle, a used car. However, new-vehicle sales have dropped more than 20% from an already-underwhelming 2019 rate (see Chart 3). New-vehicle sales tumbled to the third lowest monthly rate on record in August, outdone by only April and May of this year.

The limited sales and thus limited used-vehicle supply continue to support the price increases in the wholesale used-vehicle market.

The changes in the supply and demand of the used-vehicle market can be seen when looking at the sales and forecasts for individual vehicles. Looking at average transaction data along with the Moody’s Analytics AutoCycle forecasts, the average price of a Ford Ranger has risen despite the average kilometers on the vehicle staying consistent. The price rise begins in May and continues through the last observations in August (see Chart 4). The only other period there was a significant rise in the average sales price was in April 2019, but this was caused by the mix of vehicles being skewed towards Rangers with fewer kilometers driven.

Our forecast remains for growth to slow and finally subside as markets readjust towards the end of the calendar year. At this point, the unprecedented and unexpected ride that used-vehicle prices have taken over the past five months will come to an end. Still, the price gains that have been realized are not expected to be given back quickly. Prices of goods, like wages, tend to be somewhat sticky. This means that once dealers know what they can get for a vehicle they are not likely to drop prices back down without a major shift in market fundamentals. For this reason, the current level of pricing for used vehicles is expected to be the new normal.

Trucks and SUVs drive gains. But, but, but the accelerated depreciation tax credit…

Prepare for a major disappointment as business sweats existing assets amid massive oversupply.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.