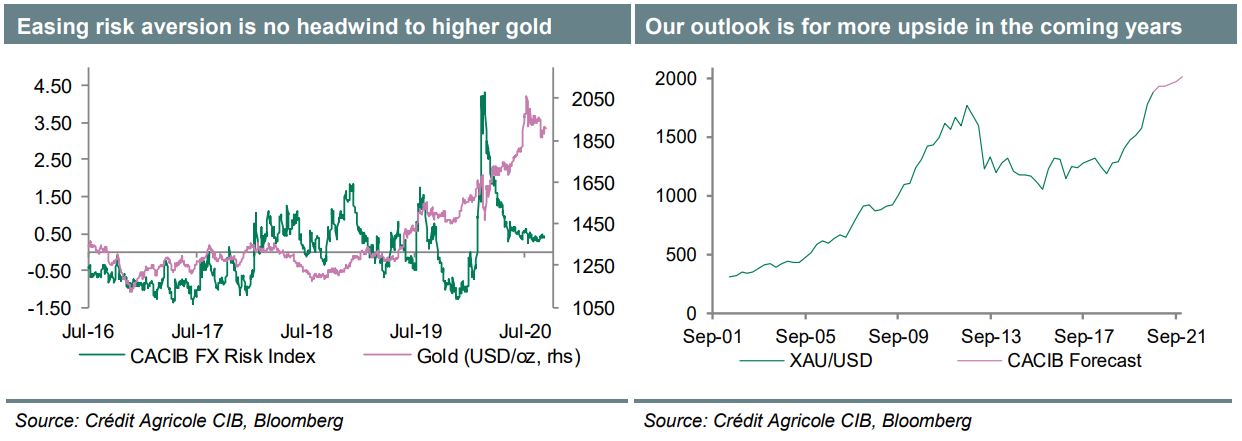

After correcting lower towards the end of September, precious metals such as gold have been stabilising with our outlook being for gradual upside in the coming few quarters. While we expect gold to end the year closer to 1940 (USD/oz), the yellow metal should advance well above 2000 in the years to come.

Given that the yellow metal is likely to remain predominantly driven by the interest rate environment and when considering most major central banks are prepared to let inflation overshoot before considering any material adjustment to monetary policy, then one should expect the backdrop for hard assets to remain favourable in the coming few years. Politically driven price action is unlikely to prove sustainable.

Rebounding global growth momentum in the coming years to the benefit of risk appetite is unlikely to prove detrimental to gold as a safe haven, especially as central banks’ more muted reaction function to such a development should prevent monetary conditions from tightening. This implies that gold’s sensitivity to periods characterised by improving risk sentiment should stay low.

On the flipside, should growth momentum deteriorate more meaningfully, major central banks such as the Fed have made it clear that they are prepared to do more if needed. This in turn should increase gold’s attractive as a risk-off hedge.

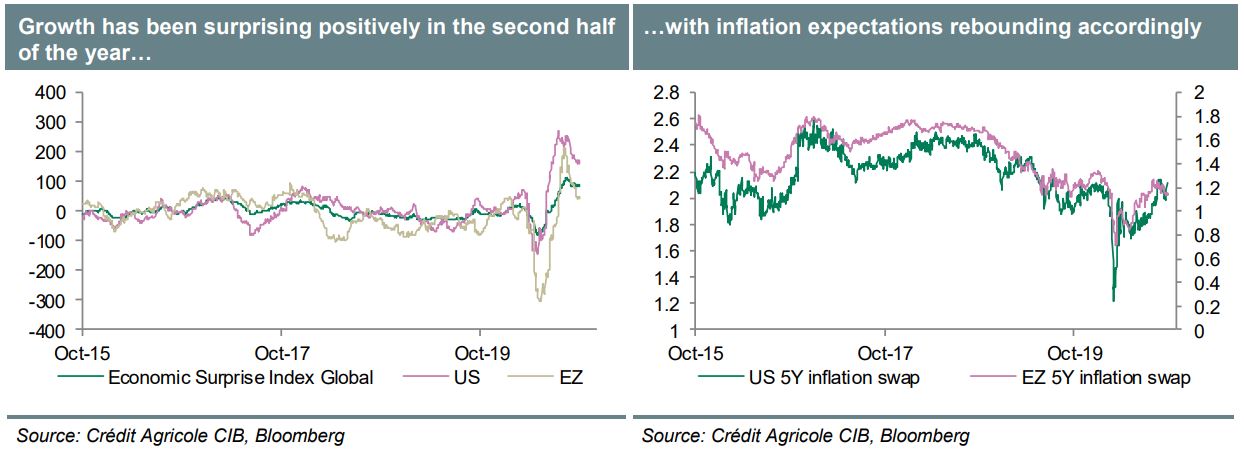

In the long run, rebounding global growth momentum is expected to help inflation rebound more evenly, as for instance implied by forward breakeven rates. Further improvement in that respect, although distant in the future, should help increase gold’s attractiveness as an inflation hedge.

Overall, we believe risk reward should stay firmly in favour of hard assets. With speculative long positioning having normalised not far from its longer-term average, this suggests that short-term downside risks should be low from here, irrespective of whether or not gold trades far from its yearly highs.

Gold was under pressure during September, mostly on the back of the stronger USD. This was in line with our base case, according to which we expected gold to end the month closer to 1860 (USD/oz). From here, we believe that dips should prove a buy with our long-term outlook remaining one of gradual upside.

While investors’ near-term focus will be on the US presidential election, any political uncertainty induced price action is unlikely to prove sustainable.

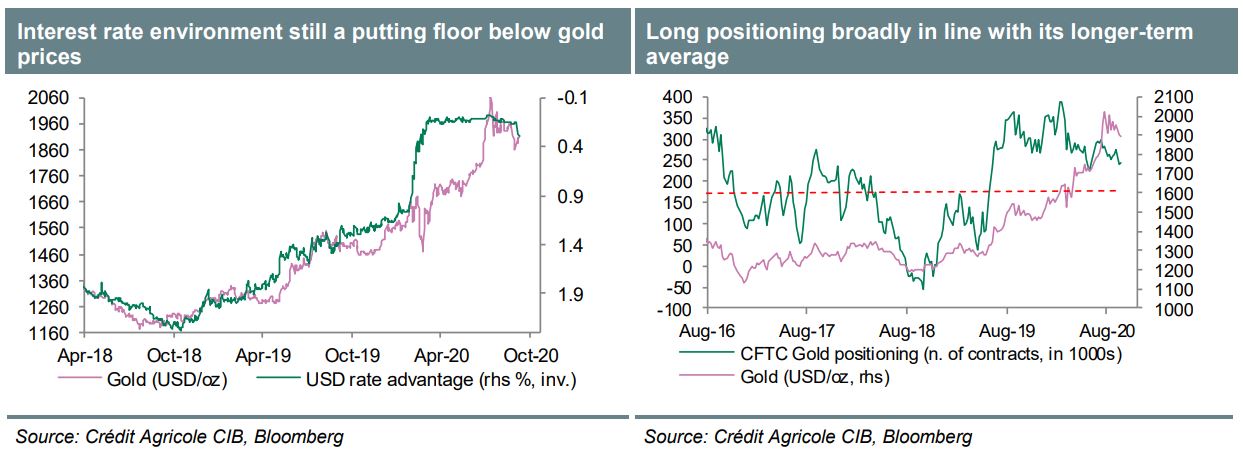

After all, it should remain about the interest rate environment to continue putting a floor below hard assets such as gold with the Fed’s new average inflation targeting framework likely to help keep the USD rate advantage firmly capped.

This should continue to put a floor below hard assets, especially as more balanced speculative long positioning argues against rising short-term downside risks from current levels.

All of the above should prove beneficial from a long-term perspective too, especially as soon as more evenly rebounding growth momentum starts to lift price growth in developed markets. With major central banks’ reaction function to such a course of action likely to prove slow, precious metals should continue to benefit from easier monetary conditions.

Most importantly, such conditions should also keep gold’s sensitivity low to periods characterised by improving risk appetite. This makes sense, when considering that it may become more attractive as an inflation hedge, although such an assessment should be treated as long term in nature.

Overall, we believe risk reward should continue to favour buying dips in gold.

While our year-end target stands at 1940 (USD/oz) we account for upside risks and more considerable upside well above 2000 in the years to come. Although long-term positioning appears elevated, it is firmly in line with its longer-term average. This speaks against heightened position squaring-related downside risks.

Solid analysis. My own view is there is another dip ahead before we move higher.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.