The new and improved bullish Bill Evans returns this morning:

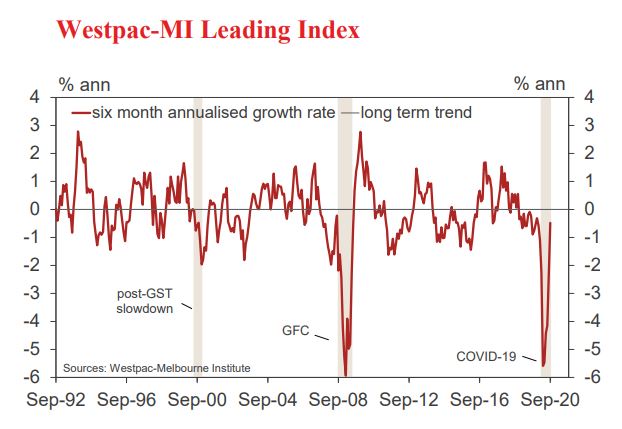

• The six-month annualised growth rate in the WestpacMelbourne Institute Leading Index, which indicates the likely pace of economic activity relative to trend three to nine months into the future, rose from –2.28% in August to –0.48% in September.

Momentum continues to show a significant improvement consistent with the Australian economy moving out of recession.

Westpac expects that growth in both the September and December quarters will be clearly in positive territory, as the Australian economy opens up. We have also revised up our growth forecasts for 2021 and 2022 following the announcement of the Federal Budget. Consistent with the steady progression in the leading Index we expect growth of 2.8% in 2021 and 3.5% in 2022. Key factors behind this stronger profile are a boost to consumer demand, as households spend around 50% of the personal tax cuts, and a lift in business investment in response to the accelerated depreciation allowances.

We are disturbed by the government’s forecasts that population growth will fall to 0.2% in 2020/21 and 0.4% in 2021/22, reflecting negative net migration in both years.

In time, perhaps a more progressive approach to dealing with foreign borders will allow a faster return to normal net migration flows.

While the index growth rate remains negative, it is now well above the lows seen in the first half of the year when the COVID shock saw it drop well below –5%. Indeed, at –0.48%, the latest reading is in line with the average recorded over the twelve months prior to the pandemic.

The Leading Index growth rate has lifted a whopping 5.11ppts since April. The main components driving the improvement have been: US industrial production (+2.82ppts); the S&P/ASX 200 (+1.01ppts); aggregate monthly hours worked (+0.75ppts); the WestpacMI Consumer Expectations index (+0.73ppts); and the Westpac-MI “Unemployment Expectations index (+0.66ppts). Notably, these gains have been partially offset by a bigger drag from commodity prices (–0.47ppts), which is measured in AUD terms – the rising currency more than offsetting a modest gain in USD prices over the last six months. There has also been a bigger drag from the dwelling approvals component where weakness through the middle of the year has seen it detract 0.35ppts from the index growth rate since April.

Note that the big negative shock that accompanied the COVID outbreak back in March–April will start cycling out of the six-month growth rate calculation in coming months.

All else being equal, the growth rate will swing into solid positive as the extreme weakness in March–April moves into the base of the calculation.

The Reserve Bank Board next meets on November 3. The Minutes of the October Board meeting, released on October 20, made it quite clear that the Board is preparing to further loosen policy settings.

We continue to expect key policy rates – the cash rate; the three year bond target rate; and the rate on the Term Funding Facility – to be reduced from 0.25% to 0.10% at the upcoming meeting on November 3.

In addition we expect the Board to announce a reduction in the rate paid on surplus funds in Exchange Settlement Accounts to 0.01% along with an open ended commitment to purchase both Australian government and semi government bonds out along the maturity spectrum to 10 years.

Is that right, Bill? Still looks like the index is projecting negative growth to me and that’s before we discount the two inputs from your recent wild outlier result from consumer sentiment.

We might see growth flop into the positive in the Sep QTR as NSW reopening outweighs VIC closing.

Advertisement

We will see a weak bounce in the Dec Qtr.

As for Mar and June 2021, both are going to be demolished by the Depressionberg Unstimulus and we may well be back into recession.

That’s what the old Bill would have concluded. Bring him back.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.