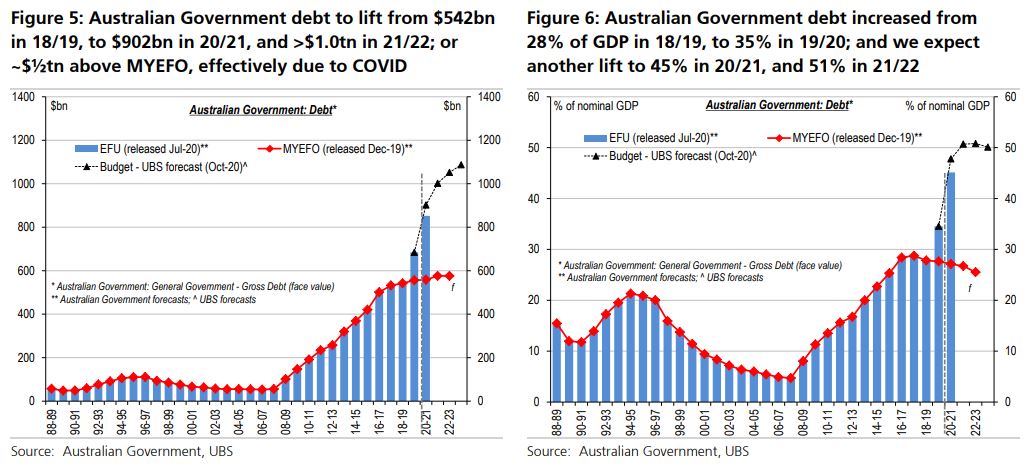

Record deficits likely: $235bn (12.0% of GDP) in 20/21; $100bn (4.9%) in 21/22

The Australian Government will release the 20/21 (Commonwealth) Budget on October 6 (delayed since May). Unsurprisingly due to COVID-19, we expect record budget deficits. After a balanced budget in 18/19 was the best since the GFC (with the General Government: Underlying Cash Balance at -$1bn), the Final Budget Outcome for 19/20 was -$85bn (or -4.3% of GDP), in line with July’s EFU. For 20/21, despite the ongoing upside surprise of commodity prices, with iron ore alone boosting the budget by $10bn+, we continue to expect a record deficit of $235bn (vs consensus ~-$225bn), significantly worse than EFU (-$185bn, with JobKeeper 3.0 alone costing $16bn); and materially worse than MYEFO (released in Dec-19 at +$5bn), which projected surpluses every year over the outlook. At 12.0% of GDP, the deficit is the largest since WW-II, and ~3x larger than the GFC. However, the vast majority of the Australian Government stimulus so far (of ~$193bn; or ~$244bn or >12% of GDP including the States) is temporary and ‘expires’ by mid-2021. Hence, even with a relatively weak economic recovery to be projected, we still expect a record narrowing of the deficit in 21/22 to -$100bn (or -4.9% of GDP; vs consensus at ~-$138bn; and compares to MYEFO’s +$8bn). Further ahead, we expect a projection of ongoing sharp consolidation in 22/23 to -$50bn (-2.3% of GDP, consensus: ~-$75bn), and in 23/24 to -$35bn (-1.5%).

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.