What to expect with the 2H20E bank results starting Thursday 29th October

The 2H20E reporting season (to September) will be unusual, with the banks operating in a false economy, given: almost half the labour force was on wage subsidies, unemployment benefits or employed by the government; mortgage & SME deferral; rental relief; and much of Victoria is still under lockdown. Therefore, it is extremely difficult for the banks to gauge the quality of their books or provisioning. Banks will again be forced to estimate expected credit losses in various scenarios, which is merely an educated guess on an Excel spreadsheet. Actual losses won’t emerge until FY21E. As a result, FY20 numbers and FY21E outlooks should be treated with caution.

Limited information in deferral run-off data. But RWA inflation may be lower

The banks are likely to provide an update on deferred loan books as holiday periods end. CBA data showed ~75% of mortgages in Victoria required deferral extension, as did ~35% of mortgages in the rest of Australia. CBA’s deferral extension was higher than we anticipated, while loans restructured to Interest Only were not disclosed.

Importantly, with substantial ECM activity, Institutional books appear in better condition than expected, while home prices have only moderated. As a result, RWA procyclicality may be less severe than guided. This may result in higher than anticipated CET1 in FY21/22E, opening the door for higher dividends and capital returns.

Stock-by-stock – what to expect

ANZ – Improving loan growth, lower Institutional credit losses, solid trading income, cost management offset by NIM pressure, NZ concerns. NAB – Bounce in trading to support revenue, NIM pressure, cost pressure, some credit provisioning catch-up. WBC – Statutory profit impacted by fines and writedowns (goodwill, life intangibles, IT) but likely to look through this for dividends, pressure on Pre-Prov Profit, lower provisioning charge in 4Q possible. CBA 1Q21 Update – CBA has a track record of a very strong 1Q updates. With economic overlay top-ups unlikely, earnings could rebound sharply.

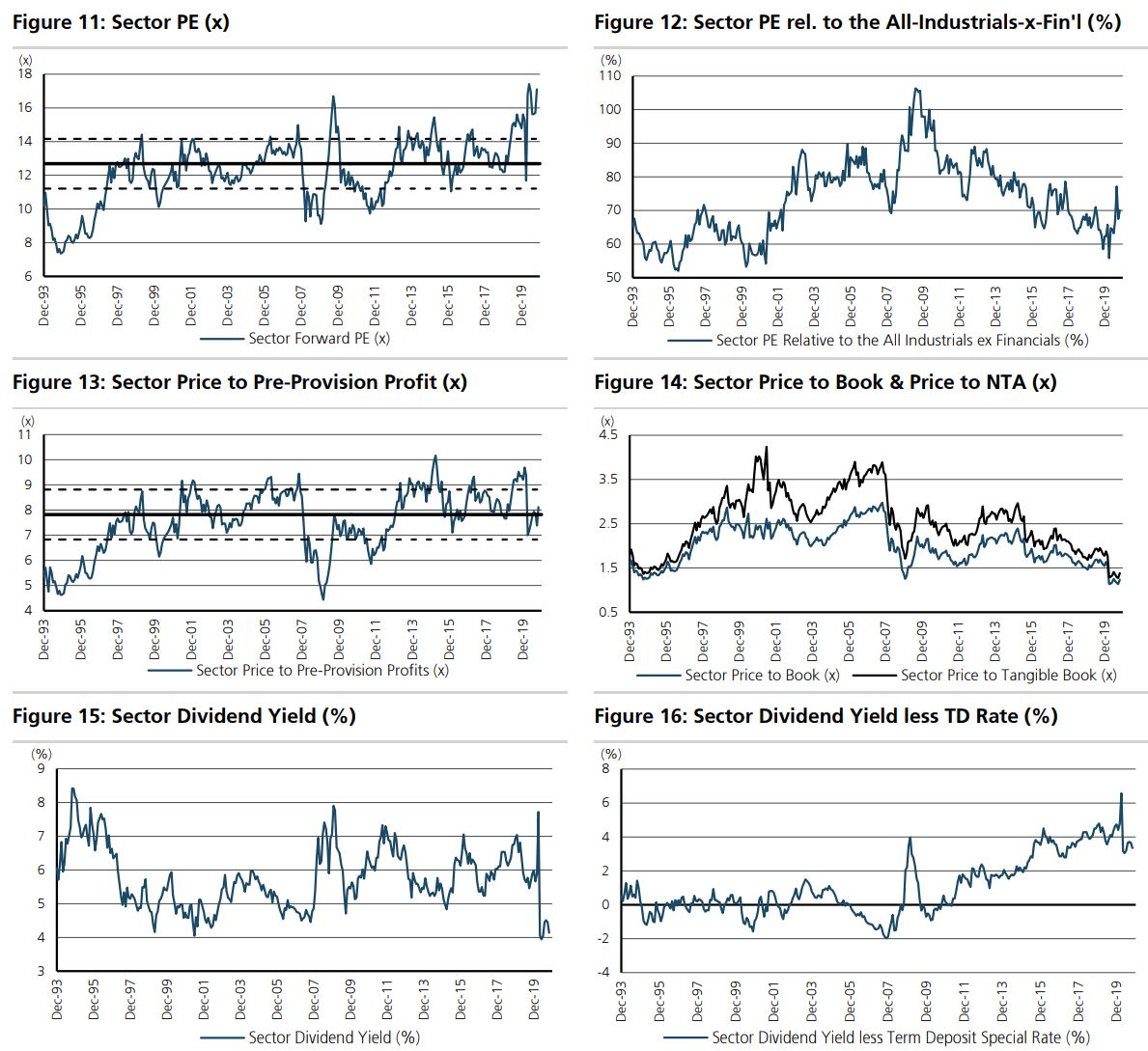

Remain positive the banks – Don’t miss the bounce. Pref: ANZ, WBC, NAB, CBA

The economy is starting to recover and the recession appears to have been less severe than was expected given the extent of policy support. As a result, we believe the market is likely to start looking through the weak earnings towards a potential profit recovery in late FY21E and FY22E. We expect the banks to rally through book value (ex CBA on 1.7x) and potentially higher as dividends begin to grow. However, this remains a function of a vaccine, speed of recovery, opening of borders and asset prices.

The banks are good value on a pre-provision profits basis. But, if you think, as I do, that the vaccine, speed of recovery, opening of borders and asset prices will all be major disappointments, and that the RBA’s exciting new journey into the unknowns of ZIRP will crush margins inexorably plus, perhaps most importantly of all, the return on insolvency, then they are the most expensive ever.

Another way to think about it is it depends upon your investment horizon.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.