Via super-bear, Albert Edwards of Societe General:

Equity market sector and factor performance has been driven by government bonds like never before. The Ice Age cyclical aversion theme has seeped deep into the equity market, facilitating, at its most extreme, massive FAANG outperformance. What now?

I was watching attentively last week as my colleagues Andrew Lapthorne and George Oikonomou presented at the flagship SG 2020 Derivatives Conference. They had just published a fascinating note entitled “Seriously… what’s wrong with Value?”, and so they were able to expand on the themes (I was so interested I actually took notes). SG has posted videos of the key presentations on our research website and so you too can see what they were saying link. It’s always good to see people speaking in the flesh even if it is virtual.

There is even a video of me giving the keynote address on Day 2 entitled, “The Ice Age is about to take its final bow. How deep will it be?” It’s a pretty jam-packed 20 minutes of ideas, but I wanted to fit a lot in. It is the first time I have made a video like this, for unlike some of my photogenic macro colleagues, I tend to be rather camera shy.

Maybe my lack of confidence behind the lens comes from the trauma of growing up with gigantic sticking out Bat-Ears (or otapostasis; like Prince Charles I too had them corrected in an operation). I still remember the day the 1960s children’s television puppet stars, Pinky and Perky, dropped in to visit us kids in the UK’s leading children’s hospital, Great Ormond Street. Upon seeing my head in a massive plaster cast the attendant press photographers mistakenly thought I must be the sickest child on the ward and so picked me out for the photo-op with Pinky and Perky, which ended up on the front page of a British tabloid national newspaper. That was back in 1968, but I still carry around that imposter syndrome today!

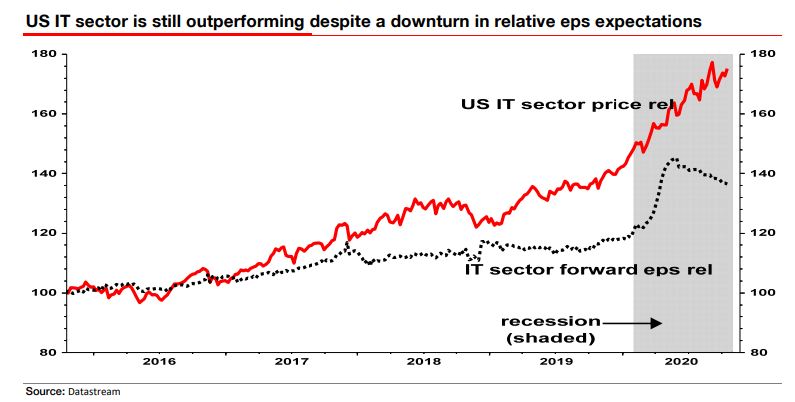

Talking about imposter syndrome, let’s pivot back to the US technology sector. Regular readers will know that, having long regarded this sector as dominated by cyclical stocks masquerading as ‘growth’ stocks, I expected their inflated valuations would be blown apart by the recession. How wrong I was but I already did my mea culpa at the end of May and I don’t intend to undergo a second ritual humiliation link. Mind you, as I confidently predicted that the FAANG stocks were a bubble of belief that would be deflating by the end of this year I need to revisit this topic.

In the Ice Age quality, growth and earnings certainty will be and should be, re-rated to extreme highs. But woe betide any stock (or sector, as in 2001) that profit-warns, making the market realise it has been fooled, having wrongly valued it as a growth stock. In 2001 it wasnt just the baby that was thrown out with the bathwater the whole bath followed the baby out the window.

The concentration and leadership of the overall US market by an increasingly few stocks could be seen as a burden as much as a boon. For Andrew Lapthorne notes that history demonstrates that periods of extreme outperformance by the 5 or 10 largest cap stocks are eventually counterbalanced by periods of huge underperformance. Is this time really so different?

Biggest 5 and 10 stocks relative performance to S&P 500 Comparing the yoy performance of the S&P 500 to the S&P 500 excluding the top 5 and top 10 largest stocks by market cap.

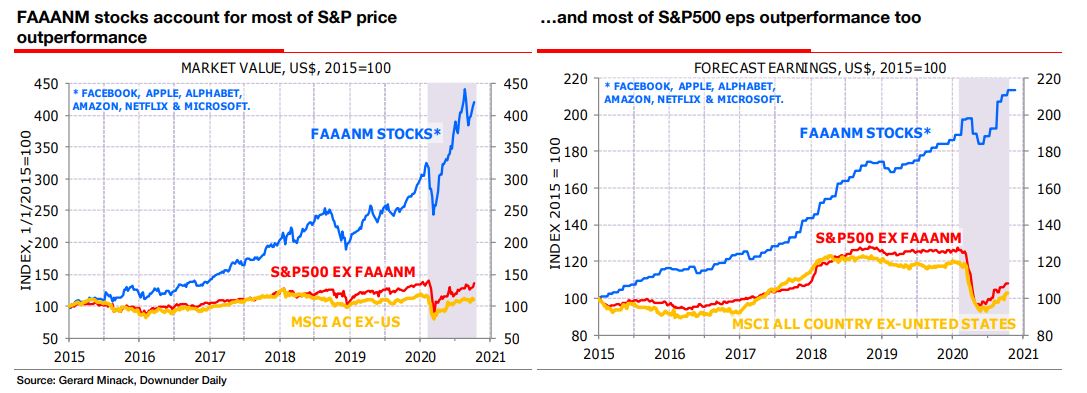

So let me finish with an update of some top-tastic charts I carried a few months back from Gerard Minack. Gerard adds Microsoft to the FAANGs (calling Google by its correct name, Alphabet) to form the FAAANMs (Facebook, Apple, Alphabet, Amazon, Netflix & Microsoft). Gerard notes the massive outperformance of the S&P versus the MSCI rest of the world (RoW) is almost entirely attributable to the FAAANM, top 6 stocks (see his charts below).

The S&P494 ex FAAANM, is almost as dull as the RoW. This is as significant as it is shocking. FAAANM stocks account for most of S&P price outperformance …and most of S&P500 eps outperformance too

The quite pedestrian price performance of the S&P494 (ie S&P500 removing the FAAANM stocks), in line with the RoW stock markets, entirely reflects their profit (and sales) performance.

It is shocking quite how reliant the US equity market has become on just six mega-cap stocks because it emphasises the risks if, for any reason the bubble in the FAAANM stocks burst, as I believe it surely will. Indeed, as Andrew showed earlier, history supports that view.

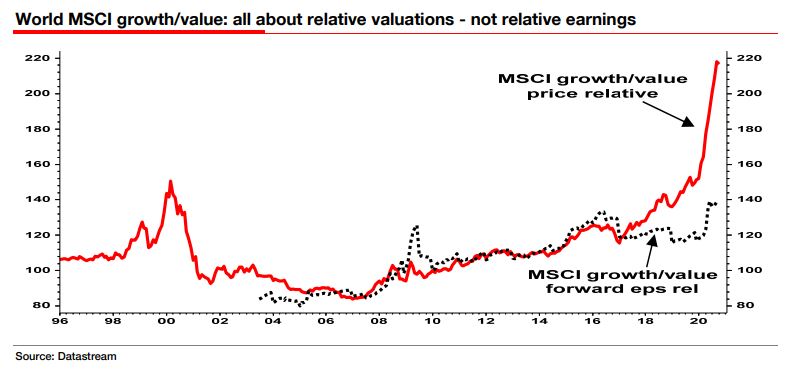

The Ice Age thesis supports K-style valuation polarisation within the equity market. Growth and quality stocks should be expensive relative to value and cyclicality. But if you have donned the Caesar-like valuation laurels that a growth stock wears and then reveal yourself as a cyclical imposter when you are sitting at these nosebleed valuations, expect a Brutus-like denouement.

I buy the basic premiss of the Ice Age so can’t see any lasting rotation into value, at least until we get a more established drive for MMT. That said, if we can get past the US election smoothly, get a new round of fiscal earlier than I fear, and contain the virus with minimal lockdowns, then I can see value snapping back next year as yields rise.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.