In his recent Lowy Institute commentary, RBA alumnus John Edwards demanded MOAR:

Just as the Australian government has little choice but to continue for some time with the expansionary fiscal stance it adopted in response to the pandemic, so too the RBA has little choice but to continue its expansionary monetary stance. In the RBA’s case, it has already and explicitly undertaken to do so.

Because of low rates maintained by the European Central Bank, the US Federal Reserve, and the Bank of Japan, the RBA must also maintain low rates unless it is prepared to accept a substantial appreciation of the Australian dollar.

This has become evident in recent months. The RBA has since March successfully maintained a 0.25 per cent ceiling on the three-year bond rate. In January, that rate was 0.75 per cent, or three times higher. The ten-year bond rate, however, has decreased much less than the three-year rate. Since March, the US ten-year Treasury bond rate has fallen below Australia’s. So too for the New Zealand and Canadian government ten-year bond rates. At the same time, and not unconnected, the Australian dollar has been appreciating against both the US dollar and the trade-weighted index, suggesting the offshore buyers find Australian bond interest rates comparatively attractive. Australia will likely be growing faster than the United States, Europe, and Japan over the next few years, as it has for most of the last two decades. It has recently moved into a persistent trade surplus with the rest of the world. Both trends will also support upward pressure on the Australian dollar. Mild now, the Australian dollar appreciation could gain speed and become a problem for Australia’s export returns if the bond rate spread between Australia and the US continues to widen. Given that the short-term rate controlled by the RBA is already at rock bottom, its only remaining tool to manage bond rates and the Australian dollar is the amount of Australian bonds it buys.

There are also good domestic reasons to sustain rock-bottom interest rates.

Like governments, households, too, currently have increased debt. To sustain consumption while incomes were falling, households ran down savings, and borrowed. Where households could not meet their mortgage commitments, the payments were deferred, but added to the debt. The banks announced that by late May, 700 000 households had requested relief on their mortgage payments. By early August payments on a total of $274 billion in household and small business loans had been deferred. At the same time, households were encouraged to draw down their retirement nest eggs to finance daily expenses.

Going into the crisis, household debt was already equal to 180 per cent of household disposable income, mainly due to Australians’ preference for owning their homes, and the high price of those homes. Coming out of the crisis, household debt is likely somewhat higher, while household financial assets are likely somewhat lower. Household incomes on average will also be lower, with the loss falling mostly on the newly unemployed or underemployed. After RBA rate cuts, household mortgage interest payments fell in March 2020 to less than one-fifteenth of household disposable income — the lowest share since the late twentieth century.[38] That share may rise a little given the likely rise in debt and fall in household disposable income since, though not by much. The sustainability of the budgets of many households depends on interest rates remaining at the lowest level they have ever been. Any small increase in the RBA policy rate would have a significant effect.

… businesses are now likely to come out of the crisis with somewhat higher debt but at somewhat lower cost than before the pandemicBusiness debt in Australia as a share of GDP moderated after the GFC. During the COVID-19 crisis, many strong businesses prudently drew on lines of credit or issued new debt to ensure they would have enough cash. Some weaker businesses were obliged to negotiate with their banks to postpone debt repayments. With the share market tumbling but long-term interest rates low for quality borrowers, there was an incentive to borrow rather than issue new shares at a price well under their long-term value. The result is that businesses are now likely to come out of the crisis with somewhat higher debt but at somewhat lower cost than before the pandemic.

Like households and the Australian government budget, corporations are now more sensitive to the decisions of the RBA. This imposes a constraint on raising interest rates, perhaps for quite a while.

What the government and the central bank have switched on, they will not easily be able to switch off. The Australian government needs to sustain demand through spending, while the RBA needs to assist by keeping rates low — and both need to maintain this stance for long enough to bring unemployment down substantially.

Yesterday he demanded MOAR again:

The most effective way for the RBA to assist the economy at this point is to buy more Australian government bonds at the long end, for example 10 years.

This will restrain the appreciation of the Australian dollar.

Cutting an already rock-bottom official cash rate will have no effect whatsoever.

Quite right. In the US it was called Operation Twist:

Operation Twist is the name given to a Federal Reserve monetary policy operation that involves the purchase and sale of bonds. The operation describes a form of monetary policy where the Fed buys and sells short-term and long-term bonds depending on their objective. However, unlike quantitative easing, Operation Twist does not expand the Fed’s balance sheet, making it a less aggressive form of easing.

The Fed rotated from short-term purchases to long to suppress mortgage rates, which in the US are mostly fixed-rate and attached to the 30 year yield.

Australian mortgage are priced off the cash rate, and increasingly the Term Funding Facility, so it won’t help in that respect. Also, the RBA will be more aggressive and add new purchases in its endeavour.

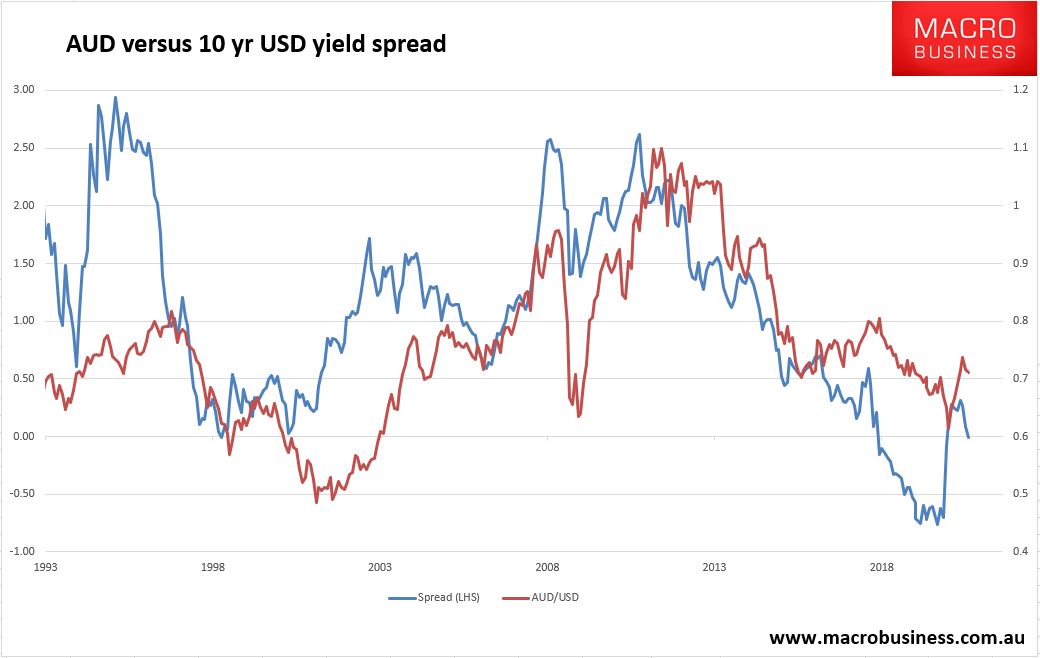

Edwards is right that this is all about the Australian dollar:

The more the spread is compressed and inverted the less the AUD will rise.

The timing of this is excellent given US yields are rising on the “blue wave” election and the US dollar falling. I doubt that that can be sustained as the virus runs riot but later next year with vaccines in play a more serious yield spike is possible and with the RBA hammering our long end the spread will deepen into the negative.

That will render the Australian dollar outright weak as iron ore adjusts.