According to Roy Morgan Research, Australia’s mortgage stress is running near record lows due to around 400,000 mortgage holders on repayment holidays:

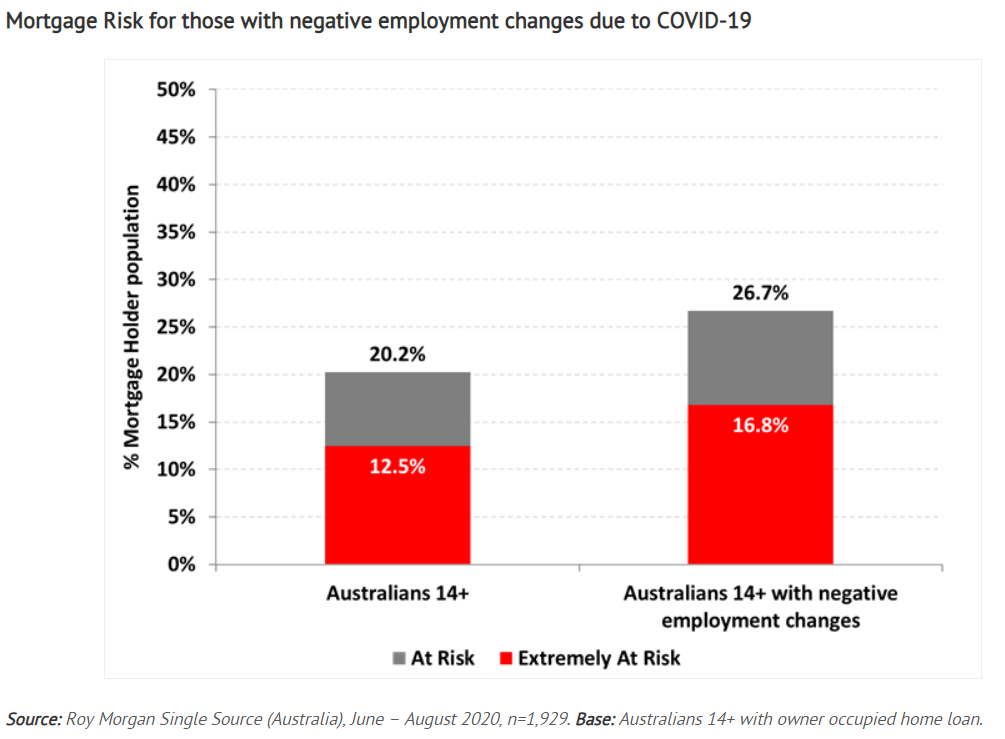

New research from Roy Morgan shows an estimated 751,000 mortgage holders (20.2%) were at risk of ‘mortgage stress’ in the three months to August 2020 as Australia navigated its way through the COVID – 19 pandemic. was living in a ‘COVID-normal’ situation although Victoria entered a Stage 4 lockdown.

This is near the record lows of a year ago when only 723,000 mortgage holders were considered ‘At Risk’ in the three months to October 2019. However, the significant support provided to the economy by the Federal Government as well as measures taken by banks and financial institutions to support borrowers over the last six months is not going to last forever.

Importantly, Roy Morgan has tracked the impact of COVID-19 on the employment situations of Australians. In May 2020, 11.2 million working Australians (72%) reported a change to their employment circumstances because of COVID-19, and in July 2020 there were still 10.4 million reporting their employment situation had changed – see more detail here.

Many of these employment changes are negative and include having ‘work hours reduced’, ‘not having any work offered’, ‘have been stood down for a period of time’, ‘business has slowed or stopped completely’, ‘had pay reduced for the same number of work hours’ or being ‘made redundant’.

For Australians with negative employment changes due to COVID-19 mortgage stress is significantly higher with over a quarter, 26.7%, now in ‘mortgage stress’ – over 6% points higher than for all mortgage holders. In addition, over one-in-six, 16.8%, are ‘extremely at risk’.

How are mortgage holders considered ‘At Risk’ or ‘Extremely At Risk’ determined?

Roy Morgan considers the risk of ‘mortgage stress’ among Mortgage holders in two ways:

Mortgage holders are considered ‘At Risk’1 if their mortgage repayments are greater than a certain percentage of household income – depending on income and spending.

Mortgage holders are considered ‘Extremely at Risk’2 if even the ‘interest only’ is over a certain proportion of household income.

Over 1-in-5 mortgage holders were ‘At Risk’ in August, near the record lows of late 2019

In the three months to August 2020, 20.2% of mortgage holders were ‘At Risk’ (751,000) which is near the record low of 723,000 reported a year ago in the three months to October 2019.

Of those ‘At Risk’ more than half, 433,000 or 12.5% of all mortgage holders, were considered ‘Extremely at Risk’ – also near the record low of 425,000 reported a year ago in the three months to October 2019.

The low level of mortgage holders ‘At Risk’ and ‘Extremely At Risk’ of mortgage stress during this period is due to the substantial support provided to the Australian economy by the Federal Government as well as the significant financial support provided by banks and financial institutions.

These are the latest findings from Roy Morgan’s Single Source Survey, based on in-depth interviews conducted with 50,000 Australians each year including over 10,000 owner-occupied mortgage-holders.

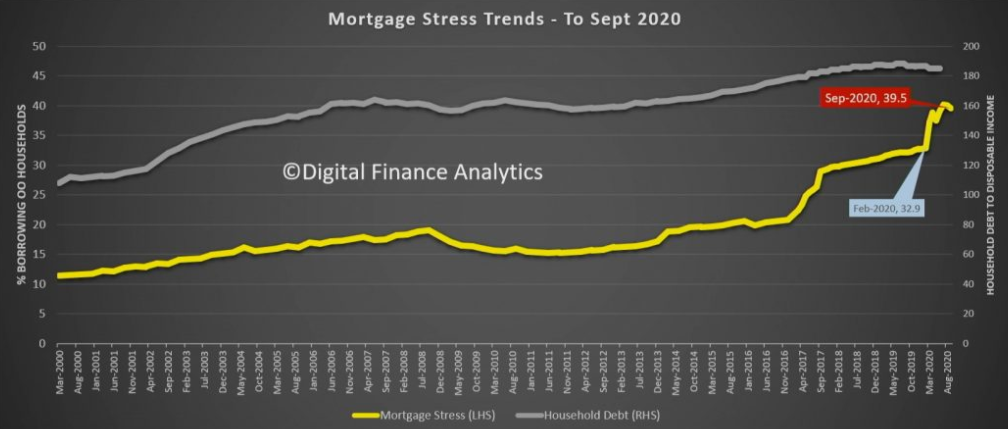

This data contradicts that of Martin North from Digital Finance Analytics, which reports mortgage stress near record highs:

Overall mortgage stress eased back to below 40% of borrowing households at 39.5%. But it remains very high. This is measured in net cashflow terms…

Across our household segments, young growing families (which include first time buyers) are most exposed, together with households on new estates on the edges of our towns and cities.

Advertisement

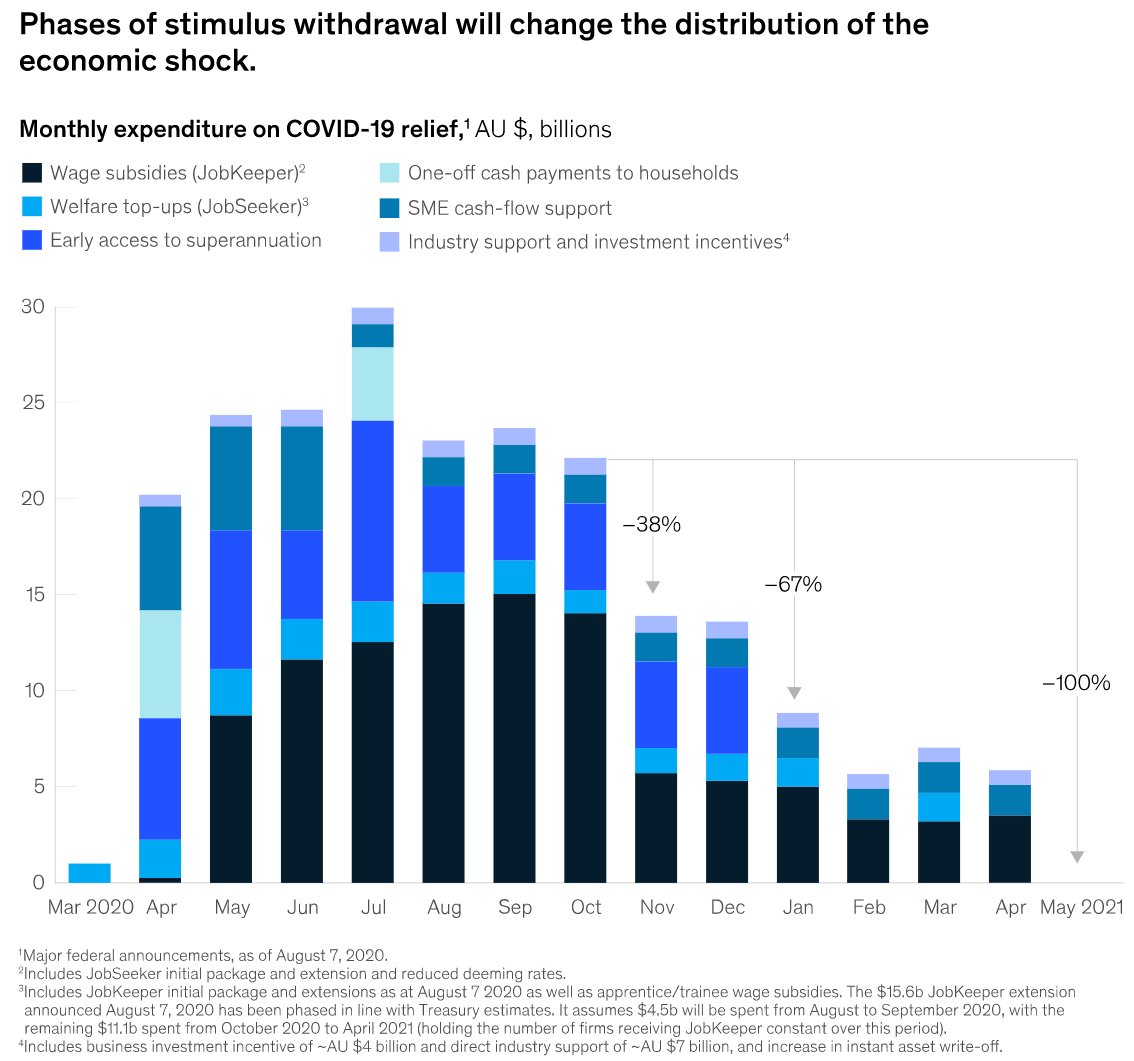

Irrespective, mortgage stress will inevitably rise once mortgage repayment holidays affecting around 400,000 borrowers come to an end, alongside the unwinding of emergency income supports:

Around $10 billion per month of emergency income support is scheduled to expire over the next half. Thus, this will drain households of disposable income, increasing stress levels.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.