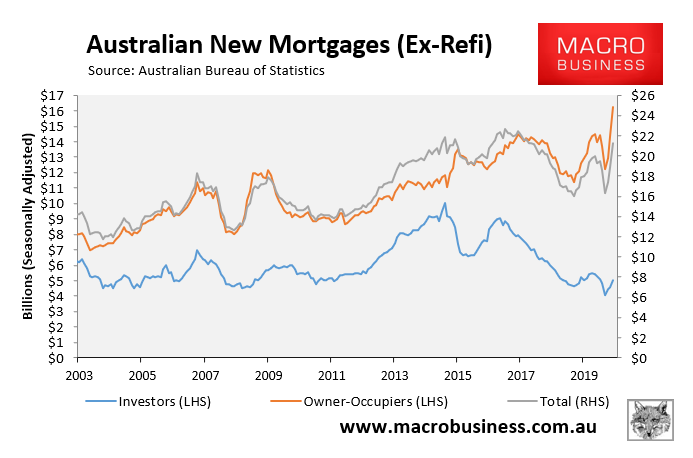

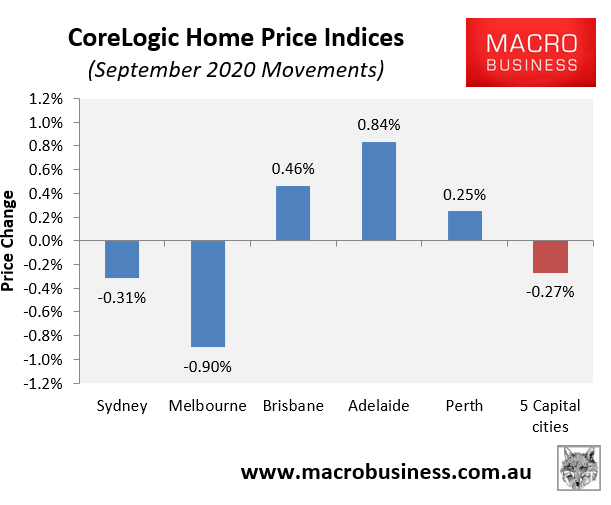

Friday’s housing finance data from the Australian Bureau of Statistics (ABS) points to a rebound in Australian property price growth.

This data showed a dramatic 12.6% lift in mortgage finance commitments (excluding refinancings) in August, with owner-occupied mortgages surging 13.6% and investor mortgages rising 9.3%:

As regular readers know, mortgage growth is one of the best indicators for property price growth having displayed a very strong historical correlation.

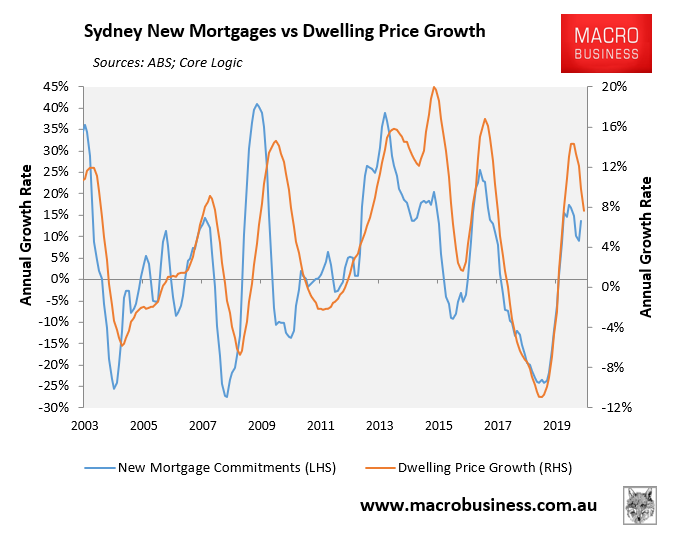

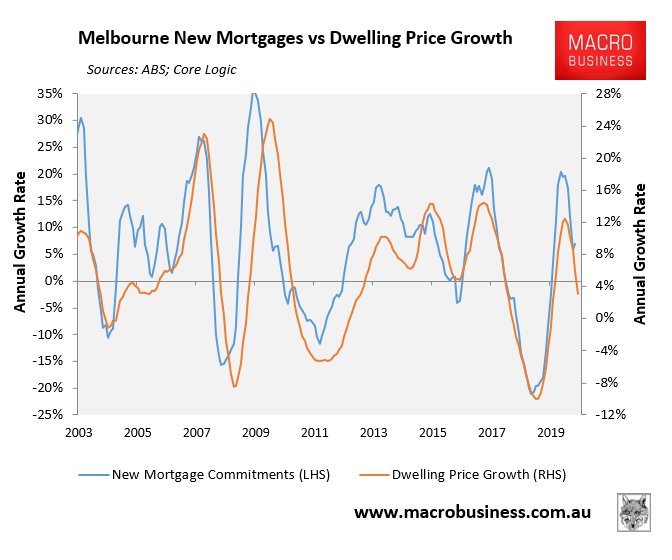

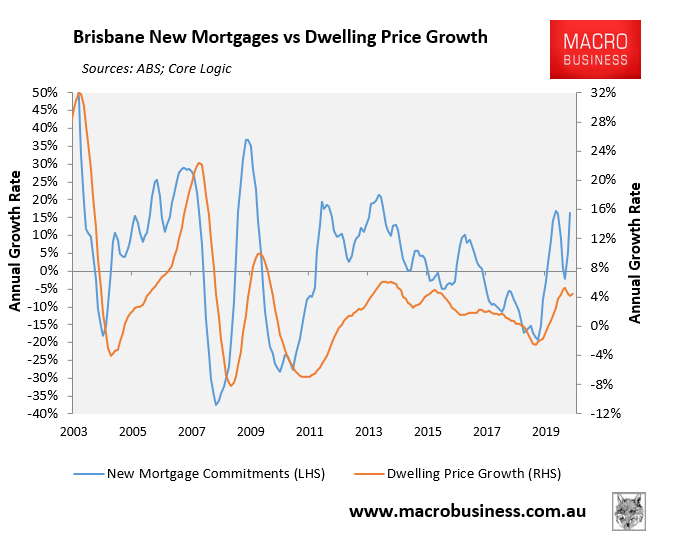

Below are charts plotting the annual value of mortgage growth (excluding refinancings) against annual dwelling value growth.

First, here’s Sydney:

Next Melbourne:

Next Brisbane:

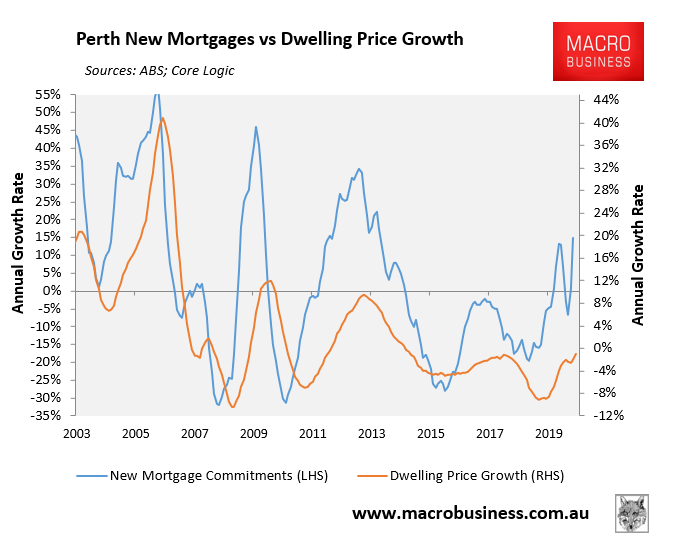

Next Perth:

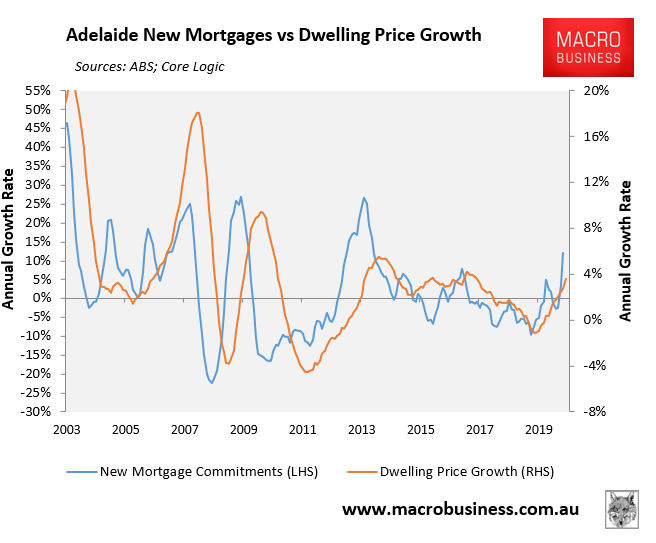

Next Adelaide:

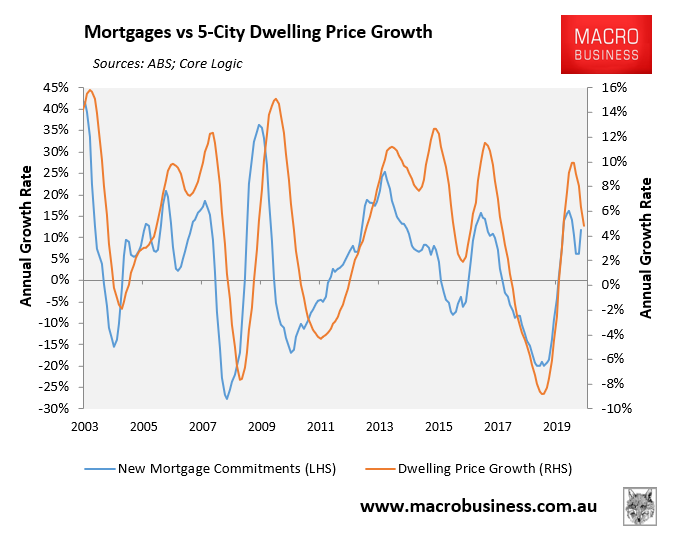

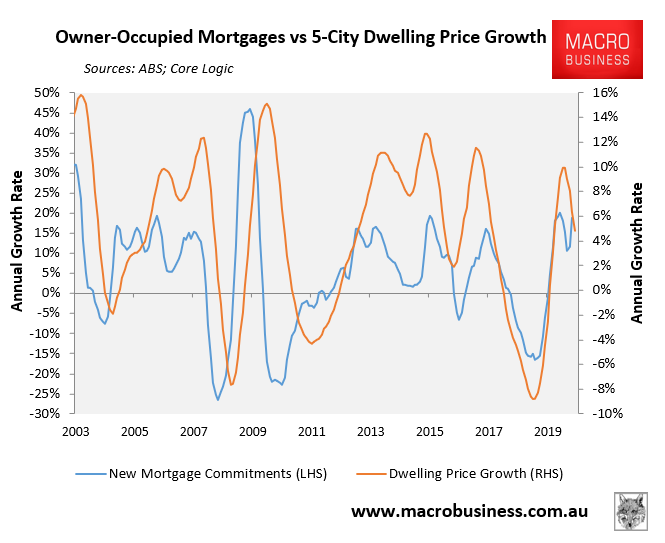

Finally, below is the 5-City aggregate:

As shown above, the mortgage rebounds have been strongest across the smaller three capitals, which is also reflected in their recent price rebound:

Sydney’s mortgage market has also experienced a moderate rebound, pointing to price stabilisation, whereas Melbourne’s remains week, suggesting further falls.

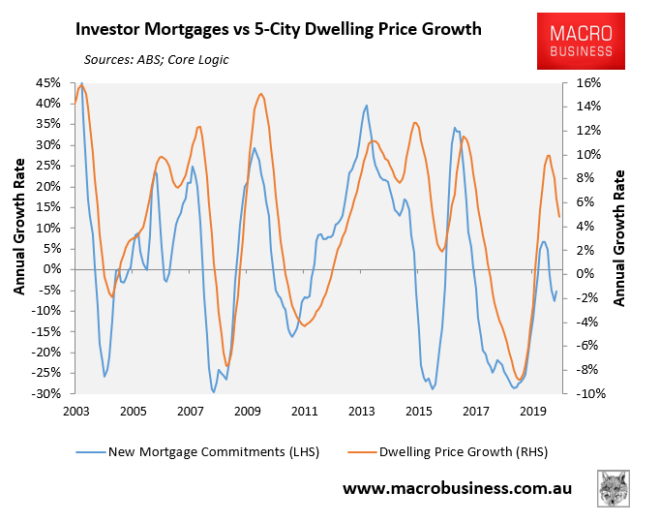

Another interesting feature is the extent by which the current rebound is being driven by owner-occupiers rather than investors:

We expect mortgage demand to increase as the Reserve Bank of Australia monetises the mortgage market via the Term Funding Facility (TFF) and the Morrison Government abolishes responsible lending laws.

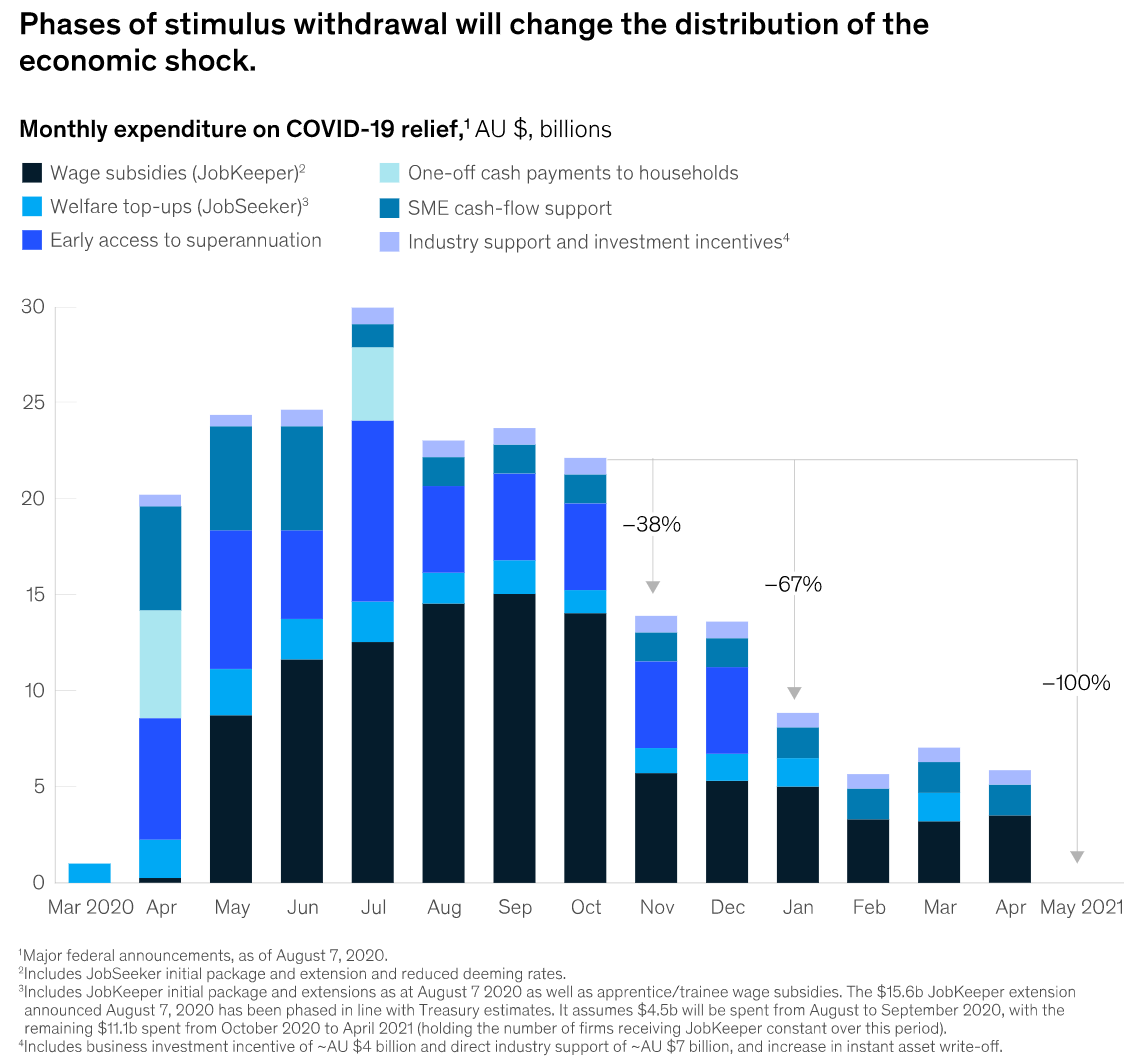

On the other hand, the collapse in immigration and the unwind of emergency income support (see next chart) will weigh heavily on prices in 2021.

It’s going to be a ‘tug-of-war’.