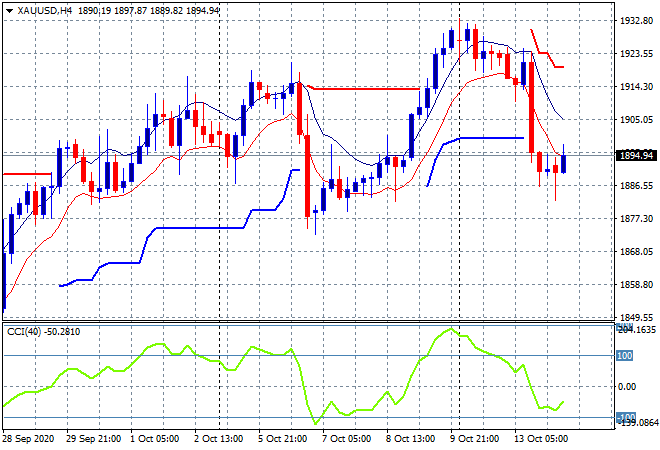

Risk is sliding back here in Asia, in line with the reversal on Wall Street overnight, with Chinese shares falling back the sharpest. The USD continues to firm against the majors and gold, which remains below the $1900USD per ounce level after its sharp fall overnight:

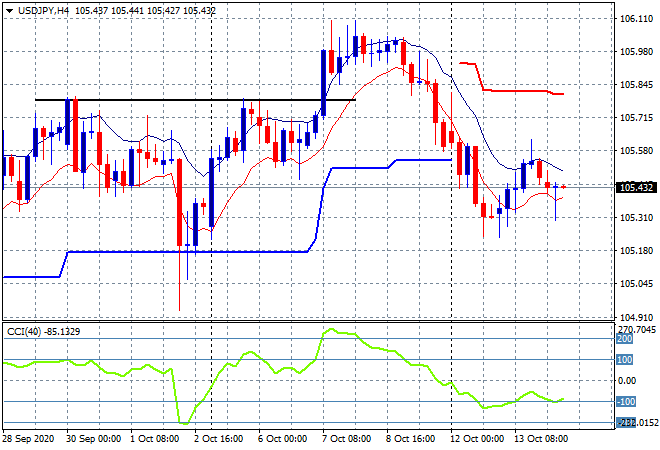

The Shanghai Composite is falling sharply going into the close, down 0.7% to 3335 points while in Hong Kong the Hang Seng Index had returned from its holiday to decline 0.3% to 24573 points. Japanese stock markets are mixed, with Nikkei 225 putting in a scratch session while the TOPIX fell back over 0.3% as Yen buying kept the USDJPY pair stalled just above the previous weekly lows at the 105.30 level:

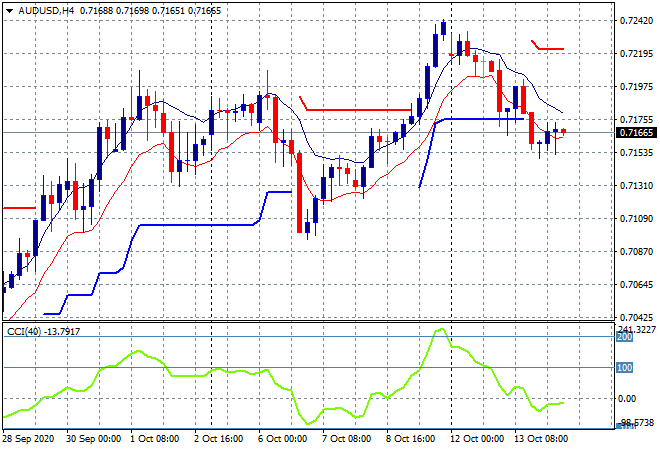

The ASX200 followed suit with other Asian markets, eventually closing 0.3% lower at 6179 points, unable to extend on its start of week gains as it fails to breach the previous June highs. The Australian dollar is treading water despite the consumer confidence report and remains below the 72 handle but unchanged from last night:

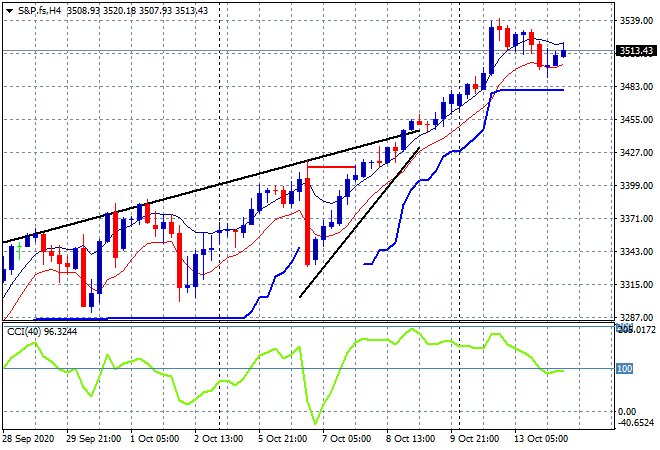

Eurostoxx and S%P futures are rising slightly into the European open with the S&P500 four hourly chart still looking to consolidate here after being overextended as it hovers above the 3500 point level:

The economic calendar includes a few more ECB speeches, the last US PPI print and the API crude oil stock count.