Should I have ever doubted that propaganda works just fine:

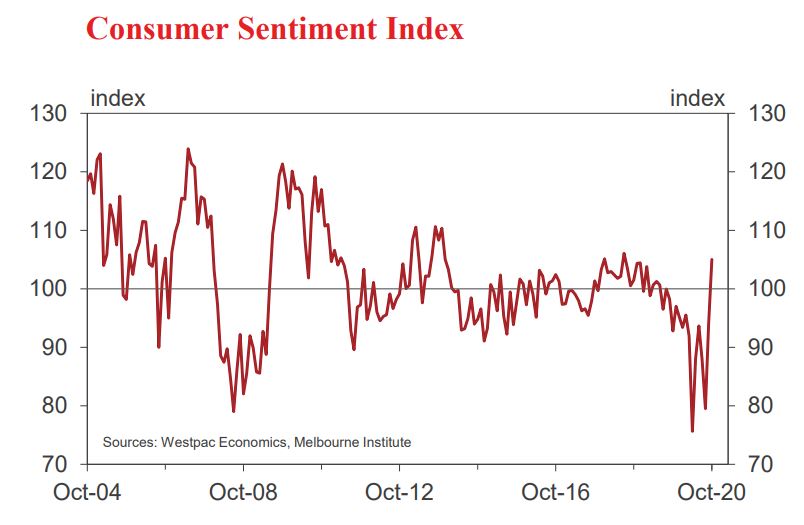

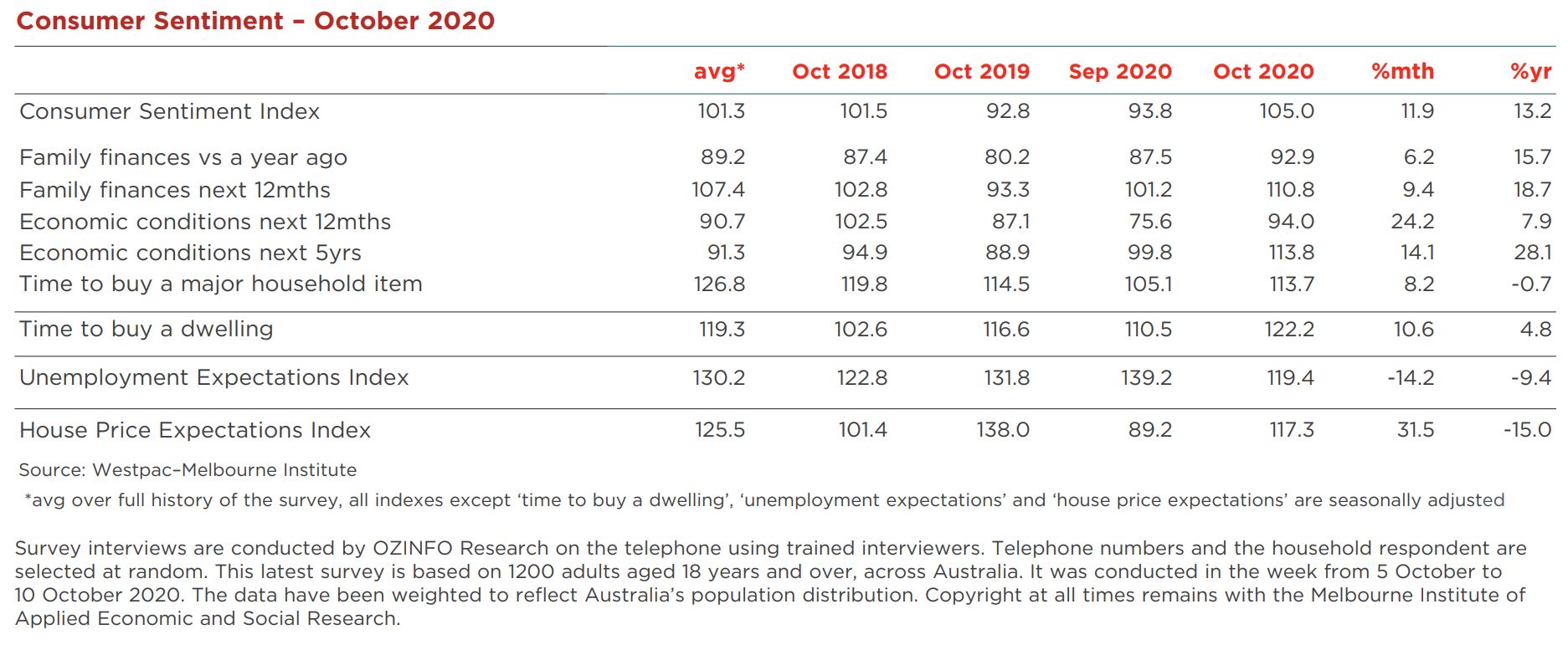

The Westpac-Melbourne Institute Index of Consumer Sentiment surged by 11.9% to 105.0 in October from 93.8 in September.

This is an extraordinary result. The Index has now lifted by 32% over the last two months to the highest level since July 2018. The Index is now 10% above the average level in the six months prior to the pandemic.

Such a development must be attributable to the response to the October Federal Budget; ongoing success across the nation in containing the COVID-19 outbreak; and the expectation that the Reserve Bank Board is likely to further cut interest rates at its next meeting on November 3.

Since 2010 we have conducted a post Budget question in the survey to assess the response of households to the Budget announcement.

Over that period, the net balance of respondents who assessed that the Budget would ‘improve their finances’ was –29%, a clear majority expecting measures to adversely affect their finances. We have never seen a Budget response that showed a net positive balance – until now.

For this Budget we saw a net positive balance of 9.5% indicating that a clear majority of respondents assessed that the Budget would ’improve their finances’.

Within the overall result there is a positive balance of 21.9% from males compared to a slight negative of –3.7% for females.

Respondents in the 35 – 49 age group returned an average positive read of 19%; while those with annual incomes over $100,000 showed a positive balance of 25.7%.

The Budget and the outlook for interest rates have given a clear boost to the confidence of homeowners. Respondents with a mortgage saw their confidence lift by 12.7% while those who fully own their homes lifted by 13.5%.

Confidence lifted in all states.

Notably, the success NSW has been having in remaining ‘open’ despite some daily evidence of new cases has really buoyed its citizens. Confidence in NSW surged by 17.5% compared to more subdued responses in Queensland (up 7.1%), WA (up 2.4%) and SA (up 9.3%).

Another welcome surprise was a solid lift of 13.7% in Victoria to a level now comparable with most states except NSW. Clearly the citizens of Victoria are eagerly anticipating an imminent reopening in Melbourne. Any significant delay is likely to see confidence in Victoria held back.

All components of the Index were higher in October. The most striking improvements were around the outlook for the economy. The ‘economy, next 12 months’ sub-index increased 24% while the ‘economy, next 5 years’ sub-index was up by 14%. Despite the lift in the 12 month outlook, this component is still only back near its August 2019 level. On the other hand, the surge in the five year outlook has taken this sub-index to its highest level since August 2010, a much more encouraging signal. Respondents are likely to be seeing the Budget as setting a foundation for a sustained lift in Australia’s economic fortunes.

Respondents are also more positive about their family finances. The ‘finances vs a year ago’ sub-index lifted 6.2% to the highest level since February 2016 and the ‘finances, next 12 months’ sub-index increased 9.4% to the highest level since September 2013.

We are pleased that the ‘time to buy a major item’ subindex was up by a solid 8.2% to 113.7. That level is still lower than the print in December 2019, indicating that households remain cautious about major spending decisions.

The survey provides us with an insight into confidence in the labour market. There was a stunning lift in confidence around job security. The Index improved by 14.2% to be back around the levels of early 2019. Despite media warnings about the looming ‘fiscal cliff’, respondents have become markedly more confident about job security. In particular, those over 45 saw a 20% lift in confidence – that was despite job-related measures in the Budget only providing specific support for younger employees.

Of all the results in this extraordinary survey, this one is the most surprising and reassuring.

Confidence in the housing market has boomed. The ‘time to buy a dwelling’ index increased 10.6% to its highest level since September 2019. As with the overall Index the result for NSW (now 120.4) was outstanding with an 11.3% rise compared to 7.0% in Victoria (now 118.0) and 4.4% in Queensland (now 118.6).

The levels of the index in each of these eastern states are comparable, indicating a high degree of expectation that the Victorian market is set to reopen.

The two states that have traditionally lagged the eastern states in the housing market but which are now dealing most successfully with the virus are standouts with respect

The forecasts given above are predictive in character. Whilst every effort has been taken to ensure that the assumptions on which the forecasts are based are reasonable, the forecasts may be affected by incorrect assumptions or by known or unknown risks and uncertainties. The results ultimately achieved may differ substantially from these forecasts.

Survey interviews are conducted by OZINFO Research on the telephone using trained interviewers. Telephone numbers and the household respondent are selected at random. This latest survey is based on 1200 adults aged 18 years and over, across Australia. It was conducted in the week from 5 October to 10 October 2020. The data have been weighted to reflect Australia’s population distribution.

Our key measure of house price expectations has also risen strongly, by 31.5% to 117.3 from 89.2. All states registered impressive recoveries: NSW (111. 7) lifted by 22.8%; Victoria (100.6) by 25.8%; QLD (134.1) by 50%; WA (141) by 46.5%; and SA (112) by 19.6%.

The national Index is now ‘only’ 17% below its pre-pandemic level and back around the level seen in July last year. There is clear optimism in smaller states – where housing has underperformed the major eastern states for several years – although the apparent resilience of the Victorian market is impressive.

The Reserve Bank Board is scheduled to meet on November 3. As discussed, one of the likely factors behind the surge in sentiment this month is an expectation that the Board is set to cut the overnight cash rate from 0.25% to 0.10%. That is expected to be in tandem with a cut in the target for the three year bond rate to 0.10%; the rate on the Term Funding Facility to 0.10% and a reduction in the rate the Reserve Bank pays on Exchange Settlement Accounts to 0.01%.

In our view, communication from the Bank over the last few weeks points to this outcome. The Budget papers and the Reserve Bank’s most recent forecasts highlight that official forecasts for the unemployment rate and inflation do not anticipate the Bank meeting its targets – full employment and inflation sustainably within the 2–3% band – by 2022.

Previous communications from the Bank pointed to an assessed ‘effective lower bound’ for rates of 0.25%. But recently, we have detected a change in attitude indicating more confidence that the plumbing of the financial system can operate effectively at an even lower set of policy rates.

With that in mind and the commitment towards full employment and the target for inflation there seems to be no reason for the Board to delay its decision.

That really is amazing. What can I say? Households are going to be very disappointed! I did note the near-total lack of debate around what the budget really is.

That said, Bill Evans should be far more cautious than he is. It is an outlier versus the ANZ/Roy Morgan measure:

Advertisement

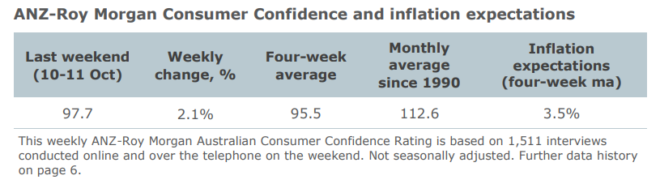

From ANZ-Roy Morgan:

Confidence gained 2.1% last week, its sixth straight weekly gain. All the sub-indices gained except ‘current finances’.

‘Current financial conditions’ declined 1.5%, while ‘future financial conditions’ gained 3.7% for its fifth straight week.

‘Current economic conditions’ gained 4.6% and is up around 23% over the six-week confidence gain. Confidence in current economic conditions is still very subdued, however. ‘Future economic conditions’ gained 3.1%, its fourth straight weekly increase.

‘Time to buy a household item’ gained 0.5% and the four-week moving average of ‘Inflation expectations’ gained 0.1ppt to 3.5%.

ANZ Head of Australian Economics, David Plank, commented:

Consumers have given a thumbs up to the Budget, with sentiment rising 2.1% to its highest level since the last weekend of May. This is the second best post budget gain in the last six years. There were healthy gains in ‘future finances’ and ‘current’ and ‘future’ economic conditions. Surprisingly, sentiment is weaker in New South Wales, including Sydney, than it is in Melbourne. Less surprisingly, confidence is strongest (and above neutral) in Perth. It is also above neutral in Tasmania and South Australia.

Some modest improvement. But sentiment remains 13.2pts lower than a year ago and 14.9 points lower than the long-term average.

Still got miles to go before consumer confidence is back to ‘normal’.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.