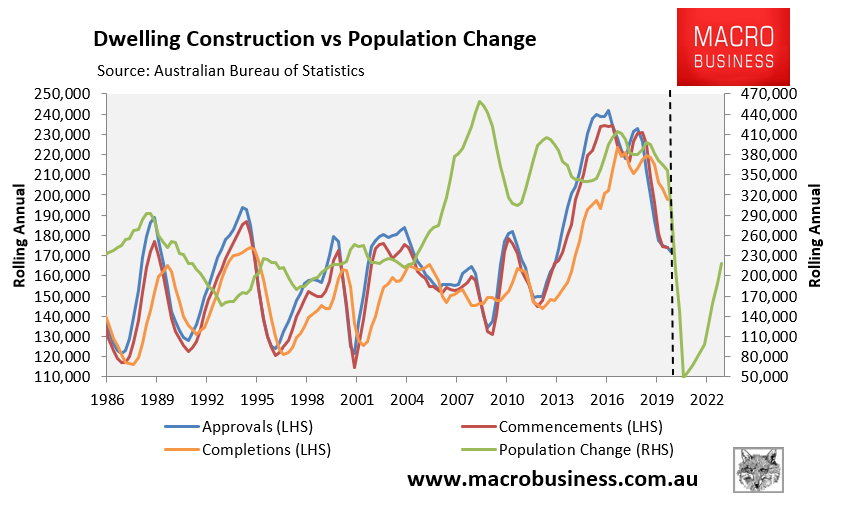

Last week I produced a series of charts plotting Australia’s projected population growth, as forecast in last week’s federal budget, against the latest dwelling approvals, commencements and completions data from the Australian Bureau of Statistics (example below).

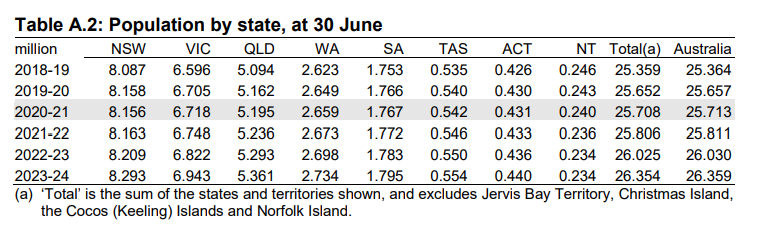

The population data these charts were based upon is presented below, taken directly from the federal budget:

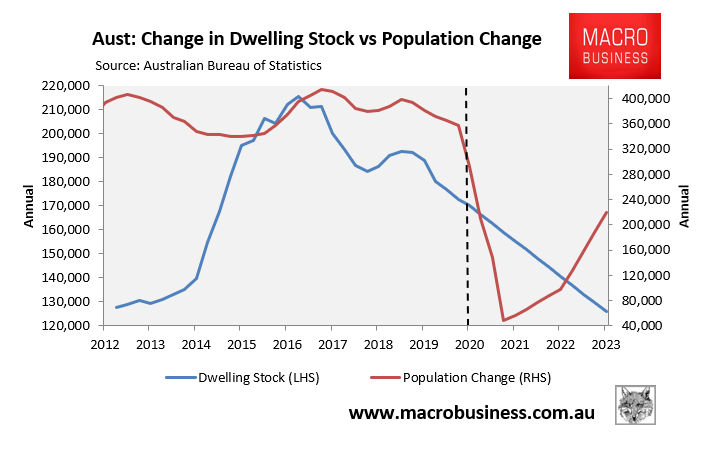

Today I want to go one step further and present the same population data against the net dwelling additions data (completions minus demolitions) provided by the Australian Bureau of Statistics.

As this dwelling additions data is only current to June 2020, I have assumed that they continue to fall over the three year forward estimates to their cyclical lows over the past decade.

The below chart plots these projections at the national level:

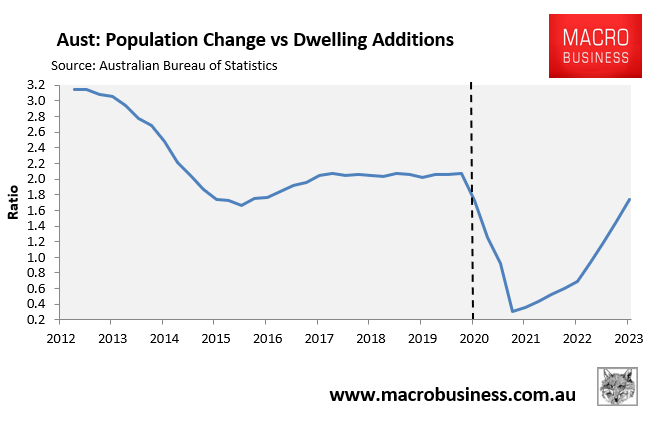

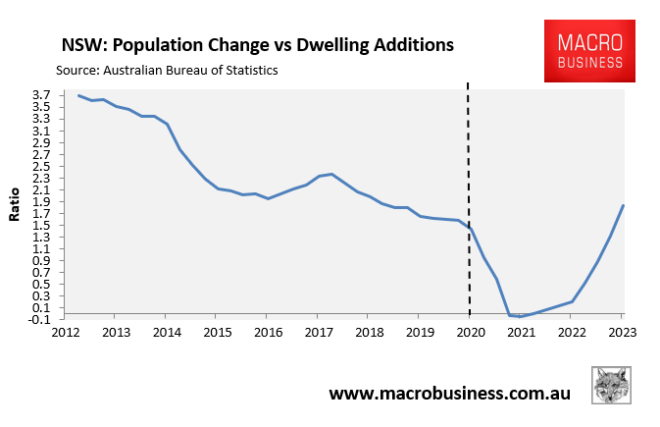

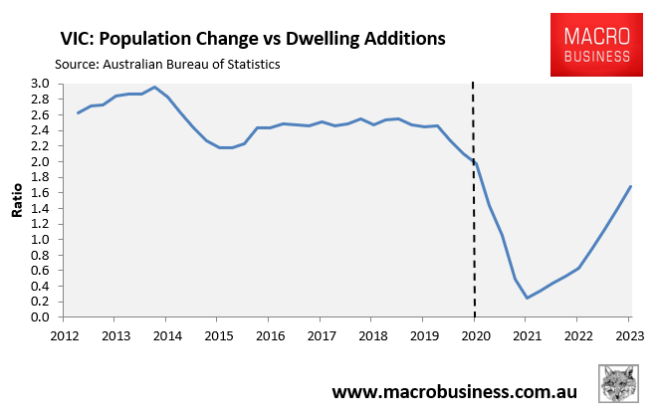

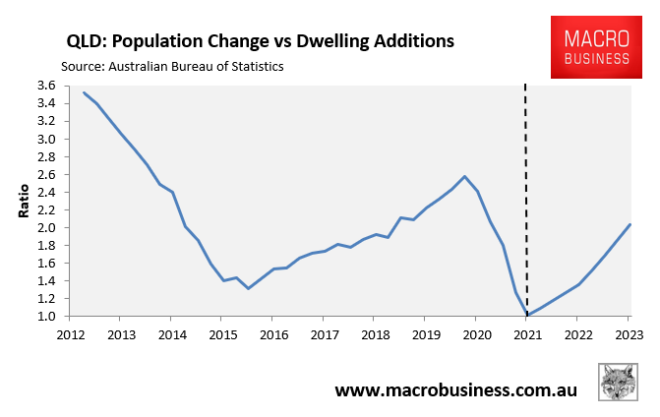

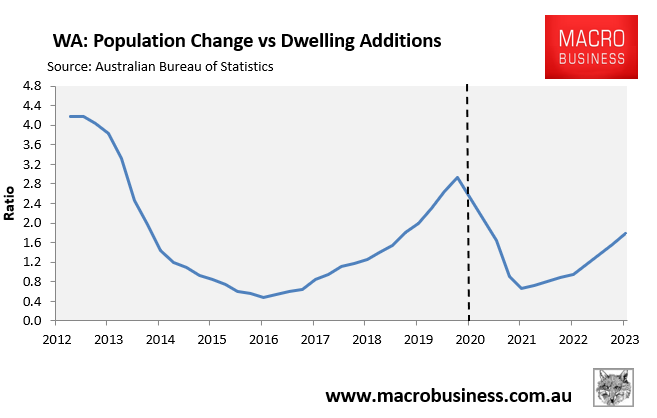

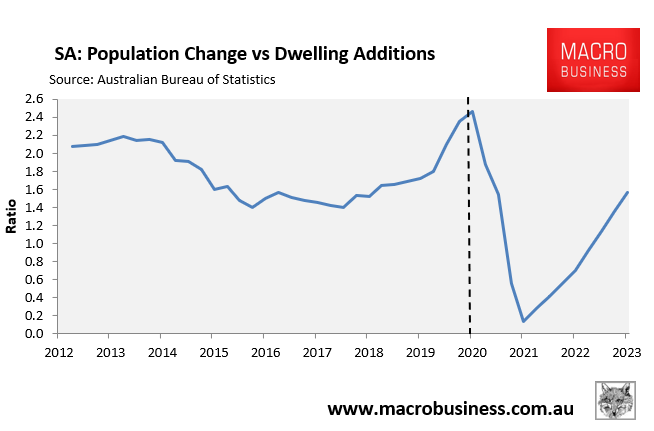

The next chart presents this same data as a ratio of population increase versus net dwelling additions:

As you can see, even if dwelling construction falls gradually to cyclical lows (125,900 a year in 2023), Australia will face a whopping supply glut of 155,000 net dwelling additions versus 56,000 population increase in 2021 and 141,000 net dwelling additions versus 98,000 population increase in 2022.

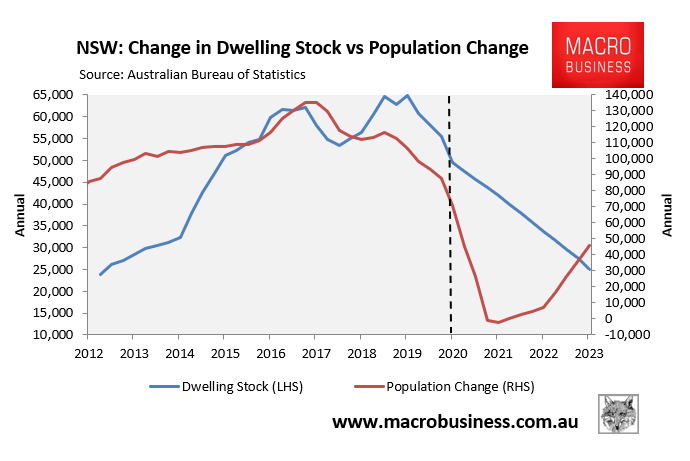

Next are the same charts for NSW:

NSW faces a gigantic supply glut with 42,000 net dwelling additions versus a 2,000 population decline in 2021 and 34,000 net dwelling additions versus 7,000 population increase in 2022.

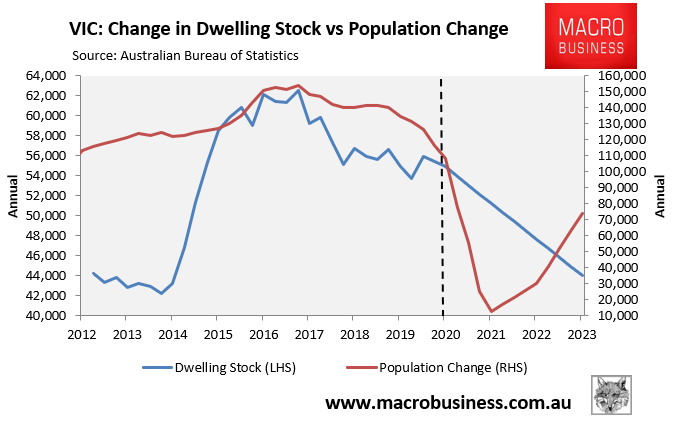

Next VIC:

VIC also faces an enormous supply glut with 51,000 net dwelling additions versus 13,000 population growth in 2021 and 48,000 net dwelling additions versus 30,000 population increase in 2022.

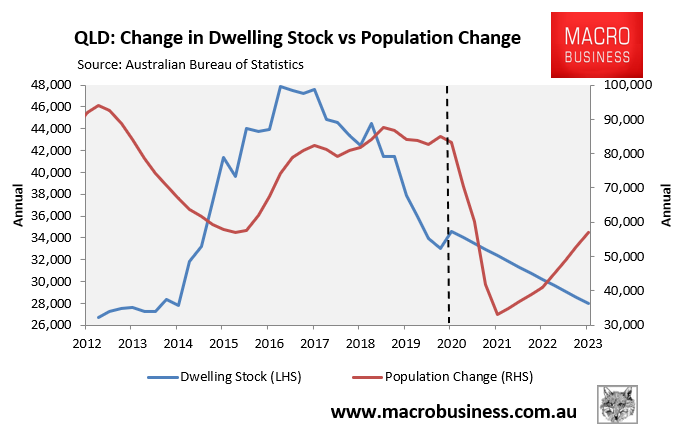

Next QLD:

QLD faces a smaller supply glut with 32,000 net dwelling additions versus 33,000 population growth in 2021 and 30,000 net dwelling additions versus 41,000 population increase in 2022.

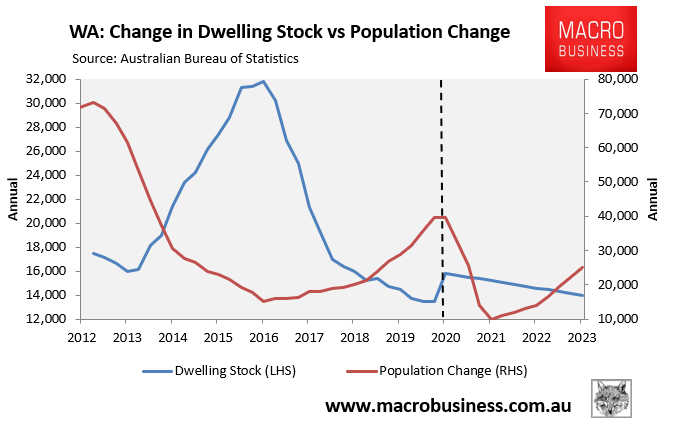

Next WA:

WA faces a big supply glut with 15,000 net dwelling additions versus 10,000 population growth in 2021 and 15,000 net dwelling additions versus 14,000 population increase in 2022.

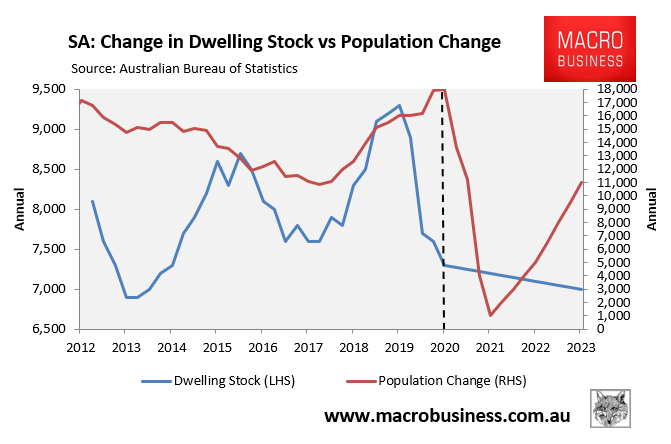

Finally, SA:

SA faces a huge supply glut with 7,200 net dwelling additions versus 1,000 population growth in 2021 and 7,100 net dwelling additions versus 5,000 population increase in 2022.

There is no sugar coating this data. Australia’s major housing markets are facing enormous property supply gluts as immigration and population growth collapses.

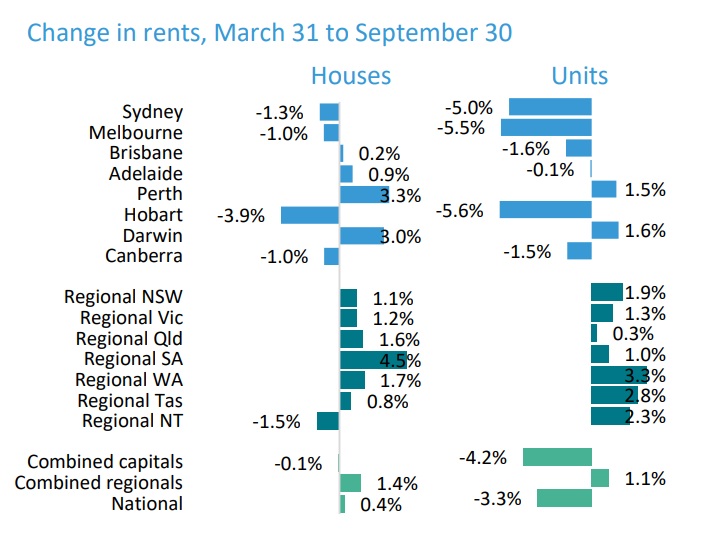

This will ensures that rental vacancies continue to balloon and rents will continue to fall, with apartments in Sydney and Melbourne most likely to be impacted:

I would not want to be a financially stretched landlord in either Sydney or Melbourne right now. On the flipside, it will be great for renters.