The ECB is back in the game. Here is last night’s statement:

Ladies and gentlemen, the Vice-President and I are very pleased to welcome you to our press conference. We will now report on the outcome of today’s meeting of the Governing Council, which was also attended by the Commission Executive Vice-President, Mr Dombrovskis.

The resurgence in coronavirus (COVID-19) infections presents renewed challenges to public health and the growth prospects of the euro area and global economies. Incoming information signals that the euro area economic recovery is losing momentum more rapidly than expected, after a strong, yet partial and uneven, rebound in economic activity over the summer months. The rise in COVID-19 cases and the associated intensification of containment measures is weighing on activity, constituting a clear deterioration in the near-term outlook. In fact, while activity in the manufacturing sector has continued to recover, activity in the services sector has been slowing visibly. Although fiscal policy measures are supporting households and firms, consumers are cautious in the light of the pandemic and its ramifications for employment and earnings. Moreover, weaker balance sheets and increased uncertainty about the economic outlook are weighing on business investment. Headline inflation is being dampened by low energy prices and muted underlying price pressures in the context of weak demand and significant slack in labour and product markets.

The monetary policy measures that we have taken since early March are helping to preserve favourable financing conditions for all sectors and jurisdictions across the euro area, thereby providing crucial support to underpin economic activity and to safeguard medium-term price stability. At the same time, in the current environment of risks clearly tilted to the downside, the Governing Council will carefully assess the incoming information, including the dynamics of the pandemic, prospects for a rollout of vaccines and developments in the exchange rate. The new round of Eurosystem staff macroeconomic projections in December will allow a thorough reassessment of the economic outlook and the balance of risks. On the basis of this updated assessment, the Governing Council will recalibrate its instruments, as appropriate, to respond to the unfolding situation and to ensure that financing conditions remain favourable to support the economic recovery and counteract the negative impact of the pandemic on the projected inflation path. This will foster the convergence of inflation towards its aim in a sustained manner, in line with its commitment to symmetry.

In the meantime, we decided to reconfirm our accommodative monetary policy stance.

We will keep the key ECB interest rates unchanged. We expect them to remain at their present or lower levels until we have seen the inflation outlook robustly converge to a level sufficiently close to, but below, 2 percent within our projection horizon, and such convergence has been consistently reflected in underlying inflation dynamics.

We will continue our purchases under the pandemic emergency purchase programme (PEPP) with a total envelope of €1,350 billion. These purchases contribute to easing the overall monetary policy stance, thereby helping to offset the downward impact of the pandemic on the projected path of inflation. The purchases will continue to be conducted in a flexible manner over time, across asset classes and among jurisdictions. This allows us to effectively stave off risks to the smooth transmission of monetary policy. We will conduct net asset purchases under the PEPP until at least the end of June 2021 and, in any case, until the Governing Council judges thatthe coronavirus crisis phase is over. We will reinvest the principal payments from maturing securities purchased under the PEPP until at least the end of 2022. In any case, the future roll-off of the PEPP portfolio will be managed to avoid interference with the appropriate monetary policy stance.

Net purchases under our asset purchase programme (APP) will continue at a monthly pace of €20 billion, together with the purchases under the additional €120 billion temporary envelope until the end of the year. We continue to expect monthly net asset purchases under the APP to run for as long as necessary to reinforce the accommodative impact of our policy rates, and to end shortly before we start raising the key ECB interest rates. We intend to continue reinvesting, in full, the principal payments from maturing securities purchased under the APP for an extended period of time past the date when we start raising the key ECB interest rates, and in any case for as long as necessary to maintain favourable liquidity conditions and an ample degree of monetary accommodation.

We will also continue to provide ample liquidity through our refinancing operations. In particular, our third series of targeted longer-term refinancing operations (TLTRO III) remains an attractive source of funding for banks, supporting bank lending to firms and households.

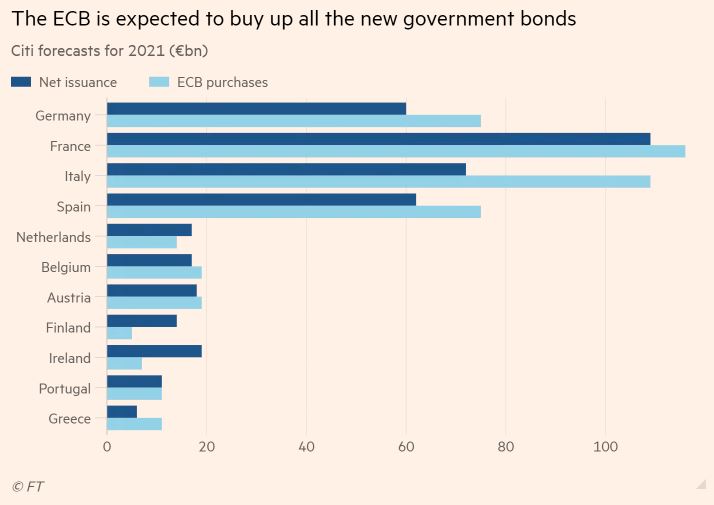

The FT notes that the central bank is on track to buy more sovereign bonds than are issued in total over the next year:

Investors will not have to contribute a single euro to finance the vast budget deficits of eurozone governments next year, according to analysts who forecast that the European Central Bank will buy a greater quantity of debt than all the new bonds hitting the market.

Draft budget plans published by EU member states earlier this month showed that deficits are expected to remain sky high even as economies rebound from the effects of the Covid-19 pandemic.

But, according to calculations by Citigroup, ECB purchases will more than cover the extra cash that governments need in 2021 — even if the central bank does not scale up its €1.35tn emergency bond-buying programme by another €500bn in December as is widely expected. Christine Lagarde, the ECB’s president, hinted at a policy-setting meeting on Thursday that further stimulus is on the way.

Advertisement

This should be bullish, right? MOAR liquidity etc. The problem is that the statement was more dovish than the market (not me) was expecting and the ECB is now clearly fighting the Fed.

Europe is leading the lockdowns as well and its inflation profile is much weaker than the US:

Advertisement

Yet it is unlikely to provide another round of fiscal stimulus, relying more on the ECB.

This is not the profile of rising currency, as the EUR has been all year. Especially since, once US election fears ease, its fiscal program will resume more strongly than in Europe delivering better growth and inflation outcomes.

It is certainly true that a recovering US is bullish for the EUR as capital flows outwards and its exports lift, but the virus is forcing the ECB to fight the Fed now and until we get some whiff or a stronger US recovery then that is going to put more upwards pressure on DXY which, in turn, is bad for reflation everywhere, especially commodities and the Australian dollar.

Advertisement

This will act as a brake on global recovery, on gold, on commodities, on AUD appreciation and on all reflation next year.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.