The usual suspects are fretting over the Australian Government’s ballooning debt, claiming we will leave a nasty legacy for future generations:

“On very optimistic projections, we don’t think Australia will be debt-free until the early 2080s,” said Cian Hussey, research fellow at conservative think tank the Institute of Public Affairs.

The Federal Government has committed to a record $213.7 billion deficit this year as it attempts to borrow and spend its way out of Australia’s first recession in nearly three decades – brought on by devastating COVID-19 lockdowns.

Asked by Sunrise host David Koch on Wednesday whether it was fair to leave a huge debt for future generations to pay off, Mr Morrison hit back.

“There will be nothing to leave to our children if we didn’t act now, David,” he said.

“This is the worst recession we’ve seen since the Great Depression. This is 45 times worse an impact on the global economy than we saw during the global financial crisis. We’ve targeted (the spending), it’s proportionate, it’s scalable and it’s temporary. And that’s to enable us to get back on our feet and get going again.”

The IPA has modelled two scenarios, one in which gross debt peaks at $1.92 trillion in 2037, the budget returns to surplus the following year, and the debt is paid off by 2063.

The second scenario has debt peaking at $2.05 trillion in 2042, a return to surplus in 2046, and the debt paid off by 2080.

In the first scenario, GDP growth stabilises at 5 per cent, whereas in the second it settles at 3 per cent.

Mr Hussey told news.com.au budget forecasts “tend to be optimistic” so it was “pretty depressing that the Morrison Government hasn’t even tried to outline when we might see a surplus or pay down the debt”…

Would the IPA seriously prefer that federal government cut spending? This would be a terrible idea as it would send the economy into an austerity-led depression, driving unemployment into the stratosphere, causing widespread business failures, and tanking tax receipts.

The Australia’s government should instead take advantage of record low borrowing rates to ramp-up infrastructure and public housing spending. Not only would this help overcome Australia’s massive infrastructure and public housing deficits (brought about by 15 years of mass immigration), but would also help stimulate the economy during a period of weak private demand and high unemployment.

Advertisement

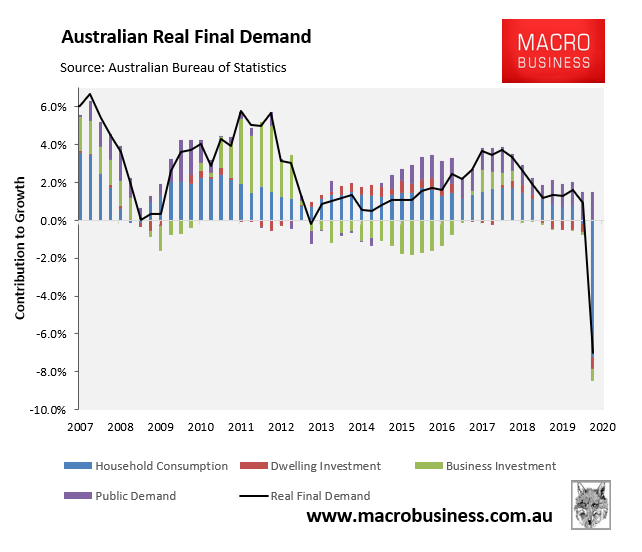

Indeed, in the absence of public spending, the Australian economy would already be in a much deeper hole:

One only needs to look at the experience of the UK after the GFC to see how ill-advised the IPA’s prescriptions are.

Advertisement

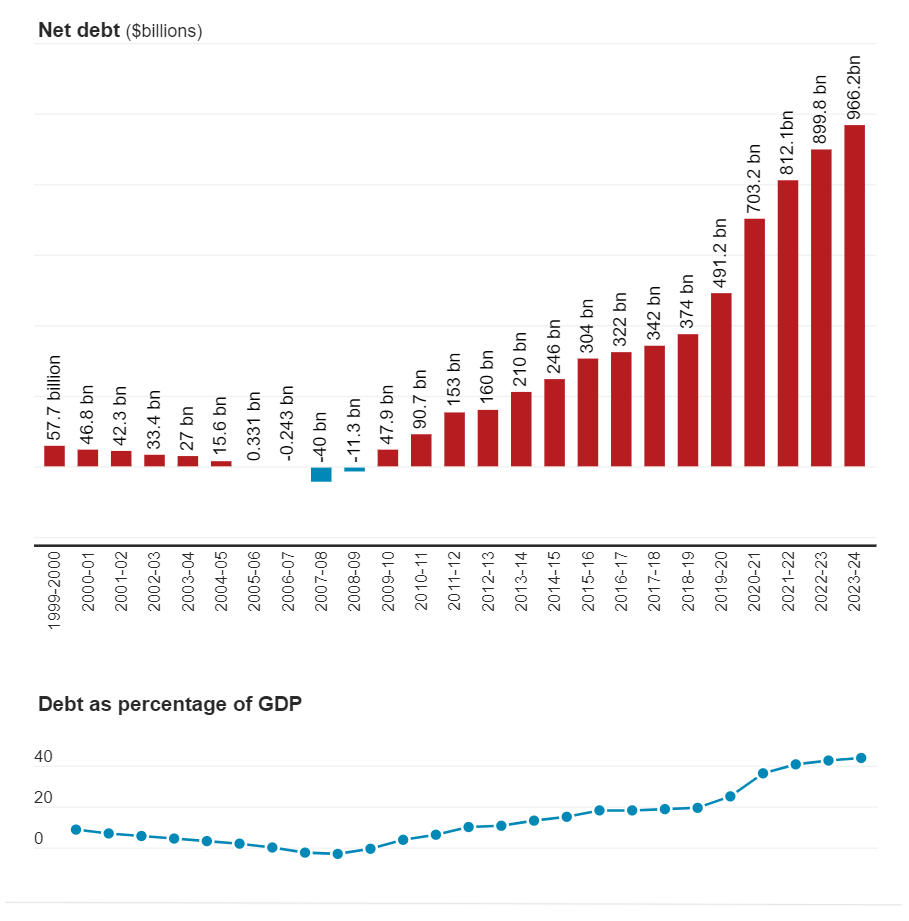

Nor should we worry about the national debt. Although debt is projected to hit nearly $1 trillion next financial year, because of record low interest rates, the cost of servicing it as a percentage of GDP will be almost half of what it was during the last recession of 1992.

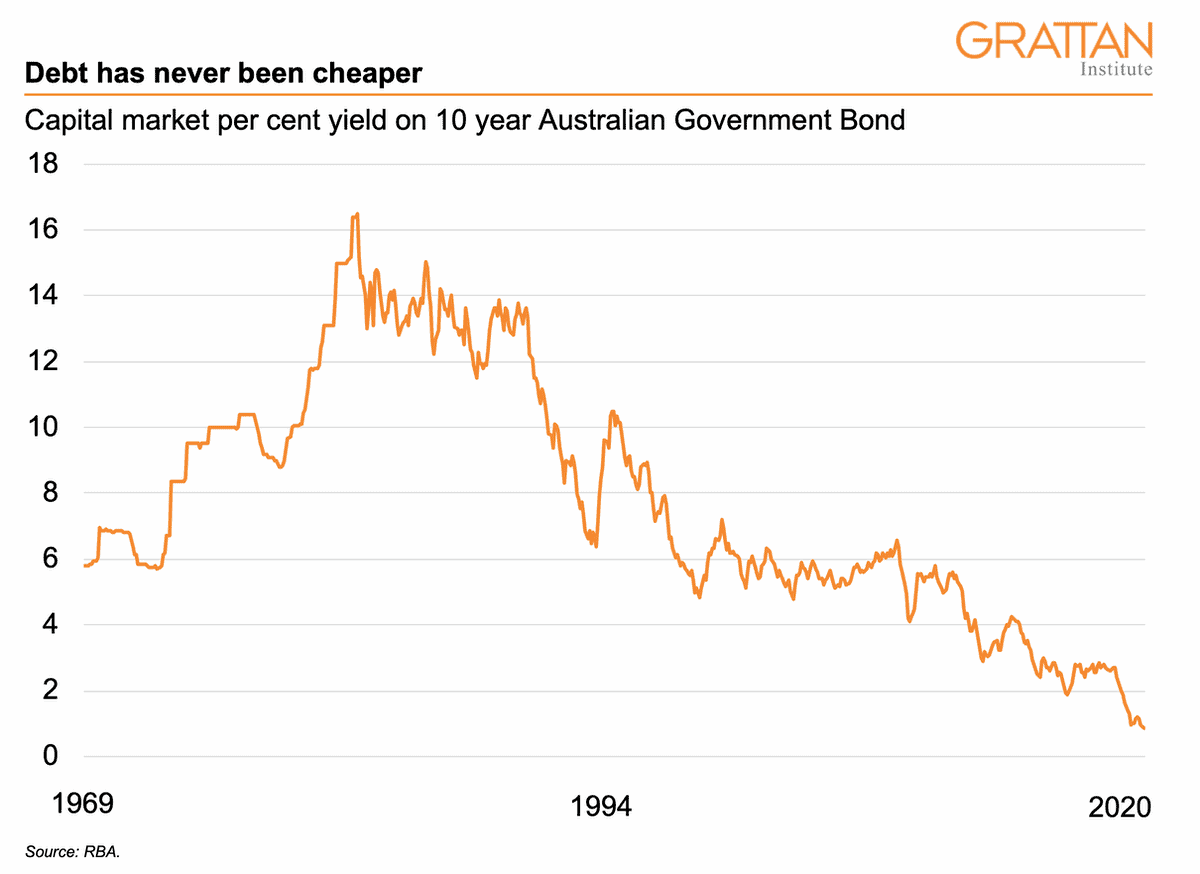

It has never been cheaper for governments to borrow. As the next chart shows, the interest rate on 10-year Australian Government Bonds is less than 1%. If inflation stays above 1%, as the Reserve Bank and Treasury expect, the “real” interest rate the federal government pays on the bond will be negative. That is, it will effectively be paid to borrow.

These very low interest costs change the dynamics of managing debt we accrue now. Investments that boost future growth – including spending to reduce unemployment and close the output gap – will pay for themselves.

This is the fiscal “free lunch” spoken about by the former chief economist of the International Monetary Fund, Olivier Blanchard, and the deputy governor of the Reserve Bank of Australia, Guy Debelle…

The good news is that with interest rates on government borrowing so low, debt as a share of GDP can be reduced without pursuing austerity in the form of deficit reduction…

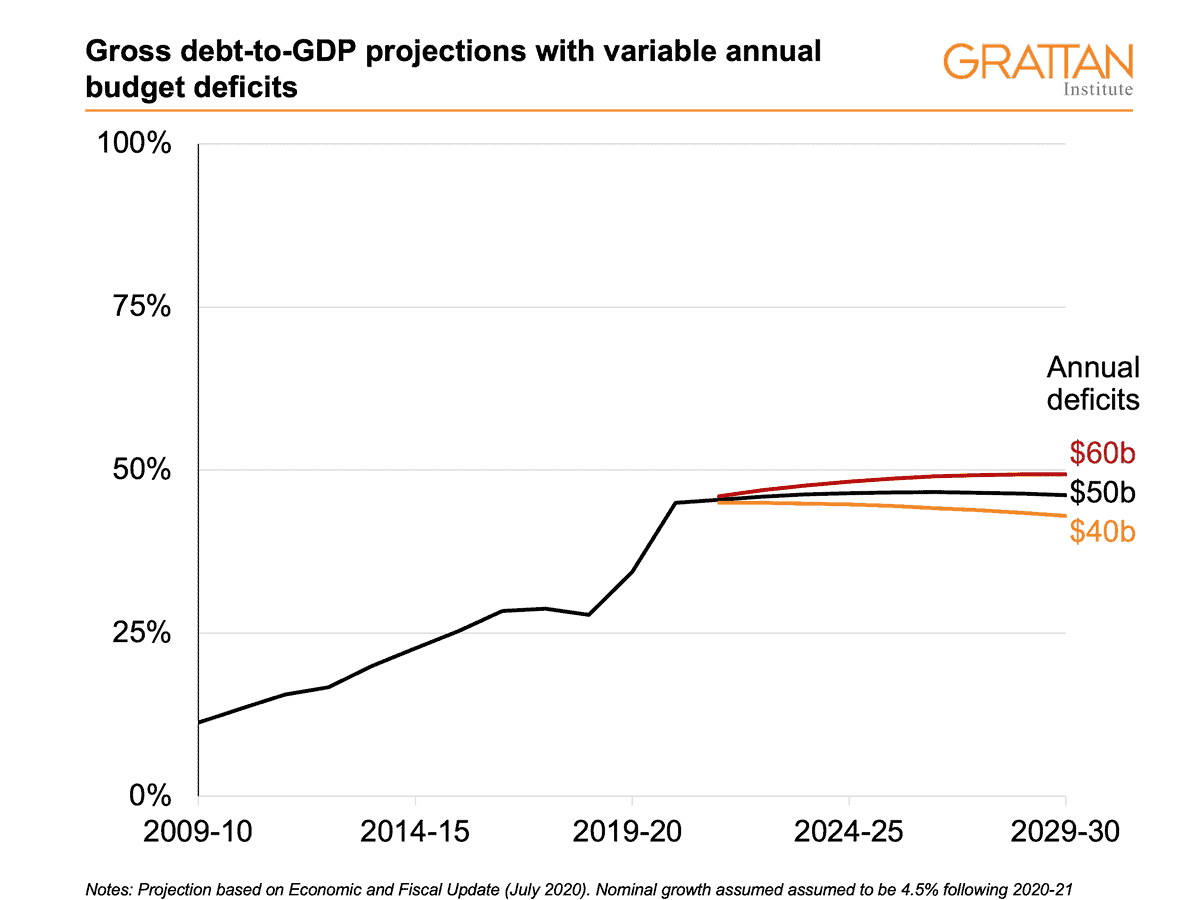

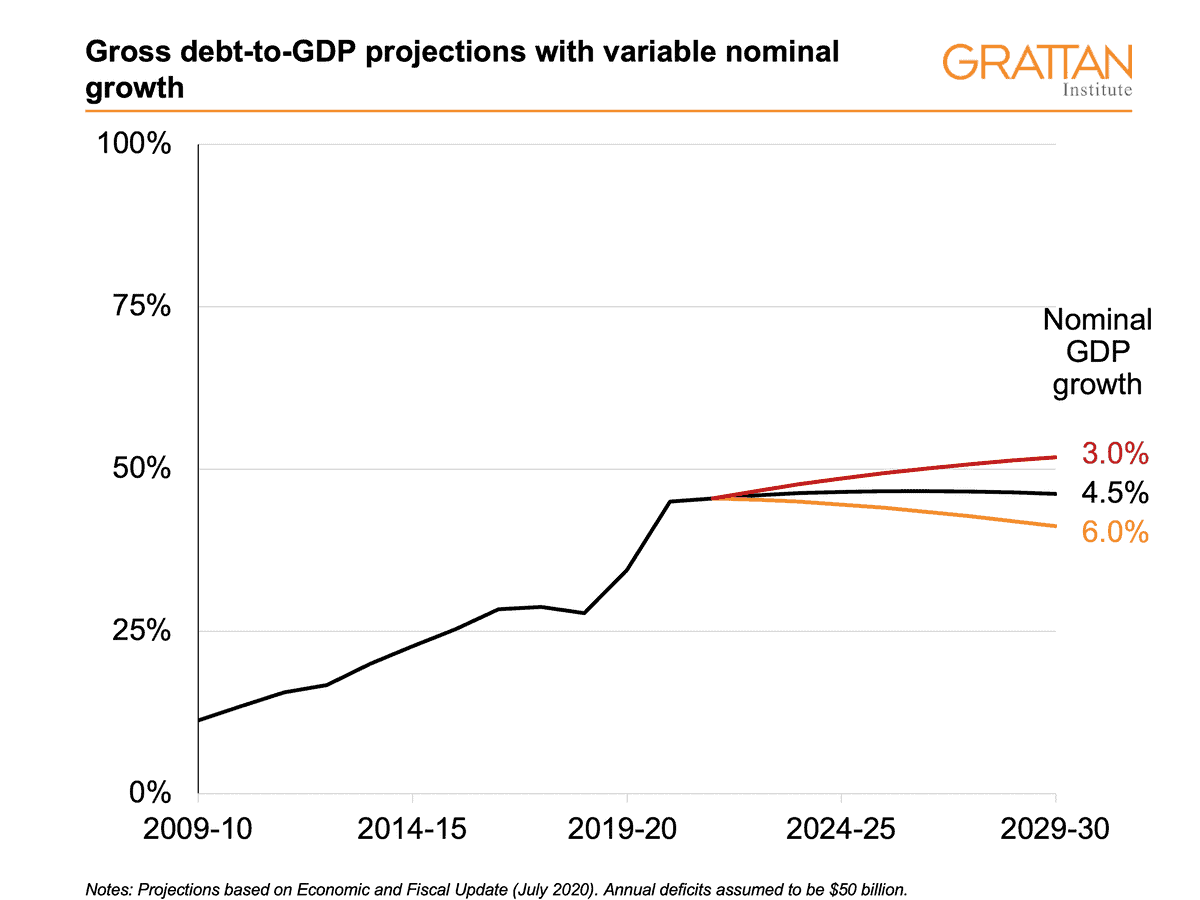

Even if interest rates were a little higher than now (say, 1.5%), the government can reduce debt relative to GDP even while continuing to run large deficits, provided that nominal GDP growth returns to a moderate level (say, 4.5%, as it was before the pandemic).

The next chart shows that under these circumstances the government can run deficits of up to $50 billion and still reduce debt as a share of GDP.

Different rates of GDP growth would change this story, as the next chart shows. With an even higher nominal growth rate, debt would shrink even faster relative to GDP. In a scenario of prolonged low growth, debt would increase relative to GDP a little, but remain very modest.

The government can do things to boost nominal growth in areas such as tax reform, education and skills, workforce participation, energy and climate policy, and land-use planning. The Reserve Bank should also do more by boosting inflation, which would support nominal growth.

Advertisement

The bottom line is that now is not the time for budget austerity. The federal government should instead borrow and spend to smooth the economic shock.

The alternative is much slower growth, rising unemployment, rising business failures, and thousands of Aussie being needlessly thrown into poverty.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.