With rate cuts and QE expansion now well priced in for the 3 Nov RBA meeting, we see reduced potential for idiosyncratic AUD weakness going forward. We leave our pre-election AUDUSD target unchanged at 0.70. In the aftermath of US elections, we expect AUD price action to follow developments in risky assets more broadly.

The price action in AUDUSD since our most recent update on 23 Sep, when we revised our target lower from 0.7350 to 0.7000 (link), has been rather choppy but overall consistent with our theme of idiosyncratic weakness. The relentless dovish rhetoric from the RBA over the past three weeks has played a key role in this, as suggested by the otherwise constructive tone observed in the vast majority of other pro-cyclical currencies over that time frame. As we near the now highly anticipated 3 November RBA rate decision, we preview the potential scenarios for monetary policy.

Hawk, Hawk, Dove

The RBA has rapidly gone from being one of the most hawkish banks in G10 throughout the northern summer, to quickly voicing its willingness to do more to support the economy. The speech by Deputy Governor Debelle on 22 Sep marked the beginning of the turn, with notable follow ups in speeches from Governor Lowe on 14 Oct and by Assistant Governor Kent on 20 October. The three speeches contain a wealth of information about the RBA’s possible policy options, which can in our view be summarized as follows.

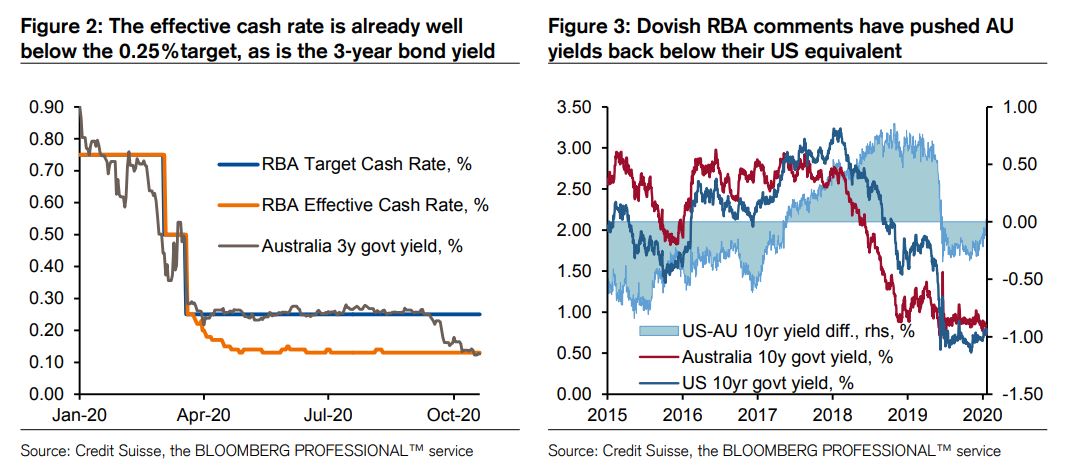

Rate cuts: Governor Lowe has been rather clear in saying that cuts to the target cash rate, currently at 0.25%, are on the table. Given previous reluctance by RBA officials to consider rates at 0% or below, markets expect the RBA to cut the cash rate by 15bps to 0.10%, an idea that Deputy Governor Debelle also floated in his 22 Sep speech. This would be in line with the interest rate that banks currently receive on their surplus Exchange Settlement balances in their accounts with the RBA. Realistically this rate would also be lowered if the RBA were cut to the target cash rate, but by less than 10bp, creating a tighter interest rate corridor.

The FX impact of this measure could be blunted by the fact that the effective cash rate is already below the 0.25% target rate and is currently trading around 0.13%, mostly explained by the abundance of liquidity in the system. A cut in the target cash rate to 0% would represent a dovish surprise relative to market expectations. At this point it seems a fairly unlikely outcome.

Asset purchases: Ahead of the Lowe speech, markets had already been expecting some form of asset purchase extension, as suggested by the 3- year yield falling below the RBA’s 0.25% target without any countervailing asset purchases by the Bank. On 14 October then, Governor Lowe made the observation that Australia’s 10-yr yield is higher than its peers. The immediate response in markets was a 10bp drop in the 10-year yield. Overall, markets viewed the statement as solidifying expectations of a shift in asset purchases from the current yield curve control approach (with purchases aimed at keeping the 3-year bond yield at 0.25%) to one that targets the belly of the curve, with less focus on market-based objectives and clear specifications on quantities. In that sense, a decision that produces instead an extension of the current YCC framework to e.g. the 5-year yield, without more precise definitions of purchases quantities, might be viewed by markets as somewhat disappointing.

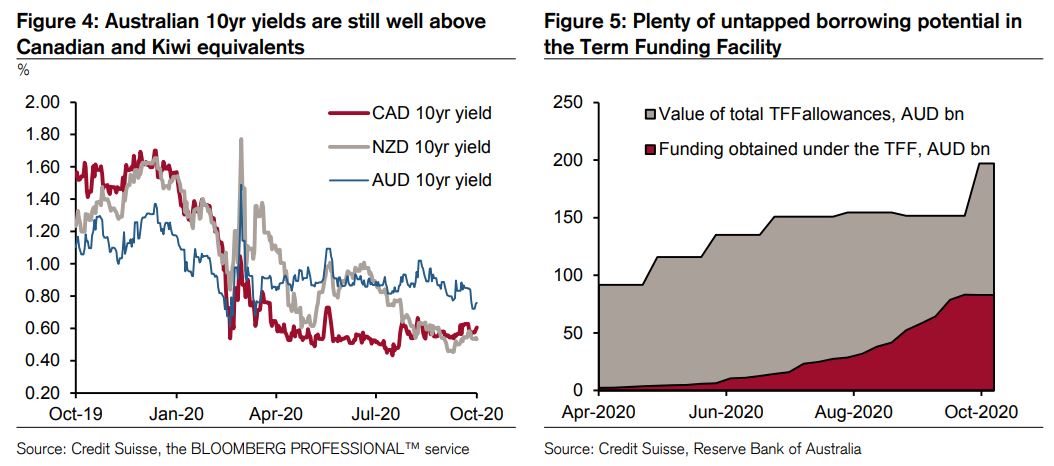

Funding facility: The speech by Assistant Governor Kent on 20 October instead focused on the third key policy stimulus tool, i.e. the Term Funding Facility (TFF). The TFF was introduced on 19 March to provide secured 3- year funding for banks at 0.25%, and its capacity was expanded to A$200bn at the 5 October RBA rate decision. With the take up by local banks still well below the facility’s maximum capacity, the possibility of further expansion in the TFF seems currently less likely than the rate cuts or further QE. A cut in the facility’s interest rate from current 0.25% is however quite likely, in the event of a cut in the target cash rate. The coincident timing of the RBA decision and of US elections makes gauging market expectations for the RBA meeting via vol metrics somewhat tricky. Nevertheless, the weak price action in spot AUD (especially amid more constructive price action in the rest of the cyclical FX spectrum), the ongoing pressure on the effective rate, and the large pullback in 3-year and 10-year yields all point to the dovish RBA shift now being to some extent priced-in. This is not to say that QE will not be effective – the still elevated level of 10yr AUD yields vs CAD and NZD suggests that the gap Governor Lowe pointed to is still present. But in terms of how this feeds into FX market expectations, with carry being negligible already, we view the lacklustre AUD performance over the past month as already quite notable, and likely reflecting a shift in RBA expectations.

This overall leaves us inclined to not change our pre-election AUDUSD target from the current 0.70 level, despite spot FX being at the time of writing fairly close to the target. The following also factors also contribute to our view:

1) Barring a spectacular surprise decision from the RBA on 3 November (e.g. no easing at all, or at the other extreme, target cash rate cut to 0%), we suspect that price action in AUDUSD will be more closely driven by the outcome of the US election around that date and in the following weeks. Over the past month, market expectations have been resiliently set on a “blue sweep” outcome and on ensuing USD weakness. AUD has not participated in the price action, and is therefore likely to be viewed as a “catch up” play in the event of an election outcome in line with market expectations. In the event of a less USD-negative / risk-positive outcome from US elections, we think it is reasonable instead to expect the procyclical aspect of AUD to push the pair sub 0.70.

2) While the RBA has been clear in its intention to ease policy, it is worth noting that the data picture in Australia is far from clear in pointing to urgent need for easing. On 19 October restrictions in the Victoria state were lowered from level 4 to level 3, which creates potential for near-term positive surprises. Similarly the positive momentum in Chinese demand also points to potential for constructive data surprises in Australia. This could prove quite important for AUD, especially if the RBA were to hint at data dependency in its rate decision and leave some discretion on asset purchases.

3) Lastly, the expansion in fiscal policy announced on 6 Oct represents another potential positive factor that might make the RBA less willing to employ an “easing at all costs” approach, and might therefore lead to risks of a less committed policy easing stance than some in markets might be expecting.

I know it is a great tradition for the RBA to disappoint. But the recent conversion to QE is pretty convincing and I expect that the bank will wade out all the way to ten-year maturity purchases. There isn’t much point doing anything if it does not do that.

I don’t think that that is fully priced into yields nor, therefore, currency.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.