The RBA decision on 6 Oct has reinforced the possibility of an easing announcement at the upcoming 3 Nov rate decision: with several speeches by RBA officials keeping policy expectations in focus between now and the decision, we see our pre-US elections AUDUSD 0.70 target as still intact.

Two weeks ago we turned less constructive on AUDUSD, revising our preelection target from 0.7350 to 0.7000 (link). Aside from considerations on the broad USD outlook, our decision was driven by the view that the RBA was getting ready to ease, as inspired by the 22 Sep speech by RBA Deputy Governor Debelle. We also saw a potential for an additional kicker in the 6 October budget announcement, noting that markets were pricing in a fairly limited amount of risk premium around the date of both the budget announcement of and the RBA rate decision.

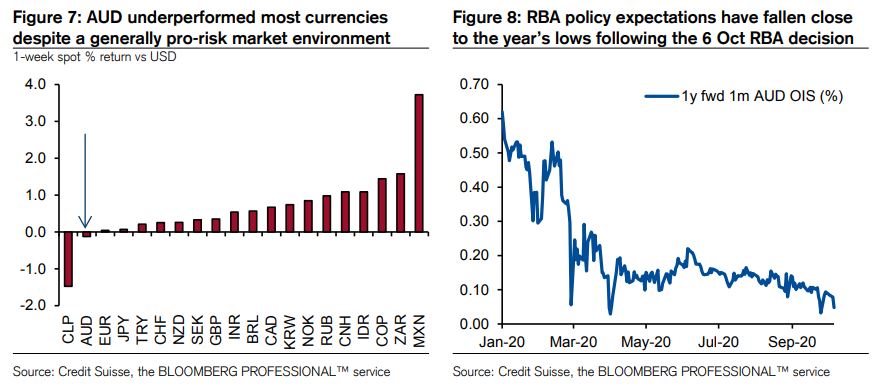

The view met its first test overnight, with the RBA releasing a dovish sounding statement from its rate decision meeting and the Treasury presenting an accommodative budget. The FX impact has overall been in line with our view, with AUDUSD lagging the otherwise mostly pro-risk price action in the rest of the G10 arena (Figure 7). Looking ahead to the rest of the month, we see scope for these themes to continue to play out: the following points on the monetary and fiscal policy outlook will be in focus.

The RBA prepares markets for a dovish shift

While the RBA did not actually deliver any policy easing overnight, it introduced rhetoric in its statement that markets viewed as reinforcing the dovish expectations first produced by the speech of Deputy Governor Debelle on 22 Sep. Language around further monetary stimulus and on the unemployment rate risks was viewed as particularly impactful, as suggested by priced-in policy expectations falling to near the lows of the year after the decision (Figure 8).

The statement however offered little to no detail on the bank’s preference on potential easing measures. RBA communications between now and the 3 November decision will therefore be scrutinized closely. In particular we think markets will focus on the speech by Governor Lowe scheduled on 15 Oct, by Assistant Governor Chris Kent on 20 Oct, and Deputy Governor Guy Debelle on 22 Oct. The minutes from the 6 Oct RBA meeting, due for release on 20 Oct will also be in focus. Markets will pay close attention to discussion of the following topics in the speeches:

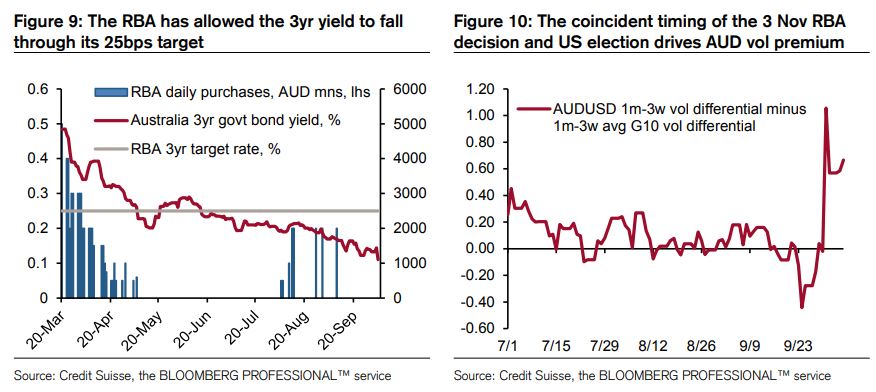

Interest rate preferences: The bank has several interest rate tools at its disposal. The bank’s cash rate, the 3yr yield target and the term funding facility are currently at 0.25%, while the exchange settlement rate is at 0.10%. Cuts to the cash rate are at this point deemed almost symbolic given that the actual ES accounts clear about 15 basis points below this rate. Alternatively, the bank could cut its 3yr yield target, currently at 0.25%, as 3yr yields are already trading about 15bps below its target (Figure 9). Lastly, the bank could cut its term funding facility rate.

QE purchases: Aside from tinkering with its available rate tools, the bank can opt to deploy a traditional QE purchasing program. The bank’s current purchases are under a Yield Curve Control (YCC) program, but the bank has been very flexible with allowing the 3yr yield to fall through target. We would consider the discussion of asset purchases defined in terms of quantity, as opposed to being tied to achieving a defined market outcome (such as the current QE policy), as a dovish development.

In the meanwhile, with the 3 Nov RBA decision in focus as the most likely date for policy easing, vol markets have priced in a large amount of risk premium in AUD space around the date, well above what is priced in for the US election on the same date for other G10 currencies (Figure 10). This creates a potentially tricky combination of factors, and arguably a higher bar for RBA easing to meaningfully weaken AUD, especially if US elections were to yield the relatively “clean” Dem sweep that investors associate with a weaker USD, and that markets are increasingly pricing in as the most likely outcome.

In this sense, the fact that the RBA opted to wait at the 6 Oct meeting reduces to some extent the potential for AUD to trade idiosyncratically later in the year, as investor willingness to take directional views around the decision will be understandably curtailed by the coincident timing of one of the biggest risk events of the year. Nevertheless, in the weeks leading up to the election, we still see potential for RBA expectations to weigh on AUD, especially if the upcoming speeches were to focus more on the possibility of a more structured extension of QE purchases. As such, we remain focused on 0.70 as our tactical AUDUSD pre-election target.

Budget provides marginal long-term upside potential for AUD

The announcement of the 2020-21 budget by the Morrison administration is a less clear FX driver than the RBA decision, but on the margin is likely to be seen as a long-term positive in our view. Most of the announcement was broadly in line with expectations: the government produced an A$213.7bn (11% of GDP) budget deficit estimate in the 12 months through June 2021, largely in line with market estimates set on $220bn. Also in line with expectations, the administration brought forward pre-announced tax cuts, and pledged to invest heavily in infrastructure and to promote further de-regulation.

The constructive surprises in the budget were the announcement of a new wage subsidy program for trainee workers, and the reduced focus on the 6% unemployment rate target previously introduced by Treasurer Frydenberg. The former is notable as is expected to be operational immediately, but is arguably quite small at A$1.2bn vs the $A85.7bn cost of Jobkeeper payments over the 20219-2021 period, as estimated in the July update.

The changes on the fiscal constraints related to the unemployment rate on the other hand are more meaningful in our view: the government had previously announced that they would pursue an accommodative stance until they brought unemployment “comfortably below the 6% mark”. Relative to the July update, the main update on this front from Treasurer Frydenberg’s speech was that he expects “the unemployment rate to fall to 6.5% by the June quarter 2022”, still well above the 6.0% level where the government approach would shift to “rebuilding fiscal buffers”.

Ahead of the event we had mentioned the possibility of an early projection of the unemployment rate falling below 6.0% as a risk from the budget: the outcome instead reduces the risk of markets having to price in a tightening of fiscal conditions in the near-term, which all things equal we think is a positive long-term factor for AUD.

Correct on monetary policy. Wrong on fiscal policy. The Depressionberg Unstimulus was shockingly short of demand pump-priming and with the huge output gap the supply-side measures are going to do bugger all meaning the RBA will have to do much more. In short, both fiscal and monetary settings are strongly AUD negative.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.