Eliza Owen, Head of Research Australia at CoreLogic, has released an interesting report examining property returns during Australia’s 20 years of low inflation:

The latest CPI results from the ABS showed a 1.6% increase in the consumer price index over the September quarter. The increase was the highest quarterly result since 2006, and adjusting for a strong rise in inflation takes some shine off the recent value increases seen across smaller capital city housing markets in the period.

Factoring inflation into the rate of capital gains of dwelling values provides an important perspective that is often overlooked.

Housing is an integral part of Australian household wealth, and has been identified as a key source of equity for funding aged care and health care later in life. Therefore, inflation can affect the real value that be accessed through property over time.

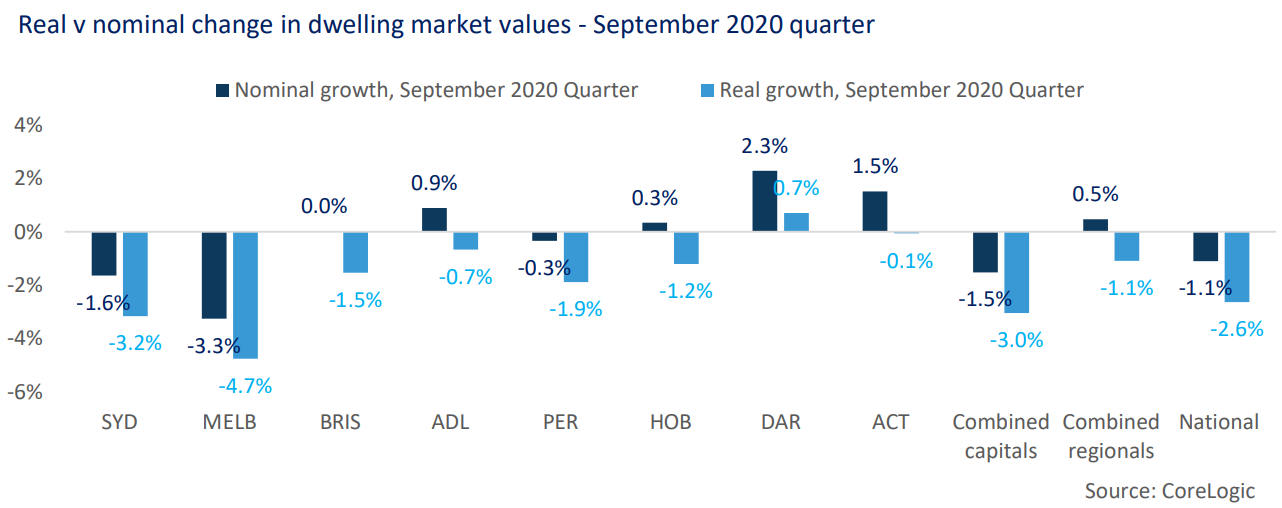

When taking headline inflation numbers into account for the September quarter, real (i.e inflation adjusted) changes in house prices showed declines across 7 of the 8 capital city markets, and the combined regional markets. Darwin was the only capital city market to exhibit real dwelling value growth, at 0.7%.

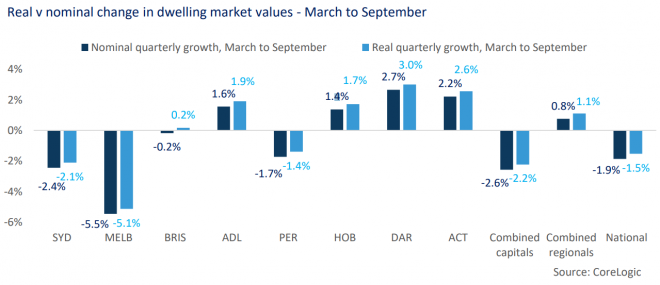

However, the 1.9% decline in headline inflation through the June quarter, which was not fully recovered by the September result, has reduced the real decline in property values through the pandemic compared with the nominal result.

Nominal declines in national dwelling values were 1.9% between the end of March (when stage 2 lockdowns were rolled out across Australia), and September. However, adjusting for the deflationary period in June, real dwelling values fell only 1.5%.

While annual inflation has been weighed down to 0.7%, real growth in national dwelling values was 4.1% in the year to September.

Cash rate reductions, which are anticipated through November, are prompted by a low inflationary environment, but simultaneously increase demand for property, and typically push prices higher. Despite the initial correction in home values that came with high uncertainty and a slowdown in economic activity, residential real estate values show signs of stabilising, or even increasing.

A particular challenge through the current period may be for those trying to save for a deposit to buy property, particularly for first home buyers who do not have existing property to draw on for sale or equity.

On the one hand, low inflation erodes the value of savings at a more gradual pace. But with the cash rate potentially hitting new record lows in November in an attempt to lift inflation, deposit rates for savings accounts are likely to be further compressed. This could see first home buyers trying to enter the market with increasingly low deposits, meaning more debt, which in a low inflationary environment, is harder to pay off over time.

What does inflation tell us about real returns in different areas over time?

Growth in housing across Australia at the macro level has broadly outpaced inflation, creating real returns for property owners across Australia. In the June 2020 Pain and Gain report, it was noted the median return for resales on property held for 30 or more years had a nominal profit of $569,000. On the median resale through the June quarter, this amounted to a real return of $230,000.

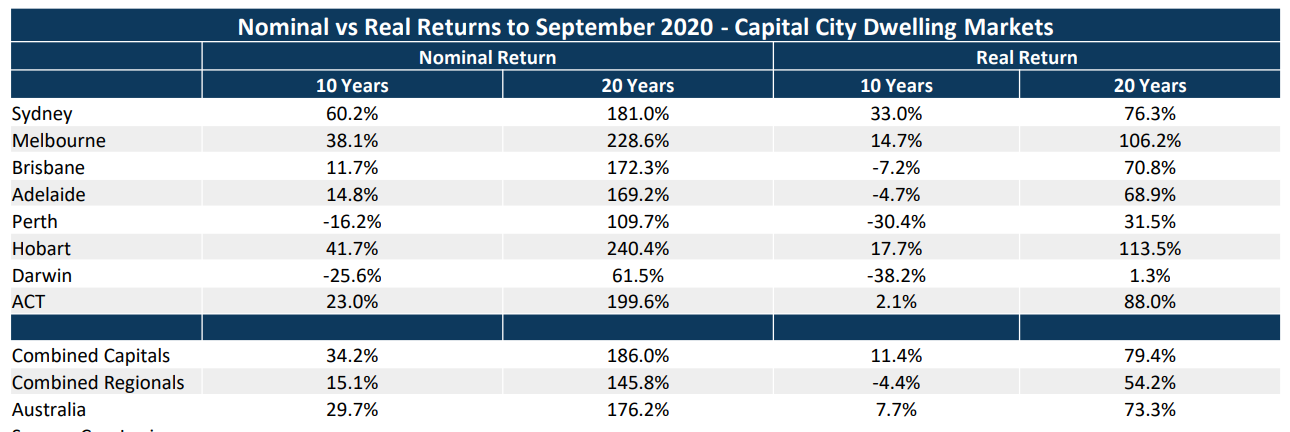

The table below summarises the nominal versus real returns on capital city dwelling values over a 10 and 20 year period. The 10 year real return highlights the weakness in long term returns from mining-related markets like Perth and Darwin. It also highlights that the growth in the Brisbane market over the past 10 years can be largely attributed to inflation.

Over a 20 year period however, each capital city dwelling market has returned growth higher than inflation. Real returns for housing in Australia increased from the late 1980’s, driven by deregulation in the financial system, increased globalisation and relatively low levels of supply to strong population growth.

Stubbornly low inflation against a low interest rate environment may continue to boost real returns for home owners, but could exacerbate the challenge for non-home owners to get on the property ladder.

I made similar observations in my 2016 Special Report: “Why common housing affordability measures are wrong”.

Inflation and interest rates might be very low, but this has been accompanied by poor wage growth, which means a greater burden across the life of a mortgage. This is the real problem with housing affordability.

Advertisement

Periods of high inflation, like we saw in the 1970s and 1980s, are generally accompanied by high nominal wages growth. And this high wage growth effectively inflates away one’s mortgage balance over time.

By contrast, low inflation and low nominal wages growth means that a jumbo-sized mortgage taken-out today will remains a big mortgage for decades to come.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.