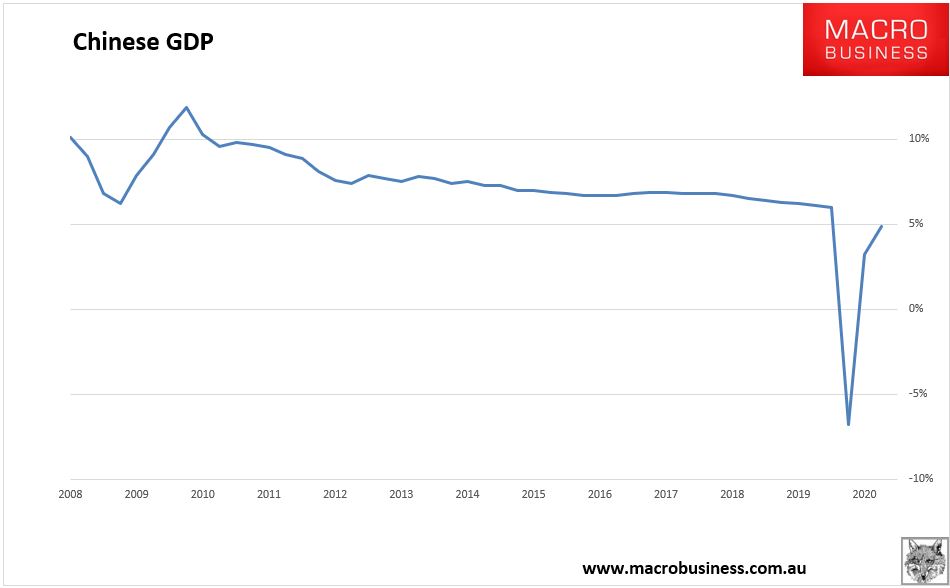

China dropped its Q3 data dump late yesterday so let’s take a look. Year to date GDP came in at 4.9%:

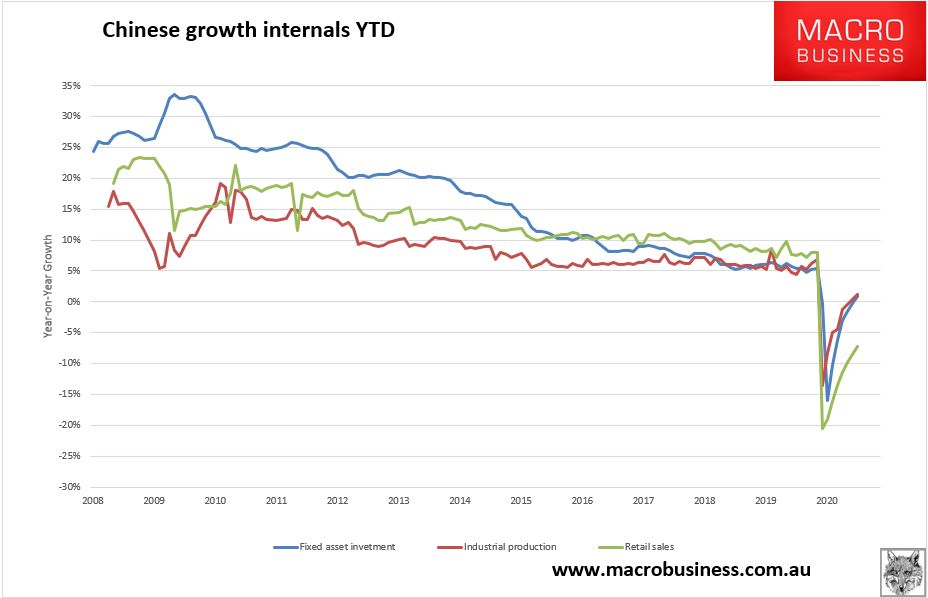

The growth internals for September were 1.2% for industrial production YTD, fixed asset investment 0.8% YTD and retail sales -7.2% YTD but 3.3% YOY:

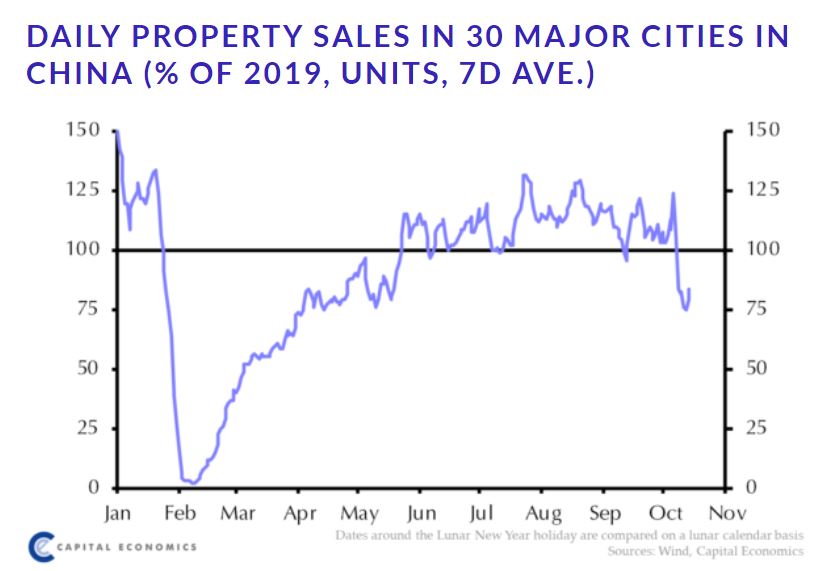

Property sales were solid in Q3 but have lately tumbled:

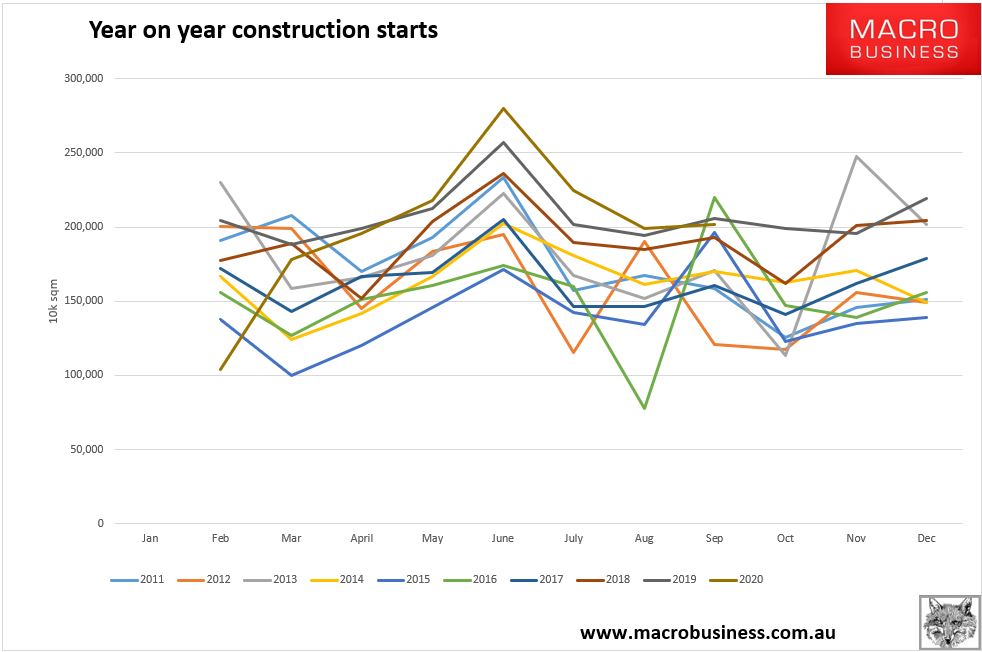

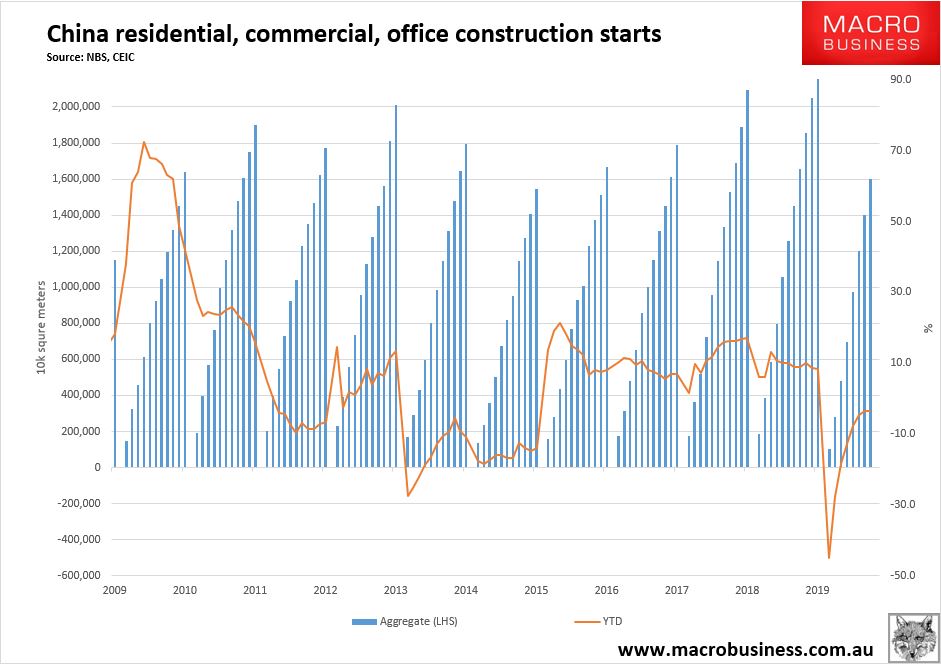

Floor area starts slowed and actually fell YOY for the first time in five months:

YTD starts are down -3.6%:

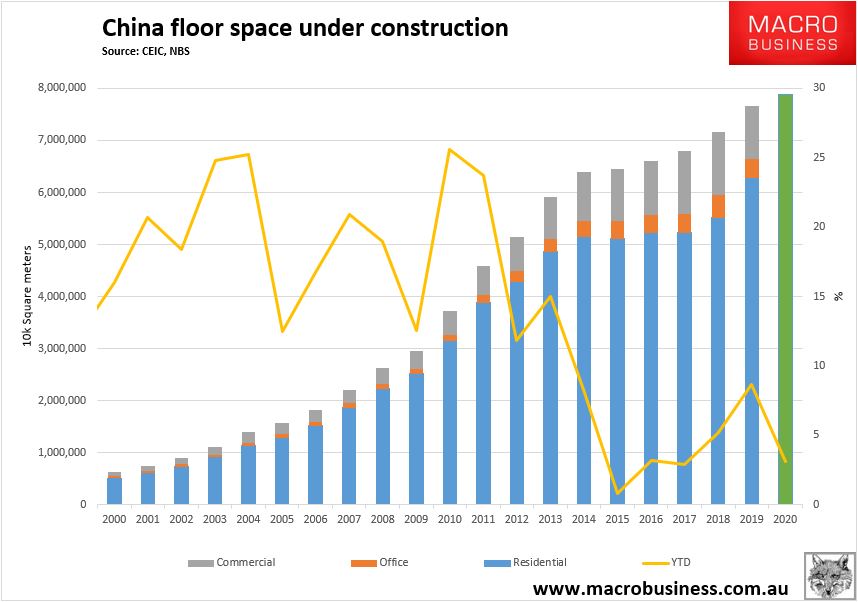

But, because COVID also hit existing project and completions, floor area under construction is still up 3.1% YTD though has started to slow:

There is a hint here that the empty apartment boom is coming off a little.

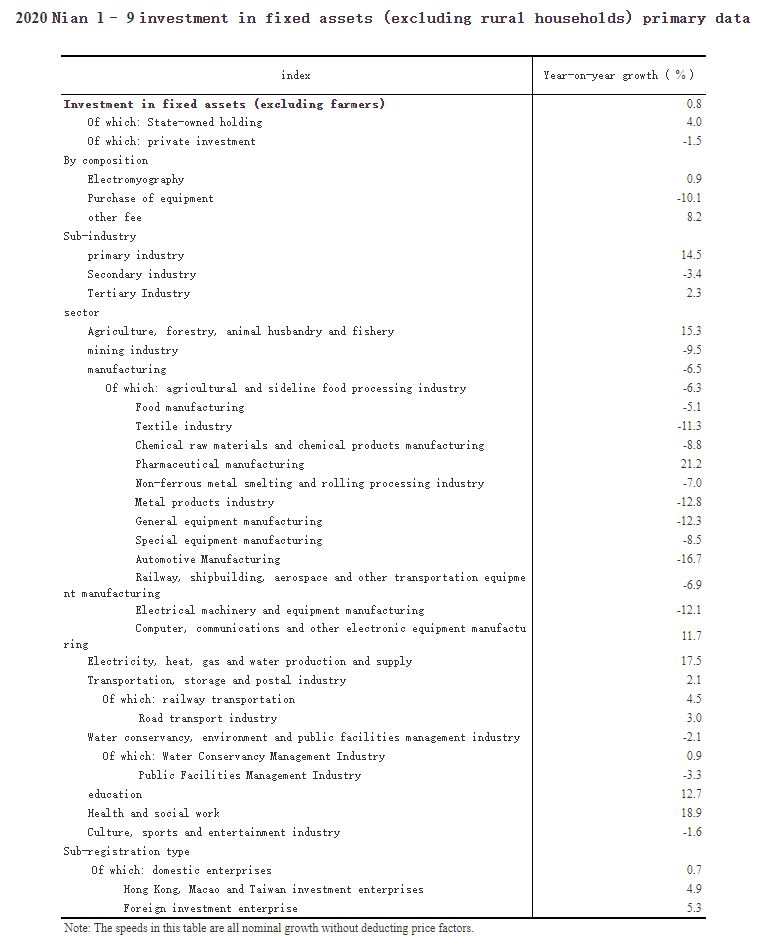

That said, fixed asset investment powers on thanks to heavy infrastructure investment in pharma, utilities, transport and services. I lot of manufacturing investment is still stalled:

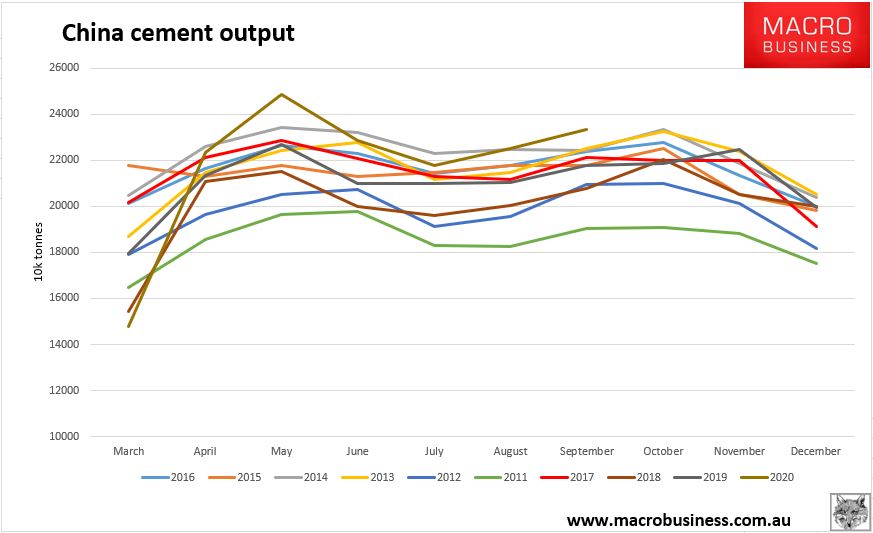

Cement output hit all-time highs as the infrastructure boom sucked in raw materials:

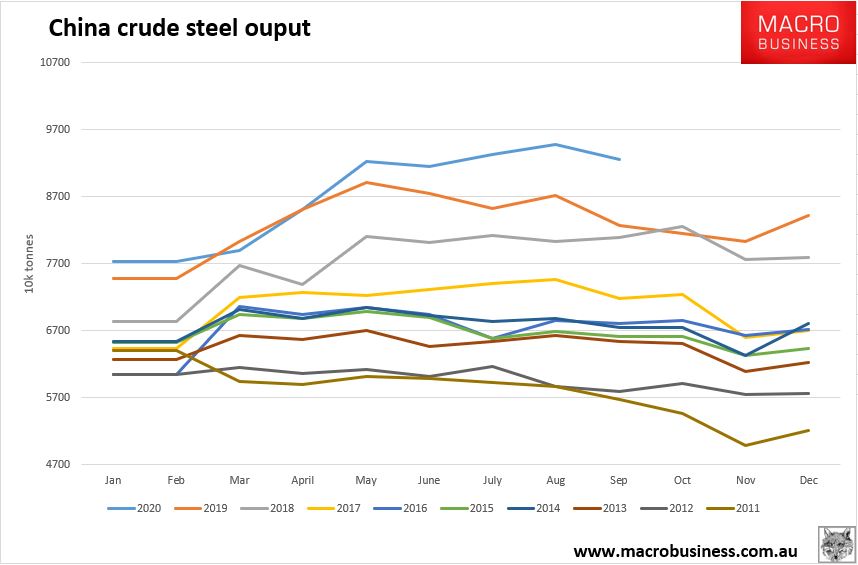

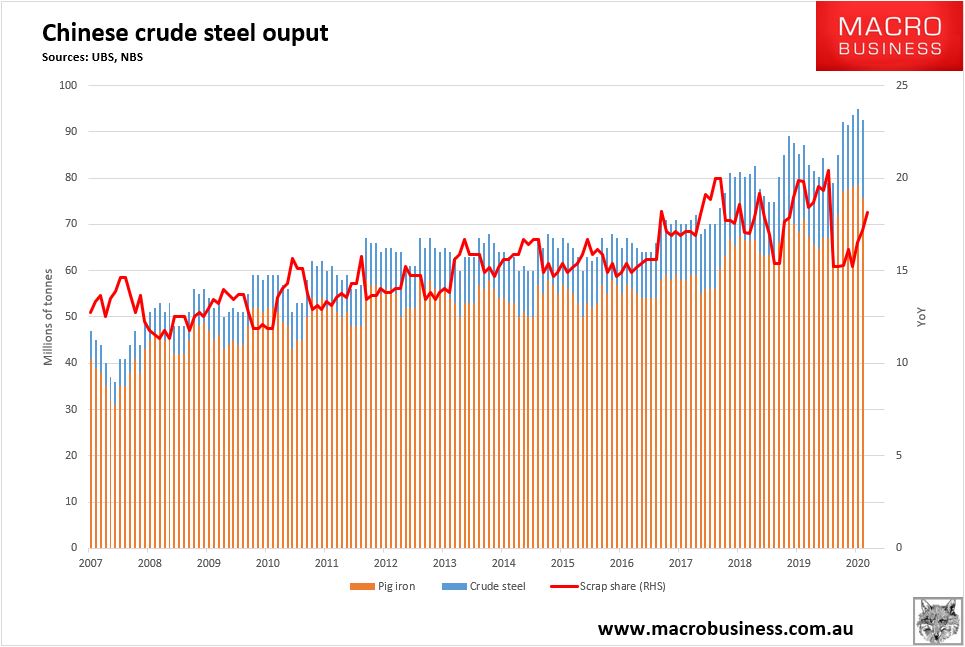

Steel output remains preposterous:

The scrap share has started to rebound as arc furnaces join the recovery:

Still plenty of demand for iron ore embedded here.

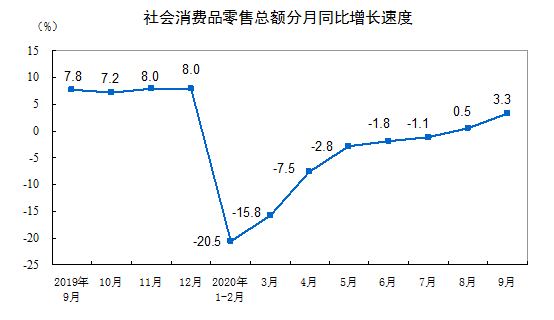

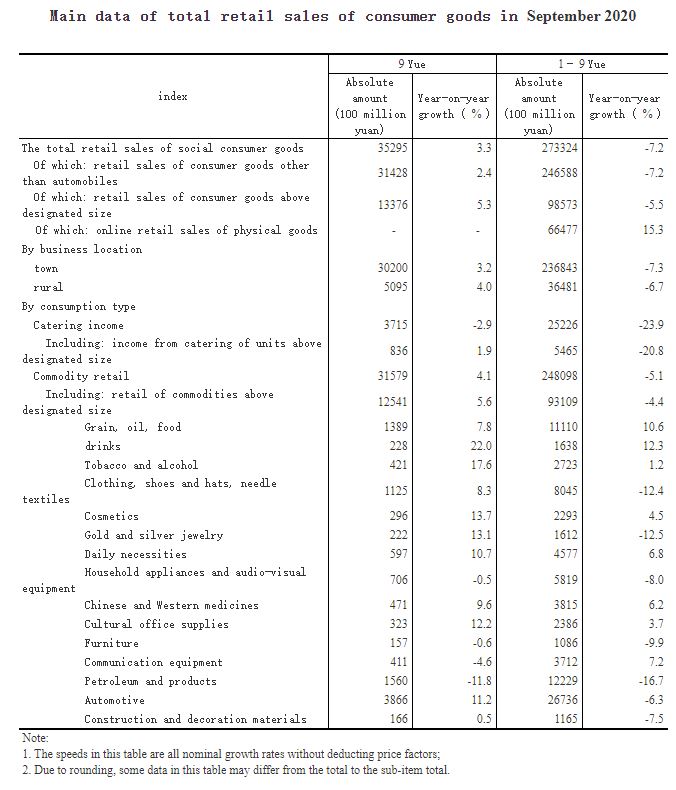

Finally, retail sales picked up 3.3% YOY:

Sales growth categories broadened, too, though travel and eating out are still struggling:

So, some evidence that the recovery has begun to filter down to households.

Yet it is still clear that the engine of growth is building anything and everything, except new factories.

The latest credit data suggest no end in sight to this stimulus so despite some slowing segments of construction it is most likely that the building will continue for the foreseeable future.